Everybody Wants To Go To Heaven, But Nobody Wants To Die

I’m sure many of you have heard of this quote. To me, it’s another way of describing today’s economic situation playing out in the United States and in many cities. How so? We all want more, without the consequences. I’ll explain inside.

Plus, we’ll touch on the theory of American exceptionalism as it relates to stock market performance, along with Do We Trust The Thrust?, and The Decision, except this is not referring to LeBron James. Of course, we’ll close with some humor, which is always welcome. Read on.

More On Everybody Wants To Go To Heaven

I was surprised to learn when researching this saying that the quote was by Joe Louis, a highly respected professional boxer in the 1935 to 1951 time period. Given his profession, I’m taking a guess that what he was referring to in the world of professional sports is “everybody says they want to be a champion, but how many of them are willing to pay the price to be elite?” I was also interested to learn that Albert King, one of the most influential and greatest blues guitarists of all time, recorded a song by the same title in 1986. Where am I going with all of this, in relation to financial markets? Good question.

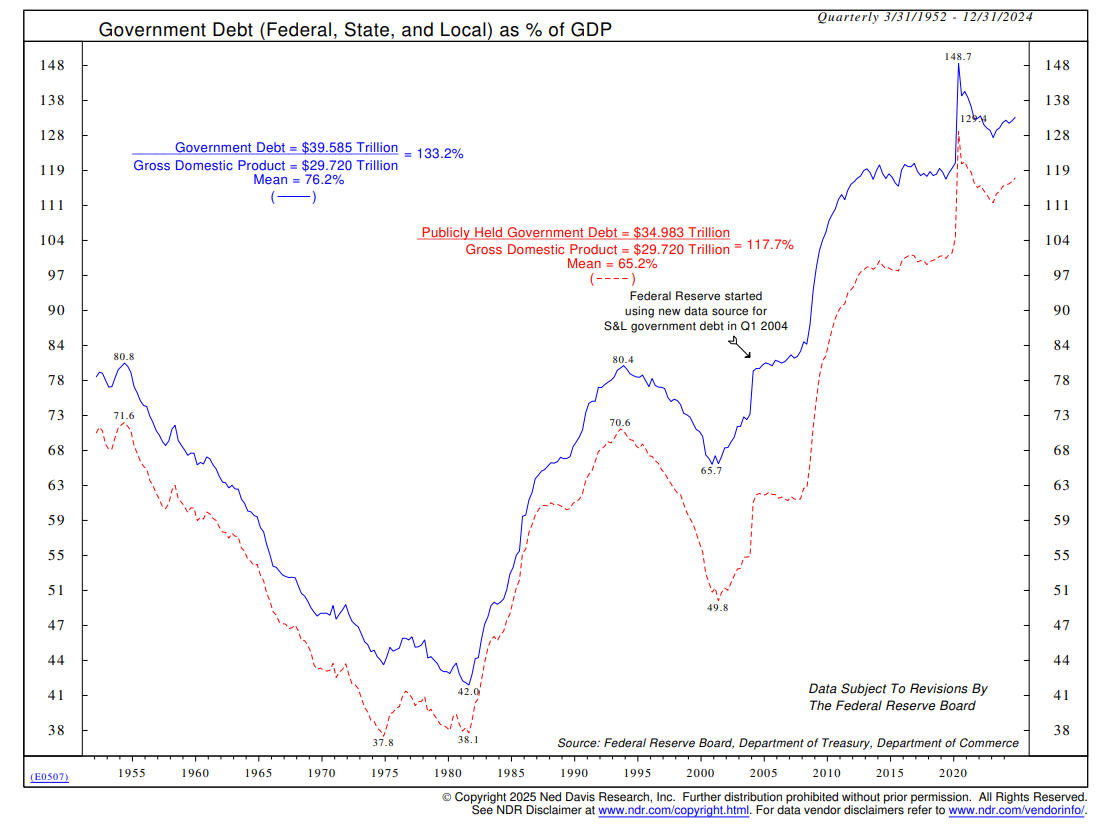

I believe the bottom line in this discussion is DEBT. We’ve all been railing for years that government debt is unsustainable, and that ultimately, it’s going to lead to financial Armageddon. Below is a chart, courtesy of Ned Davis Research (www.ndr.com), showing total government debt now at nearly $40 trillion.

