Monthly Update October 2014

CONCLUSION

Last month, I wrote about a change in character in the markets, based on weakness in global equities and high yield corporate bonds. This change, which is from up to down, appears to be accelerating. The percentage of stocks on the NYSE Index above their 200-day moving average has fallen to 47%, which means that more than half the companies are in major downtrends. Though the S&P 500, even after today’s -2% loss, is up 5.3% for the year, it represents only large companies. In contrast, the Russell 2000, representative of small companies, is down -7.2%, international stocks as represented by the Vanguard Total International Fund are down -3.3%, and mid-sized companies are down -0.30%, based on the S&P 400 Midcap Index. Below is a weekly chart of the Russell 2000, going back to August 2011, courtesy of www.stockcharts.com.

You can see the uptrend line in red I’ve drawn off the 2011 low, which has now been decisively broken. Small cap weakness has been warning of more serious trouble, and the Russell 2000 has already violated its early August low. The equivalent level for the S&P 500 is the 1904 level. When the S&P 500 breaks its uptrend line, all stock markets will be in gear to the downside. There is no telling just how far down such a decline may go. Given the fundamental overvaluation and dependence on the Fed, anything is possible. Investors should remember that markets decline much faster than they rise. The bottom line is that the major trend of the market is in question, and that is reflected in our current positioning.

A Potential Positive—the Election Cycle

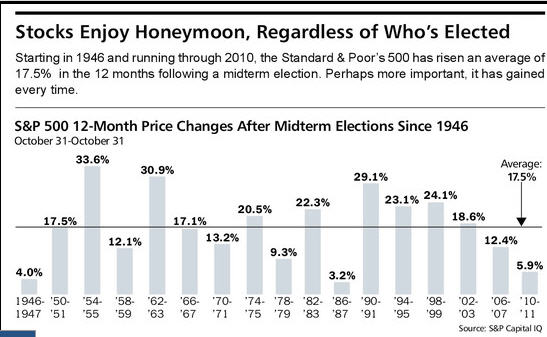

If one believes in history and cycles (and we do, over long periods of time), then the following may be encouraging as we enter 2015. A midterm election is coming in November, and as the table/chart below shows, courtesy of S&P Capital IQ, there have been 17 since 1946.

As you can see, when measuring the price change of the S&P 500 from October 31 to October 31, there has never been a down year, with the average gain being 17.5%, and the smallest gain, 3.2%. When analyzing calendar year data in a pre-election year, you have to go back to 1937 to find a losing year (-2.3%). From this perspective, the odds seem pretty favorable, but the “stat geek” part of me worries about 17 observations—it is not statistically valid. This reminds me of an unfortunate baseball event that just happened—until last week, no team who finished with the best record in baseball had ever been swept in the division series. Well, the Angels are the first. And second, Clayton Kershaw of the Dodgers, probably the best pitcher in baseball, just lost twice in one week. I guess what I’m saying is—don’t take this data to the bank. It won’t work every time, anymore than the “best six months” and the “worst six months” don’t work every year. Remember, the Fed’s monetary policy is unprecedented, and the consequences unknown. As always, we’ll rely upon the direction of our various risk models to guide us in a disciplined manner.

A Quick Inflation Update

Though not official yet, it appears the Social Security Administration will be announcing shortly the COLA adjustment for 2015 (cost of living). The projection is for a 1.7% increase.

This week, gasoline prices hit a four-year low. Despite the many fears of rising interest rates, the weakness in commodities across the board and global markets (much of Europe is in a recession), the biggest risk does not appear to be inflation, but rather deflation.

Portfolio Changes / Updates & a brief note on Bill Gross

You’d have to be hiding under a rock to not know that legendary mutual fund manager, Bill Gross, left PIMCO two weeks ago, the firm he founded and built into a $trillion money management business. We do not own PIMCO Total Return, the main fund he managed, in hardly any accounts, but do recommend it in the 401 (k) plans of various clients. We wouldn’t sell the fund just because he’s left, nor would we buy his new fund at Janus. We own other bond funds at PIMCO, including Short Term, GNMA and High Yield, and are very comfortable with them. Mr. Gross is an excellent money manager, but apparently, even by his own admission, not a very good manager of people. Those are two different skill sets. At age 70, with all the money one could want, he is not retiring from life, but rather starting a new challenge. What a great attitude. Good for him.

