No, Thank You, I Don’t Think So, I Think I’m Smellin’ a Rat

Those words are part of the chorus of Don Henley’s song “No, Thank You” from his Cass County album which debuted last October. I think they succinctly sum up this Presidential Election, with Hillary and Donald recording the highest disapproval ratings in history. Here are two snippets of Henley’s song:

These are hard times we’re living in, Nobody cuts you any slack. We got Space Age machinery, Stone Age emotions, Today a man had better watch his back.

Everybody’s selling somethin’, the baron and the bumpkin, A man has got to fight for what is his. If what they’re offering to you looks too good to be true, You can bet your bottom dollar that it is

No, thank you, I don’t think so, I think I’m smellin’ a rat, Don’t tell me what you’re gonna do for me, ‘Cause I’ve been there, done that.

Later in the song, he goes on to say:

B.S. blaring from the radio, the TV, Hot wind blowin’ off the Hill. It’s a mystery to me we can’t agree to disagree, It’s lookin’ like we never, ever will.

Like a drunkard in the night, swingin’ left and swingin’ right, Republican or Democrat. Well, I ain’t got no love for none of the above, cause I’ve been there, done that.

We’re not about to tell anyone how to vote, but I did come across some good wisdom this past week on this topic that would benefit anyone. It came from John Wesley, an Anglican cleric and Theologian who in October 1774 gave a sermon on politics. He said back then, “I met those of our society who had votes in the ensuing election and advised them this way:

- To vote without fee or reward for the person they judged most worthy

- To speak no evil of the person they voted against, and

- To take care their spirits were not sharpened against those that voted on the other side

Thanks to Biola Communications Professor Tim Muehlhoff for the illustration.

The Election Impact on Markets

I’ve stated before that we think that Federal Reserve policy is more important to the financial markets than who wins the Presidency, and nothing has changed in that assessment. Right now, the Fed is expected to raise rates at their December meeting, and though that may not be the nail in the coffin to the stock market, it is not going to help (but it needs to be done).

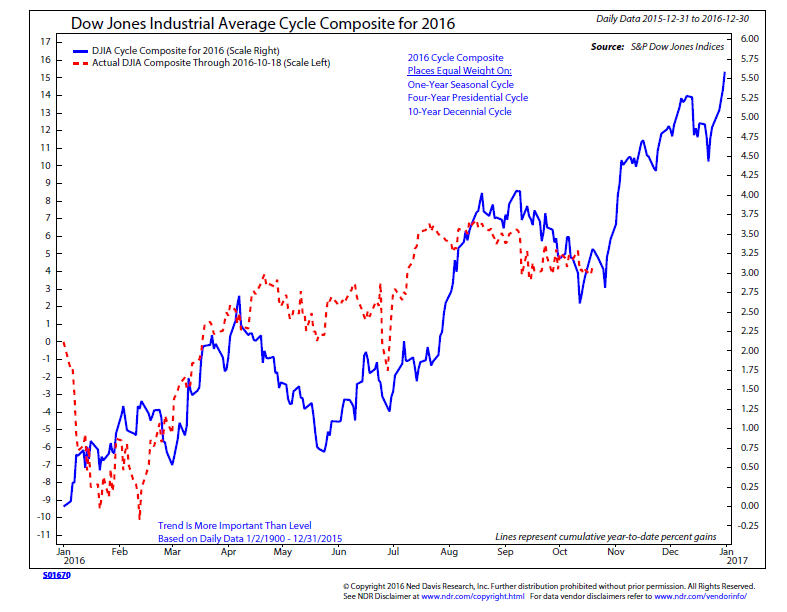

The good news is we are about to enter the strongest seasonal period for stocks, which mostly runs from November to April. The Cycle Composite for 2016 from Ned Davis Research (shown below), suggests that stocks should be bottoming now, and mostly rising until January.

Given that we’ve recently seen confirmation of price highs with most breadth indicators, along with corporate high yield bonds continuing to make new highs, I suspect the narrow trading range of the past few months will eventually yield to an upside breakout. We’ll see.