The chart above combines both federal, state and local debt, so I want to emphasize this problem is not just in Washington. The City of Los Angeles is currently dealing with a $1 billion budget shortfall, and the mayor has put forth a plan to eliminate some 1600 jobs. A recent Los Angeles Times guest editorial was headlined “Mayor’s cuts would make our streets worse.” Let’s face it. If one has to eliminate $1 billion of spending, there is going to be pain in a lot of places, and nobody wants to deal with that. And that is the gist of this dilemma. Nobody wants to live within their means. It is too early to tell the effects of the recent DOGE (Department Of Government Efficiency, an oxymoron if I’ve ever heard one) efforts to reduce spending of the federal government. It’s possible that these efforts will make very little impact, because part of the problem at the federal level is that some 70% of federal spending is attributed to entitlements such as Social Security and Medicare, and it’s my understanding that those areas and others cannot be touched without the approval of Congress.

That’s like telling a corporate CFO who is responsible for a $10 million budget, and the CEO tells them they need to cut expenses by 15%, but they can’t touch 70% of their departments. There’s going to be some pain. If in fact in future years, there is significantly less government spending, that’s not going to be good for financial markets. Stocks, but not fixed income, have hugely benefited by the injection of capital into the markets from the Federal Reserve since the 2009 meltdown. When the Fed has pulled back, which they did in a large manner in 2022, markets fall. But, one cannot have an accommodating Fed all the time. Interest rates are not intended to be down at 1-2%, or even near zero as the Fed maintained them for many years. Yields at current levels are actually much closer to the norm of the past 50 years than not. By the way, one of the other factors related to the $39 trillion of debt is that about $10 trillion will roll over this year. As lower yielding debt matures, and has to be renewed at higher rates, the interest expense of the government goes up, eating up more of the budget. And this becomes a self-fulfilling prophecy.

This debt isn’t going away any time soon. Not only are markets dealing with the volatility of the on-again, off-again tariff dictums from Trump and Company, but there is tremendous uncertainty over tax policy, as the Republican leadership grapples with trying to extend the tax cuts that were enacted in 2017 which are ending this year, while also adding giveaways such as no tax on tips for service workers, or no tax on overtime for certain workers. Let’s not fool ourselves. Neither party is truly interested in cutting spending. Or if they are, it’s always going to be, “Hey, leave my district alone, I’ve got voters to worry about.” Spending cuts are fine, as long as they are for someone else. And therein lies the problem.

I’ve no idea how this will play out with markets, but my sense is that markets are going to force a reckoning with spending. And other than higher yields for fixed income, that’s not a recipe for a good stock market environment. In my opinion, expectations should be tempered, and that’s backed up by where we stand within long term trends (see below).

The Long Term Trend

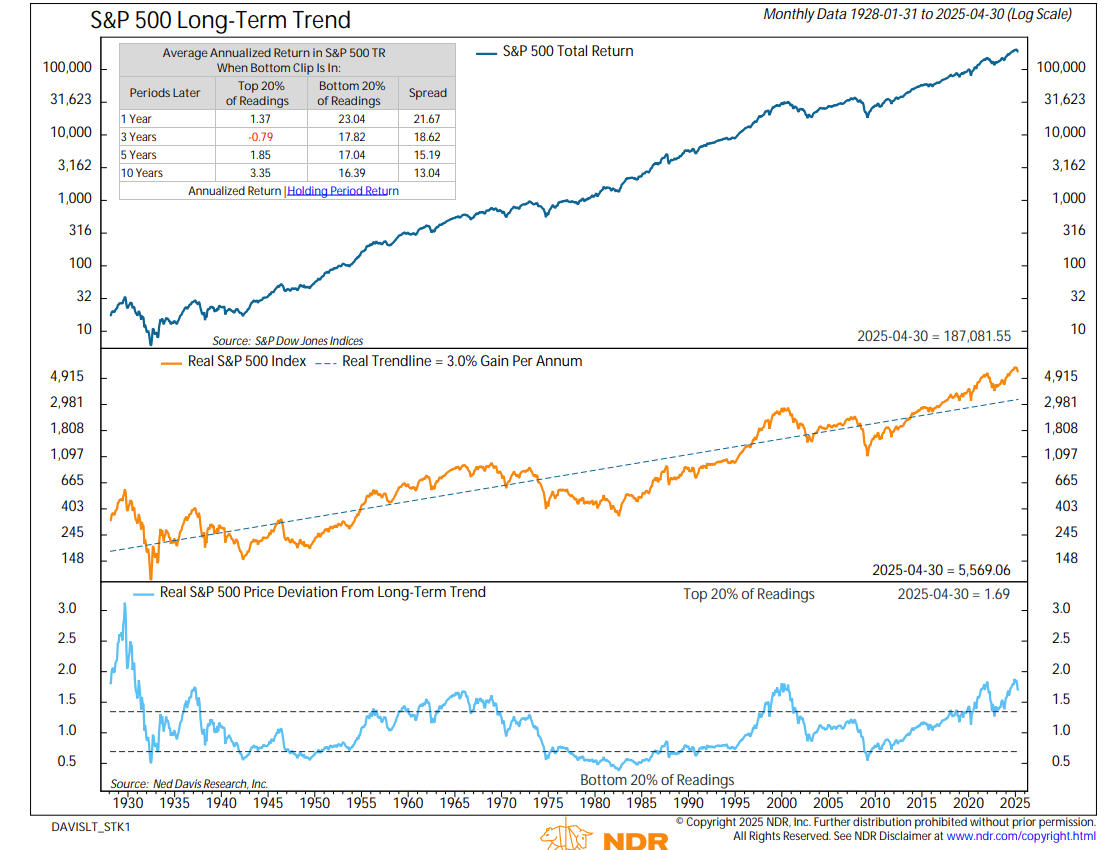

As we and others have continually emphasized, long-term valuation measures are not very helpful for timing, but they do put in perspective the amount of risk one is taking. It’s a fact that since 1926, the S&P 500 has compounded at about 10% per annum, but that is nearly a 100-year time frame, with the benefit of hindsight. Markets move in cycles, and from 2009 to 2024, the S&P 500 has compounded at near 16% per annum. That’s 60% above trend. If you believe in mean reversion (and I do), it suggests stocks could be in the beginning stages of a long road to nowhere, or at least below average returns. Witness the chart below, also courtesy of Ned Davis Research.

In the chart, the middle clip shows the long term trendline of the S&P 500 Index with a 3% real trendline growing at 3% per annum. As shown in the table in the top clip, when the market is trading in the bottom 20% of historical readings, future returns from 1 year to 10 years out are way above average, at some 60% to 70% above the norm. The last such undervalued reading was in 2009, and the market has behaved accordingly. But the opposite is true when in the top 20% of readings, as we are now, and have been since around 2020. Other than from 1925 to 1929, this indicator has never been so stretched, with estimated returns 10 years out in the 3-3.5% range, which is in line with other valuation models we track. That is why we like investment grade bonds in the 4.5% range looking out 2 to 3 years as a compliment to tactical equity exposure.

With the on-again, and now mostly off-again tariff news, volatility has been the norm for stock markets the first five months, with the S&P 500 down nearly -17% from its February 19 peak at the low on April 8, and the NASDAQ off more than -20%. Now, through data from May 13, below is how the various indexes have performed year-to-date:

S&P 500 + 0.49%

NASDAQ 100 +1.00%

S&P Midcap 400 -1.57%

S&P Smallcap 600 -5.96%

Vanguard Total International Stock Fund +11.86%

For some perspective, we calculated the return of the Vanguard S&P 500 Index Fund from December 31, 2008 to December 31, 2024 and then compared it to the Vanguard Total International Index Fund for the same period. The returns have made investors and professionals wonder aloud, “Should we really be allocating money to international equities?” The results are 14.5% compounded against 6.5%, for 16 years! But the first four plus months of 2025 have been quite different, with an 11% edge to international. I can’t know that the cycle has changed for a long time. There’s simply no way to know that. It is why we keep 25% of international equity exposure in our Passive Index mix, but we don’t do that in our main tactical accounts. Rather, we rely on relative strength and only on April 1 did our measures shift enough to move equity exposure to the international space. Sometimes, these trends last for months, and at other times, they last for years. This one, much like the argument for value stocks vs growth stocks, has a chance to be the latter. We’ll see.

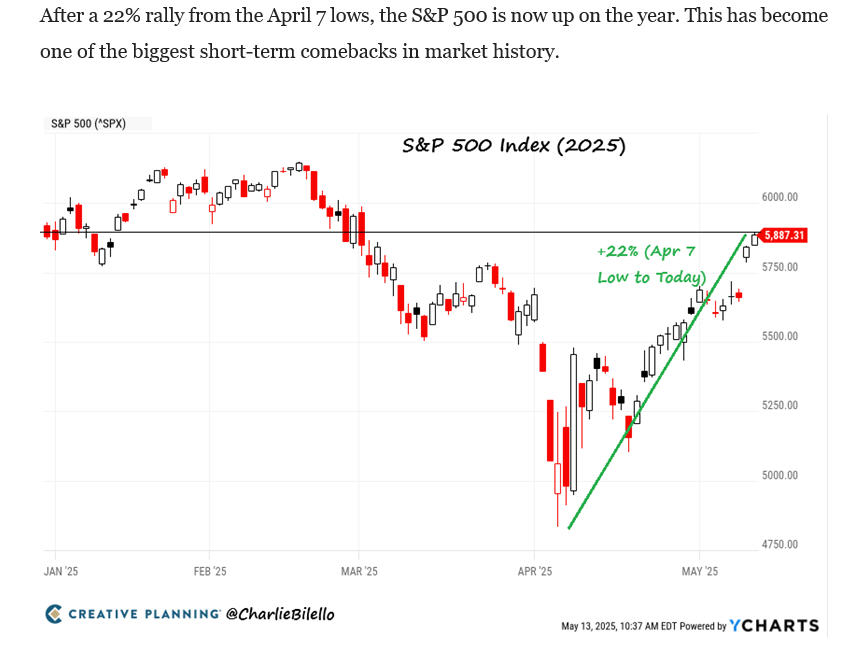

Trust The Thrust, Or Bear Market Rally

As the chart below shows, courtesy of CreativePlanning@CharlieBilello, the stock market has experienced a massive rally off of the April 8 lows, nearly unprecedented.

