There’s Nothing Fair About The FAIR Plan, And Time To Buckle Up?

Federal Reserve Chairman Jerome Powell is happy that inflation seems headed in the right direction, now running at just under 3% annualized. He’s obviously not purchased homeowners insurance in California recently.

In this month’s update, we’ll discuss our latest experience with that area, along with the historical negatives of September stock market seasonality, the recent stock market breadth thrust, off channel communications and Michelle’s Masters. No cheating and skipping right to the humor.

California’s Insurer Of Last Resort

Do you ever wonder who comes up with these names of governmental agencies, or legislative bills? Like the Inflation Reduction Act of 2022. Really? The cost of most everything is going up, except for perhaps McDonald’s $5 value meals. Or the name of a new retirement plan several years ago, called the SIMPLE Plan for small business owners. Have you ever tried to open one? They’re a pain in the tush.

Which brings us to California’s FAIR Plan. Please, no darts or arrows from our wonderful out of state clients. Some of you have your own issues. At least we have good weather! But, try getting homeowners insurance. Eh, not so easy these days. As I related a year ago, the policy for our home in Yorba Linda was with a company named AmGuard, which is actually a Berkshire Hathaway company (think Warren Buffett).

They notified us during the summer (with an August renewal date), that they were canceling our policy because our home is deemed to be in a fire zone. Our insurance broker indicated we could appeal to them, and figuring we had nothing to lose, we did, completing a 12 question profile. Two weeks after submitting our appeal, they rescinded the cancellation and agreed to renew our policy for another 12 months.

Two months later, in October 2023, we received a notice that AmGuard was canceling our policy effective August 2024 since they were leaving the state. At least we’ve known for many months we needed to do something. Some context. Our premiums for the latest year were essentially $4900.

The state’s FAIR Plan gets its name from Fair Access to Insurance Requirements. It was created in 1968 to provide insurance to homeowners in high risk areas, such as those in fire zones or earthquake fault lines. It’s considered the insurer of last resort, as more than 350,000 new policies have been issued in the past year as several large companies such as State Farm and Allstate have canceled tens of thousands of policies, while others such as AmGuard have simply left the state.

The FAIR Plan does protect from fire risk, but it doesn’t cover personal liability, vandalism, earthquake, hail, flood or theft. As a result of the limited coverage, homeowners must get an additional policy to fill the gaps. This is called a “difference in condition,” or DIC policy.

Our Farmer’s agent was unable to find a company who would insure our home. He experienced the same thing, since he lives in Yorba Linda, and at least one of our clients, also a Yorba Linda resident, has had to move to the FAIR Plan. I did reach out to an independent agent who was referred to me by a dear friend, and she was excellent at what she does. The first quote she got for our home was for . . . $39,000. I’m not kidding. She then found a non-admitted insurer in the Bay Area who quoted us $15,000.

What is a non-admitted insurer? These companies are approved, but not licensed, to offer insurance in the state, and they’re not subject to the same regulations as traditional insurers (for instance, they can charge more and aren’t subject to caps). One of the drawbacks of being with a non-admitted carrier is that claims may not be paid in the event the insurer becomes insolvent. Lloyds of London is an example of one of the world’s most well known non-admitted insurers.

In the end, we ended up with a quote from the FAIR Plan for $6,765 for dwelling coverage of $1,845,000, which works out to $461 per square foot to rebuild. On top of that , we had to purchase a DIC policy from Farmer’s, which ran another $3600. But that wasn’t the end of it. The Farmer’s policy required that we install an earthquake gas shutoff valve, a Moen water leak detection system and have central station burglar and fire alarm monitoring.

The first two items cost us an additional $2500 or so from a licensed plumbing contractor, and we’re in the midst of getting a quote on the fire alarm monitoring (we already have a burglar alarm system). As you can see, our base premiums have more than doubled, up over $5000 annually. Or, to put it another way, at $25 per person for breakfast, that’s 200 trips to the Original Pancake House in Placentia. That’s depressing.

Depending on where you live, whether it be in California or other states, you may be facing similar issues. This, unfortunately, is one of the downsides of substantially rising home values. We purchased our current home in Yorba Linda in August of 2019 for $1.79 million, and today, Zillow and Redfin estimate its value at around $2.75 million. Honestly, I think I would be just as happy if our home was still worth $1.79 million. Our taxes would be lower and so would the homeowners insurance (I think).

I think it’s fair to ask—would I be happy also if our portfolios were the same value as they were in 2019? Probably not. Is that hypocritical? I don’t know. I view living and owning a home as different than our investment portfolios. I do know this, though. Life is short, so eat the bacon!

September Seasonals Dead Ahead

The financial press often use the term “volatility” in headlines and articles, almost always associating it with large down days in stocks and intermediate declines. But, the truth is, volatility actually works both ways, and that’s been on display since the stock market’s most recent peak on July 16.

From July 16 to August 5, the S&P 500 Index fell -8.48% on a closing basis, and has recovered nearly 100% of that loss since, gaining back +8.63%. Similarly, the Nasdaq 100 (NDX) fell -12.27% during the same period, and has gained back +10.19% since August 5.

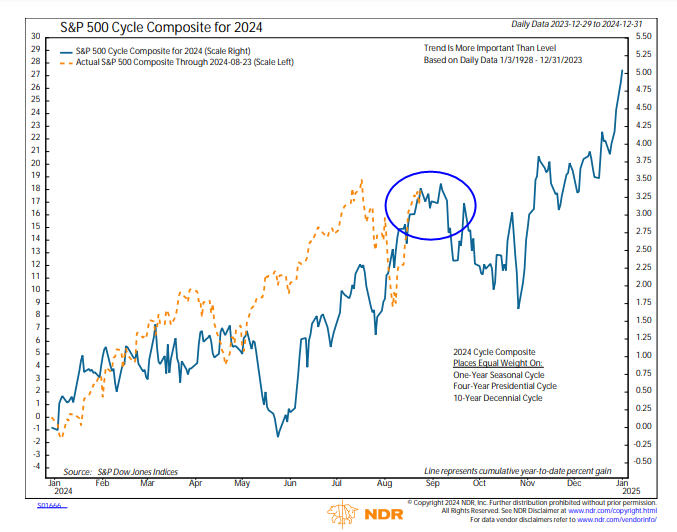

Historically, going back to 1950, the period between August and the end of October is the worst time of the year for stocks. Cycles don’t always work, but it’s helpful to know their tendencies in alignment with how the market is actually behaving. Below is the S&P 500 Cycle Composite for 2024, courtesy of our friends at Ned Davis Research (www.ndr.com).

As you can see, the projected path of stocks isn’t always in line with the reality. The decline called for in May took place in April. But, the peak in mid-July was spot on, and the V-shaped rebound has been equally spot on, and certainly not expected by most people. Now, as we approach early September, be prepared for some turbulence leading into the election. An update on some of the technicals is below.

Again, stock market cycles are not perfect, but if the market follows the pattern above, no matter who wins the Presidential race, stocks are likely to end the year on a high note. We’ll see.

Breadth Thrusts And New Highs/Lows

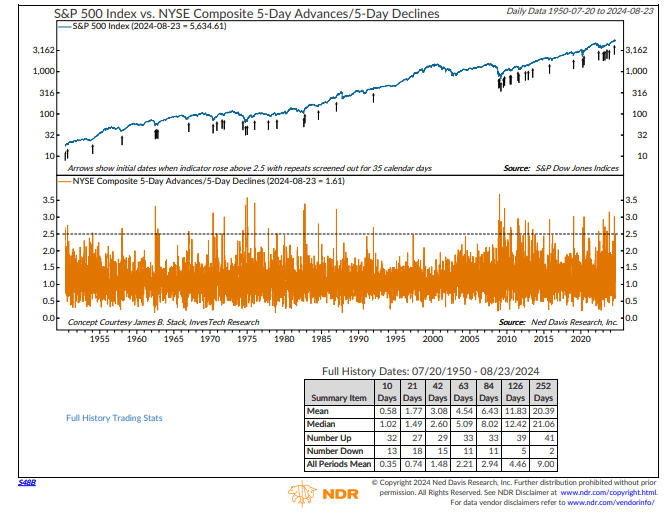

Though it coincided with the market’s recent peak, the ratio of five-day advances of the stocks in the NY Composite Index relative to five-day declines rose above the 2.5 threshold on July 16, generating what market technicians term a “breadth thrust.”

The concept behind this indicator is from analyst and money manager James Stack, who writes the quite informative Investech Research newsletter. Below, Ned Davis Research created a chart using the above rule and took the data back to 1950.

There have been 43 prior cases since 1950, with median gains of over 21% looking out over the following year, with only two cases resulting in losses. First, that’s statistically significant, and second, the median gains are more than double the market’s gains over all periods. This is a bullish development.

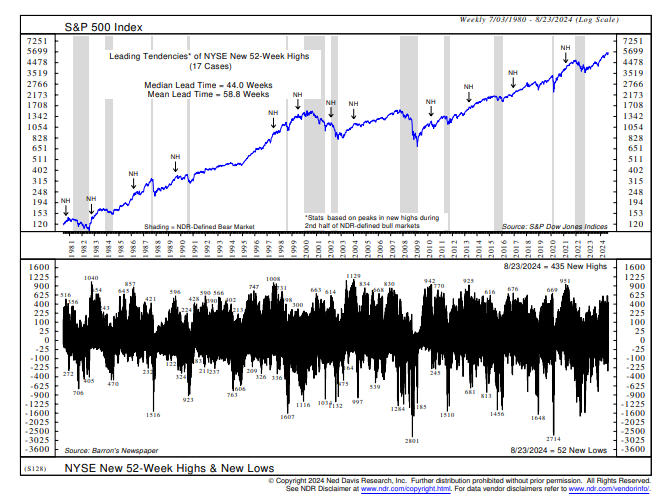

Coupled with the number of stocks making new weekly highs (see below), and the NYSE Advance-Decline Line confirming recent highs a few weeks ago, the odds suggest an eventual final market peak is likely to be many months away, possibly coinciding with year-end cycles.

The above chart, also courtesy of Ned Davis Research, shows the number of 52-week highs on the NYSE as well as the number of 52-week lows. A new cycle high was reached on July 19, a “confirming” indicator, much like the advance/decline line. Why is this significant?

In the past 44 years, weekly new highs have peaked a median of 44 weeks before the market’s final top. That would put us in the December/January time frame. It pays to monitor the number of stocks making new lows. When conditions become more problematic, you’ll often see a significant pickup in the number of new lows. At present, that’s simply not the case.

Portfolio Allocations

As has been the case for many months now, our tactical portfolios remain nearly fully invested, with 83% exposure on the stock side, while our high yield bond risk model remains on its November 2023 BUY signal, and this area has continued to make new highs nearly every week. I hesitate to say, “Don’t worry, be happy!” especially in front of expected September/October turbulence, but at present, that’s what the indicators say.

Off Channel Communications

The investment advisory profession is one of the most regulated industries in the nation, and that process seems to get worse as time goes on (hey, why should we be any different than all the other professions?) 🙂

There are numerous records we must maintain, from daily trading logs, to email archiving, and all sorts of regular compliance processes, such as a Business Continuity Plan, personal trading disclosures and a host of other things, all of which partner Steve Medland can educate you on, as he has served from day one of TABR as our Compliance Officer. All of us at the firm take this area quite seriously, as over 200 plus clients entrust their life savings with us.

In some 20 plus years of TABR, we have been audited twice by the SEC (Securities & Exchange Commission). You don’t get grades from the SEC, such as an A, B or C. Rather, if you’ve done mostly everything right, you just won’t get any nicks on the post-audit analysis, and they’ll send you on your way. We do know this. We run a very low-risk firm. All of our investments with clients are traditional—stocks, bonds, mutual funds and ETFs, with hardly any annuities and no private placements or alternative investments.

All of our clients’ funds, other than a handful of 401 (k) plans we manage, are custodied at Fidelity Investments, one of the most reputable firms in the business, and everything is transparent.

Why am I writing about this? Because texting has become a present communication tool in modern life, and it presents a problem for compliance because regulations oblige advisors to retain and archive such communications. I use my email at TABR and my cell phone for both personal and business purposes. There is no problem archiving all of our email correspondence with clients. But, texting is another story.

I’ve learned that advisors at certain large broker/dealers have to maintain two phones, one for clients/business and the other for their personal life. I’m sorry, but life is complicated enough, and that’s not happening with me or Steve. Honestly, one of the biggest reasons we formed TABR some 20 years ago was to run our own business and not have some home office overlooking everything we do. We take compliance seriously, and we’re certainly not telling the SEC that we don’t text with clients.

But, I will say this. Our texting is limited to confirming appointments, or responding to a text from a client, and that’s usually with, “Hey, I’ll call you.” We don’t conduct business via text. If you text us something that relates to planning, or orders, you’re likely going to see that we respond to you via email and/or a phone call. With our email, we have a “paper trail,” but with texts, they can easily be deleted, and that’s why the SEC is concerned with this form of communication.

Here’s another angle. As we gather documents for planning and such, some clients in the past (and likely future!) have attempted to send us documents via text. Please don’t do that. Most of the time, the documents aren’t formatted properly, and they’re difficult to convert to email where we can actually read them and use them on a full screen.

As for phone calls, many of you have my personal cell phone number, and Steve’s as well, and we’re quite transparent with that information, which is on our business card. Some clients call us on our cell phone number during weekdays, instead of our office number. If you do that, you may find that I don’t pick up, or I call you back several hours later. Why? Because if I’m at my office, which is most of the time (I don’t work remote), I’m either on the phone or working on stuff.

And, if you leave me a message on my phone, I may not see it for a bit. For some reason, I check my texts more often than I check my phone messages. My wife will even tell you—if she calls my cell and I don’t pick up, and she needs to speak with me, she’ll just call the office. I would suggest you do the same!

I hope this comes across that we’re “rigidly flexible.” And we are. Taking care of people’s money and doing planning is very personal, and Steve and I realize life doesn’t just happen from 8 to 5, weekdays. So, don’t fret if you need to call us on a weekend, or email us. We’ll get back to you as promptly as possible. We’re here to serve you.

From PT to MFT

When I met my wife-to-be, Michelle in 1989, she was working as a Physical Therapist for a spine clinic in Long Beach. She became mostly a full-time Mom in 1994 when our son, Adam, was born, but continued to fill in for friends and colleagues occasionally. That continued through 2004, when she became pregnant with our daughter Caroline.

After Caroline was born, her PT career was pretty much permanently set aside. As Caroline grew up and became more independent, Michelle developed an interest through our church in peer counseling, while also growing in her participation with BSF (Bible Study Fellowship). After a few years serving as a Group Leader with BSF, she became a TL (Teaching Leader).

For those of you unfamiliar with BSF, that’s like being named the Grand Poobah. You’re basically a non-paid pastor, giving a “sermon” on a section of the Bible every week, tailoring her personal style in communicating that week’s study material to a group of women that would often number from 125 to 175 people. She did this amazingly, and in an outstanding manner for 11 years.

A little over 3 years ago, knowing our daughter would soon be headed to college and for the first time in some 28 years, there would be no one to care for at home, Michelle pivoted and retired from BSF. She then decided to embark on a journey to pursue her Master’s Degree in Clinical Psychology with an emphasis in Marriage and Family Therapy.

In late June, that culminated in her graduating from Azusa Pacific University. Her next step is to accumulate enough hours as an Associate Marriage and Family Therapist, serving and seeing clients to become an LMFT, which is a Licensed Marriage & Family Therapist.

Michelle is currently transitioning to full-time with her employer, CIFT (Center for Individual and Family Therapy), as we prepare to send Caroline away for her sophomore year at Cal Poly SLO. I couldn’t be more proud of her drive, mission and desire to serve others. Below is a photo from graduation night, with Michelle’s mom, Dot, on the left, daughter Caroline, yours truly, and Adam on a stick!

Just a few weeks after the above, she celebrated her 64th birthday on July 18, and we did that by attending the final show of the North American tour of the Kid Laroi, at the Los Angeles Memorial Coliseum. We got the whole VIP treatment from our son and Laroi’s team, backstage and the whole thing. Below is a photo with Laroi and Adam, who many of you know has been Laroi’s chief photographer and videographer for three years running.

It was a special night, and we paid for it the next day at work, getting home at 1 am in the morning. Oh, to be young again. Adam, Laroi and their team went out for dinner afterwards and got home around 4 am. Just so you know, that is not what happens after every show. Not at all. This was a celebration of some 7 weeks on the road, plus being at home with friends and family.

Material Of A Less Serious Nature

A fireman is washing the engine outside the station when he notices a little girl next door. She’s sitting in a little red wagon with little ladders hung off the side and a garden hose tightly coiled in the back. The girl is wearing a fireman’s helmet and has the wagon tied to a dog and a cat. The fireman walks over to take a closer look. “That sure is a nice fire truck,” the fireman says with admiration.

“Thanks,” the girl says proudly.

The fireman looks a little closer and notices the girl has tied the wagon to the dog’s collar and the cat’s testicles. “Little partner,” the fireman says: “I don’t want to tell you how to run your rig, but if you were to tie that rope around the cat’s collar, I think he could pull more.”

The little girl replied: “You’re probably right, sir, but then I wouldn’t have a siren.”

Speaking of red alerts, the red flag was long ago raised by the Angels, who have the second worst record in the American League. And my Giants are on oxygen, 5 games back with five weeks to go. Miracles do happen, but it isn’t probable. Thank God for the NFL. In two weeks, my 49ers start their Super Bowl or Bust campaign. That’s eminently more interesting to me than Kamala and Trump. Yeech! Give me 18 weeks of Brock, Deebo, Nick and Fred and I’m a happy camper.

As always, thank you for the trust and confidence all of you place in us at TABR.

Best wishes,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.