Investment Allocations Update

There’s been little change in this area. Tactical equity allocations remain at about 64%, and we expect this will increase to 76% in the next week or so, as our seasonal risk model will be turning positive. Our real estate model remains on its March BUY signal, though prices have weakened in the last month with the backup in yields, as the 10-year Treasury note has jumped from a low of 1.39% to 1.74%. As mentioned above, high yield bonds are making new highs and our risk model remains on its February BUY signal. We added to positions in this area about one month ago, and are now nearly 70% invested, certainly with a dose of regret for not being fully invested.

Overall, the sum message from our stock and bond risk models is that of a moderately positive environment. It does not appear time to leave the party yet.

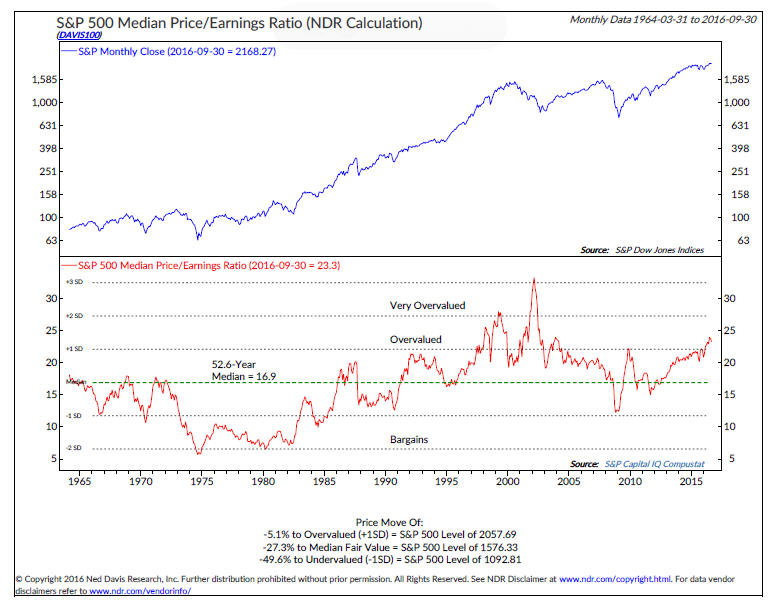

Valuation Headwinds

We’ve mentioned many times that stock market valuation tools are terrible timing indicators. But, eventually, they do (and will) matter. One measurement below, also courtesy of Ned Davis Research, is the median Price/Earnings Ratio of the S&P 500.

The data goes back to 1964, and the current reading is at 23.7, while the 52 -year median is just under 17. Just to get back to fair value, the S&P 500 would need to fall by nearly 30%. That is likely to happen at some point. But who knows, maybe the PE goes to 27 first, as it has done twice before since 1998. Remember, anything can happen in the stock and bond markets.

Material of a Less Serious Nature

I couldn’t resist, so this month, you get two political jokes. You’re guaranteed to laugh, no matter who you’re voting for.

Hillary and Donald are in a life raft out in the middle of the Atlantic Ocean. Who survives?

………..THE UNITED STATES!

And, now here’s number two. Once upon a time there was a king who wanted to go fishing. He called the royal weather forecaster and inquired as to the forecast for the next few hours. The weatherman assured him that there was no chance of rain in the coming days.

So, the king went fishing with his wife, the queen. On the way, he met a farmer on his donkey. Upon seeing the king, the farmer said, “Your majesty, you should return to the palace at once because in just a short time I expect a huge amount of rain in this area.” The king was polite and considerate, and replied “I hold the palace meteorologist in high regard. He is an extensively educated and experienced professional. And besides, I pay him very high wages. He gave me a very different forecast. I trust him and will continue on my way.”

So, he continued on his way. However, a short time later a torrential rain fell from the sky. The King and Queen were totally soaked and their entourage chuckled upon seeing them in such a shameful condition.

Furious, the King returned to the palace and gave the order to fire the professional. Then, he summoned the farmer and offered him the prestigious and high paying role of royal forecaster. The farmer said, “Your Majesty, I do not know anything about forecasting. I obtain my information from my donkey. If I see my donkey’s ears drooping, it means with certainty that it will rain.”

So, the King hired the donkey. Thus, began the practice of hiring dumb asses to work in the government and occupy its highest and most influential offices. The practice continues to this day.

By the way, if you’re wondering who I’m voting for. . . . .it’s MADISON BUMGARNER!

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.