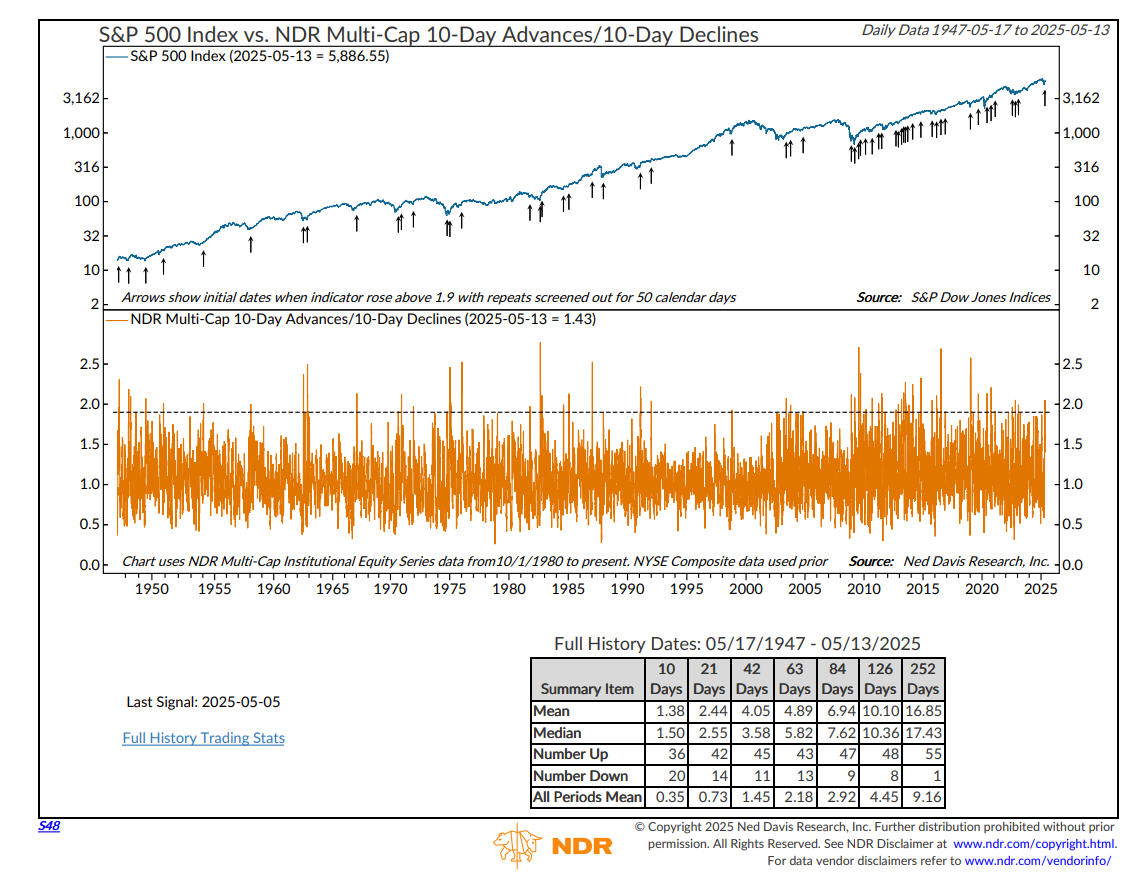

With this powerful surge, a number of breadth thrust signals have fired, which have had positive significance in the past. Our friends at Ned Davis Research monitor several iterations, and one of them below has been perhaps the most reliable in data going back to 1947. It measures the ratio of 10-day advancing stocks to 10-day declining stocks, using the NDR Multi-cap stock universe. When the ratio exceeds 1.9 on a 10-day basis, a Thrust is indicated. See the chart below.

Looking at the summary table at the bottom of the chart, there have been 56 prior signals since 1947, and one year later, 55 of them have resulted in gains, with the mean at nearly 17%. That’s 70% above norm, and statistically significant. Furthermore, Davis put together five different thrust indicators, all which have a history going back to 1980 (not quite as much data). Using 12 different thrust measures, when at least five of them have fired within a particular time frame, the results have been gains going out 1 year in 28 of 28 cases, again with mean performance at over 21% per annum. With all of this evidence, it may appear that the worst is behind us, and there’s smooth sailing ahead.

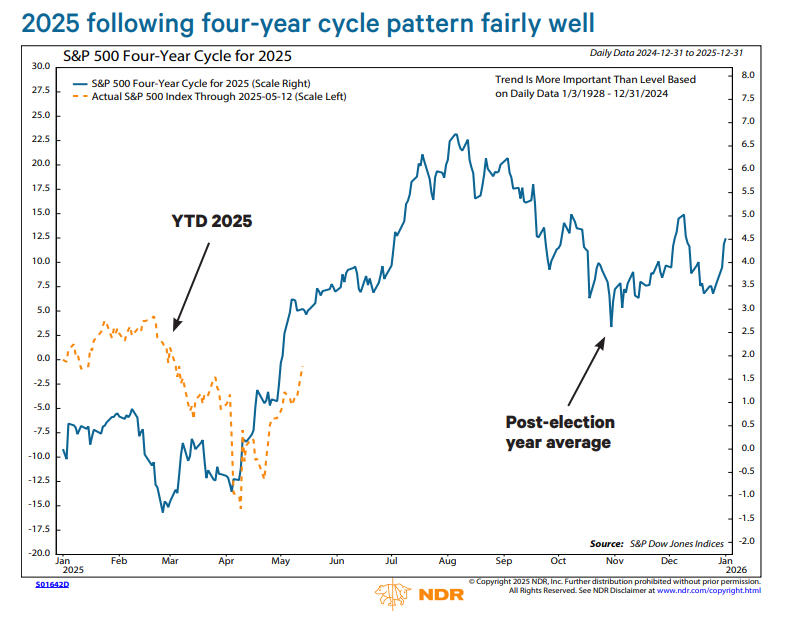

However, further analysis shows that with one of the Thrust measures, known as the Zweig Breadth Thrust, named after famous analyst Marty Zweig, nearly 50% of the cases had a test of the lows within 3 months before heading higher. Despite this historical evidence, this could also just be a very strong bear market rally, where stocks fail to make new highs and ultimately, fall back. The updated S&P 500 Cycle Composite, shown below, also courtesy of NDR, shows a rally likely peaking in late June, followed by weakness into October.

The bear market rally case has a decent precedent, as cited by Sam Stovall, the chief investment strategist at CFRA. He wrote last week that “nearly 2/3 of all bear markets since WWII started with double-digit declines that recovered to within 2% or higher of the 200-day moving average only to reverse course and dive once again to set an even lower low.”

Portfolio Allocations

At present, I would characterize our positions as “high neutral.” Three of our five stock market risk models are positive, which dictates about 60% tactical equity exposure, and bolstering those odds are that our high yield bond risk model flipped back to a BUY signal on Monday, May 5, and that trade is off to a good start. I’m not betting on, though, another trade in that asset class that lasts 17 months like the last one.