Back in June, we made a switch in funds within our bond strategies, selling Sierra Core Retirement Fund (SIRZX) and replacing it with Sierra Strategic Income Fund (SSIRX). It is run by the same management team who we know quite well. The new fund is run in a similar fashion, with more emphasis on income, and is a transaction fee fund on the Fidelity platform. The expense ratio is lower by 0.83%, which is a savings to clients, with performance just as good, so we think it is a win-win.

A week ago, one of our five core tactical equity funds fell out of our rankings, so we have sold off almost all the position in Southern Sun Small Company Fund (SSSFX), replacing it with Hotchkis & Wiley Value Opportunities (HWAAX). We’ve owned Southern Sun since May 29, 2012 and it’s been a rewarding holding during this team, beating the benchmark of the Vanguard Total Stock Index and Vanguard Total International Index (75/25), by a decent margin—up 57.4% vs 45.7% for the period.

Finally, in the last few weeks, we’ve been eliminating the Marketfield Fund (MFLDX) from all accounts, and will soon be finished with that process. We’ve been disturbed since April after attending a dinner with their top fund manager, and not liking what I heard. My gut told me when their asset base had ballooned from $4 billion to $20 billion in one year, becoming the largest alternative fund in the industry, that performance could not continue. I decided to give the fund some additional time, but concluded my original instincts were correct. We’ve had mixed results in the past several years with alternative funds, and have chosen to minimize exposure going forward, wanting to more rely upon our own work in risk management and selection.

Currently, tactical equity exposure is down to 40%, below neutral. We still have a 50% position in real estate via the IYR. In bonds, we are 100% invested in PIMCO GNMA, but now down to just 30% in Loomis Sayles Bond with the other 70% temporarily in Loomis Sayles Limited Maturity. And, in corporate high yield, we remain 90% invested in short term bond funds such as Fidelity Short Term Bond, PIMCO Short Term and Blackrock Low Duration, with the remaining 10% in high yield. We are in a fairly defensive posture until our models improve.

Material of a Less Serious Nature

Here’s this month’s humor, to lighten things up.

Men in Heaven

When everybody on earth was dead and waiting to enter Paradise, God appeared and said, “I want the men to make two lines. One line for the men who were true heads of their household, and the other line for the men who were dominated by their women. I want all the women to report to St. Peter.

Soon, the women were gone, and there were two lines of men. The line of men who were dominated by their wives was 100 miles long, and in the line of men who were truly heads of their household, there was only one man.

God said to the long line, “You men should be ashamed of yourselves. I created you to be the head of your household! You have been disobedient and have not fulfilled your purpose! Of all of you, only one obeyed. Learn from him.” God then turned to the one man and asked, “How did you manage to be the only one in this line?”

The man replied, “My wife told me to stand here.”

Until Halloween, which is still a pretty big deal at the Kargenian and Medland households (with our respective youngsters), we’ll be back with more in a few weeks.

Sincerely,

Bob Kargenian, CMT

TABR Capital Management, LLC(“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site(www.adviserinfo.sec.gov.).

For additional information about TABR, including fees and services, send for our disclosure brochure as set forth on Form ADV from us using the contact information herein. Please read the disclosure brochure carefully before you invest or send money.

The results of TABR’s Model Portfolios are net of actual fees deducted from client accounts and include the reinvestment of dividends and other earnings. Comparison of the TABR Model Portfolios to other indices is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors. The returns noted of various market indices include reinvested dividends unless otherwise noted.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the model results above in part because client accounts may be allocated among several portfolios or have substantial cash flow in or out of the account. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge.