A 1000 Dow Points Ain’t What She Used To Be, And Lessons From Howard Marks

We’ve come a long way, baby. No, I’m not referring to the 1978 ballad by the same name performed by Loretta Lynn. I’m talking about the Dow Jones Industrial Average, which first crossed the 1,000 level in November 1972. Today, nearly 49 years later, it sits comfortably above 33,000.

We’ll touch on the milestones in-between, and why percentages, and not points, are a preferred measuring stick. We’ll also summarize the lessons we took away from an interview last month with legendary distressed debt investor, Howard Marks, who is well known for his insightful writing in his role as Co-founder and Chairman of Oaktree Capital Management.

1,000 Point Milestones In The Dow Jones Industrials Are No Longer Meaningful

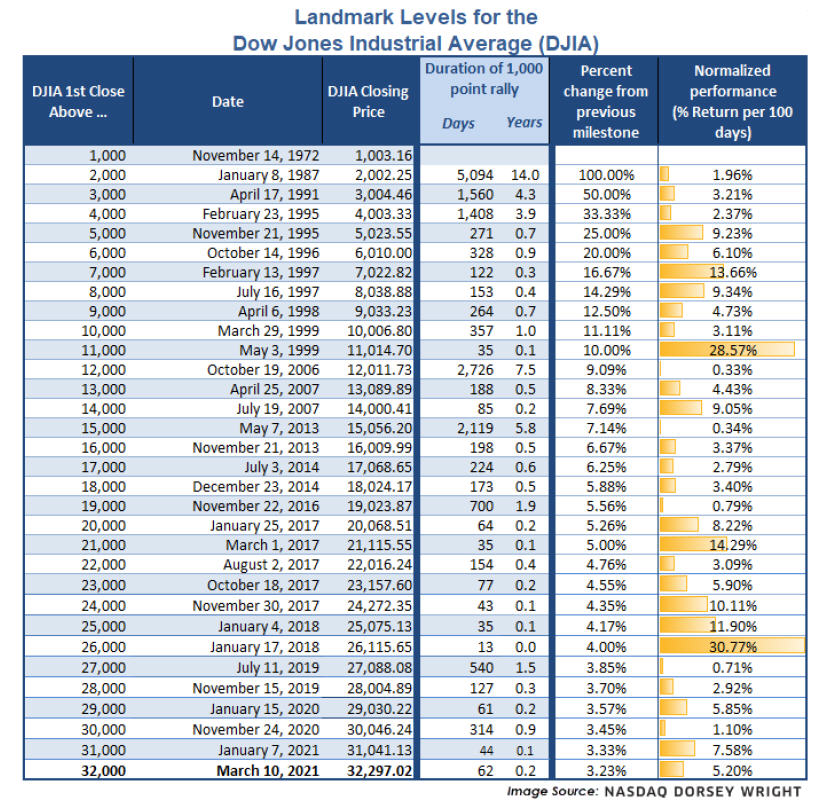

In November of 1972, the Dow Industrials crossed above the 1,000 level for the first time in its history. It would take nearly 15 years for it to gain the next 1,000 points, in January 1987. That doesn’t sound so impressive, does it? That’s only 5% annually, compounded. It’s important to note, though, that is looking at the nominal price level of the Dow, and does not include dividends. In December of 1972, we found data that showed the S&P 500 was yielding about 2.7% at that time, and the S&P 500 and Dow Jones have correlated fairly well over time. Today, that yield is about 1.4%, having peaked back in 1981 at 5.36%. My, how times have changed.

As you’ll see in this math exercise, it was a lot more difficult for the Dow to gain the next 1,000 points in 1972, which involved a doubling, than it is today, sitting above 33,000. To achieve an equivalent accomplishment today, the Dow would need to cross above the 66,000 level. Someday, that will happen, but who knows when? For me, that was the take-away I got from the study that my friends at Dorsey Wright produced last month, which is shown below.