The Decision

No, this section is not about LeBron James declaring on national television in July 2010 that he was leaving the Cleveland Cavaliers to join the Miami Heat to chase an NBA Championship. Rather, it’s about Daniel Kahneman, one of the world’s most accomplished thinkers, who was a psychologist at Princeton University, won the Nobel Prize in economics and wrote the best-selling book, “Thinking, Fast and Slow,” which was first published in 2011 and is essential reading in every front office in professional baseball.

Kahneman passed away on March 27, 2024, and in a poignant piece in the Wall Street Journal, writer Jason Zweig chronicled what happened to his dear friend. The link to that article is below.

https://www.wsj.com/arts-culture/books/daniel-kahneman-assisted-suicide-9fb16124

Kahneman emailed his closest friends, and told them he was saying goodbye, and was on his way to Switzerland to end his life. Many of his friends are still struggling to come to grips with his “decision.” But in Zweig’s article, Kahneman gives clues to his thinking. Below are several quotes that were in his email.

“I have believed since I was a teenager that the miseries and indignities of the last years of life are superfluous, and I am acting on that belief.”

“I am still active, enjoying many things in life (except the daily news) and will die a happy man. But my kidneys are on their last legs, the frequency of mental lapses is increasing, and I am ninety years old. It is time to go.”

“I discovered after making the decision that I am not afraid of not existing, and that I think of death as going to sleep and not waking up. The last period has truly not been hard, except for witnessing the pain I caused others. So if you were inclined to be sorry for me, don’t be.”

In the final section of the article, Zweig poses some very interesting and difficult questions.

Zweig wrote, “As death approaches, should we make the best of whatever time we have left with those we love the most? Or should we spare them, and ourselves, from as much as possible of our inevitable decline? Is our death ours alone to own?

“Danny taught me the importance of saying “I don’t know.” And I don’t know the answers to those questions. I do know the final words of his final email sound right, yet somehow feel wrong: “Thank you for helping make my life a good one.”

These issues are quite personal, and perhaps a bit different for everyone. I do feel we are all shaped by our experiences. I have no problem sharing with you my own thoughts. Having witnessed my mother and her two sisters deteriorate and spend their final years in a nursing home with memory issues, I have no interest in repeating that scenario for our children. Do I have a choice? I hope so. And I do feel our death is ours to own. I would want to spare my loved ones from my inevitable decline. In my perfect world, I would love to emulate Warren Buffet, who is still mostly sharp in his early 90s, yet recognizes it’s time. But I also realize not everyone who reaches their 90s is in a strong physical and mental condition. With Zweig’s question, I think we should do both—make the most of our time with friends and family, but also spare them from our decline.

In his death, and his story, Kahneman makes us think, again. How ironic.

Material Of A Less Serious Nature

With permission, from Harley Schwadron

A good old Alabama boy won a bass boat in a raffle drawing. He brought it home and his wife looks at him and says, “What are you going to do with that?”

“There ain’t no water deep enough to float a boat within 100 miles of here.” He says, “I won it, and I’m going to keep it.”

His brother came over to visit several days later. He sees the wife and asks where his brother is?

The brother heads out behind the house and sees his brother in the middle of a big field, sitting in a bass boat with a fishing rod in his hand.

He yells out to him. “What are you ‘doin?” His brother replies, “I’m fishin’. What does it look like I’m doin’?

His brother yells, “It’s people like you that give people from Alabama a bad rap, makin’ everybody think we’re stupid.”

“If I could swim, I’d come out there and whip your ass!”

Spring is definitely in play, with temperatures now hitting 100 here and there (ok, not everywhere). School will conclude for most everyone in the next four weeks. So, in that realm, I’m going to close a bit differently than normal. In late April, our daughter Caroline, who is a sophomore at Cal Poly San Luis Obispo and on their dressage team for the second year, competed in the National Equine Championships once again (she won Grand Champion last year in her novice division).

That’s her above. The team finished 5th in the nation in their division, and in the team competition on Friday, with Caroline competing as an individual where her scores are combined with the team, she finished 2nd of 12 riders. Needless to say, as you can see below, she was one happy camper.

It’s so awesome to see your kids excel at something they love. Way to go girl. You’ll see a smile just as big on me if my Dallas Stars continue their magic through the Stanley Cup playoffs, and win the Stanley Cup. Go Mikko and Miro and Roope and Mikael and Thomas and Otter and Johnny! Oh well, I lost you there unless you consult the roster.

As always, thank you for your continued trust and confidence in all of us at TABR.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.