In the study shown above, they outlined each 1,000 point milestone, along with the date the move occurred, plus the number of days it took to rally from the previous milestone, along with the percent move. As the math implies, it takes bigger gains to reach the increments starting at lower levels (4,000 to 5,000 requires a 25% move) than now, when a gain of just over 1,000 points could move the average from 33,000 to 34,000. In fact, that could even happen in one day. More likely, though, the move to 66,000 will take place over a period of years. If it happened in 10 years, it would imply a compound return of 7.2% (look up the rule of 72), but again, remember, the computation of the Dow that is reported each day does not include reinvested dividends.

The truth is, we really have no idea how long it will take, do we? What stood out for me were the two very lengthy periods nestled in the middle of the table. The Dow first crossed the 11,000 level in May of 1999, only to find it would take 7 1/2 years to gain the next 1,000 points. That was due to the bear market which began in March 2000, which lasted until March 2003. Likewise, the Dow would first cross the 14,000 level in July 2007, only to require nearly 6 years to achieve the next milestone, thanks to the bear market which commenced in October 2007 and ended in March 2009.

In the context of those two bear markets, investors have been spoiled during the last 8 years, in that there have been very few declines, and the one that was certainly significant last March due to the pandemic, was over in a flash, with a recovery nearly as fast as the decline. The table above is a reminder that market cycles can be very different, and are unpredictable. I should note that after the table above was produced, it took the Dow only 7 days to go from above 32,000 to 33,000, that taking place on March 17. Much like the past, at some point one of these milestones will last for years, not days or months.

Lessons From Howard Marks

Since its inception in 2012, I’ve been involved as an equity board member for the Titan Capital Management senior level finance class at Cal State Fullerton, where students are learning real-world skills in analyzing companies and markets, learning critical thinking and writing and then applying those skills in the management of what today is approximately $2 million of the University’s endowment, which consists mostly of equity and fixed-income securities.

Each year, myself and other board members and outsiders may lecture to the students on a variety of topics, to add to what they are learning from their respective professors. As a result, I’m always on the alert for possibilities that might enhance the students experience, such as two years ago when I was able to arrange with my contacts at PIMCO an entire afternoon session at their headquarters in Newport Beach. In that light, I’ve been reading Howard Marks’ books and memos for many years, and thought, hey, his firm is based in Los Angeles, why not ask him if he would be willing to speak to the class? That was four years ago, and things didn’t mesh with his schedule, since he was spending much of his time on the East Coast. A few months ago, I reached out again thinking a Zoom meeting with the class might be easier, and presto, we had a date. Last month, armed with questions submitted by students of the class, I was able to interview Howard in a sort of fireside chat format for one hour, with about 40 students, faculty, board members and class alumni listening and Zooming in.

Howard Marks Co-Founder and Chairman of Oaktree Capital Management

In listening to a replay of the interview, I took over two pages of notes, and below, I’ve summarized the lessons I came away with.

History doesn’t repeat. The cycles are all different. The fact that something happened in the past doesn’t mean it will happen again. You can’t extrapolate patterns from the past, but we don’t have any other reference point to go on. If something has never happened before, you can’t say you know how it will turn out. By the way, a good example of that is last year’s stock market decline caused by the pandemic (Bob speaking).

The easiest way to get in trouble investing is to have the belief you know what’s going to happen, and to bet heavily. That’s how they carry you out. It’s much better to have an approach such as “Here’s what I believe will happen, but I don’t know, and here’s what could go wrong.” See the recent blowup of Archegos Capital as an example of this.

One of the biggest lessons from the pandemic was how fast psychology can change, and how little you know. The Fed has nearly unlimited powers, and seemingly can produce almost any outcome they want. This cycle is not an ordinary cycle. It came from the outside. It was an exogenous cause. The recovery in both the economy and markets has come from the Fed (the government). What are the ramifications of this? Inflation? Rising interest rates? Lower stock prices? That’s unanswerable. We don’t know.

Regarding the nascent trend of interest in ESG investing (environmental, social, governance), which is much more prominent in Europe than in the United States, Marks noted that an advisor’s fiduciary responsibility is to the client, not the planet. Is ESG investing profitable? Who knows? Is it relevant to the future if the conditions are different?

No rule always works. The investing environment is dynamic. To have superior results, you need an edge. If information is readily available to everyone, where’s the edge? You have to do a better job of analyzing the data, or better at imagining the future, or have superior insight. Simple knowledge of the facts can’t be the answer. In the 1970s and 1980s, if you wanted to research a company, you had to write a letter requesting a copy of the annual report, and you might get it back in 3 weeks. Today, that same information is instantly available on your computer.

We closed the session talking about reading and books, and perhaps the favorite thing I took away from the session was his comment about “if you can live with ambiguity, it is very interesting.” One of his recent favorite books is Annie Duke’s Thinking in Bets: Making Smarter Decisions When You Don’t Have All The Facts. And finally, he offered one of his favorite quotes to the students from American journalist Christopher Morley. “There is only one success. To be able to spend your life in your own way.” Marks went on to add “Play to your strengths, avoid your weaknesses, figure out what makes you happy, and do it.”

Howard has authored two books, The Most Important Thing—Uncommon Sense For The Thoughtful Investor (there’s a revised edition of this), and Mastering The Market Cycle—Getting The Odds On Your Side. He’s well known for his investor memos, which he publishes semi-regularly when he has something useful to say, and below is a link to his writings for those who are interested.

https://www.oaktreecapital.com/insights/howard-marks-memos

The Many Benefits Of Reading by Bob Veres

Preface by Bob Kargenian

I am a big believer in reading hard-cover books and newspapers every day (yes, print newspapers!). Monday to Friday we get the Los Angeles Times, Orange County Register, USA Today and Wall Street Journal in print, plus Saturdays with Barron’s and Investor’s Business Daily, along with the Wall Street Journal weekend edition. I also read the NY Times online each day, mostly just scanning for things of interest, along with a subscription to The Athletic, to keep up with all of my sports teams (note–the best $59 a year you’ll ever spend!). When I came across this piece from financial planning writer Bob Veres, I had to pass it along.

“In this day and age, it seems like reading is becoming a thing of the past, what with podcasts, TED talks and YouTube videos becoming more popular vectors of information and entertainment. But a growing body of scientific literature suggests that reading actual books may be more important than we realize for enhancing certain parts of our brains and delaying the onset of dementia.

The research is still in the early stages, but when they scanned brain waves, the scientists found that when you read about a character playing tennis, areas of your brain light up as if you were physically out there on the court yourself. When you read about fictional characters very different from yourself, it boosts areas of your brain associated with emotional intelligence, which help you understand what others are thinking by reading their emotions. Researchers also found that deep reading, when you get really absorbed in a book, builds up our ability to focus and grasp complex ideas.

Just learning to read, as a child, has profound impacts on brain development, creating a specialized area in your left ventral occipital temporal region, increased verbal memory and thickening your corpus callosum, which is the information highway that connects the left and right hemispheres of your brain. Exposure to vocabulary through reading leads to higher scores on general tests of intelligence for children.

Research published in Neurology also suggests that regular reading may slow the inevitable decline in memory and brain function as we age. Frequent brain exercise—deep reading, but also playing chess or working puzzles—was shown to lower mental decline by 32 percent. And people who engaged in brain exercise were 2.5 times less likely to develop Alzheimer’s disease than those who were not.

Anything else? A 2009 study by researchers at Sussex University found that reading can reduce stress by as much as 68 percent. Losing yourself in a thoroughly engrossing book can help you escape the worries and stresses of the everyday world, by participating in the domain of the author’s imagination.

The bottom line is that reading isn’t just a way to cram facts into your brain, no matter what your high school teachers may have told you. It’s a way to continuously rewire your brain to become more effective and efficient, to strengthen your ability to imagine alternative scenarios when you make decisions, to remember details and think through complex problems. It doesn’t just make you more knowledgeable—you can get that from a TED talk. Reading makes us all functionally smarter.”

Sources:

https://www.inc.com/jessica-stillman/reading-books-brain-chemistry.html

https://www.realsimple.com/health/preventative-health/benefits-of-reading-real-books

A Large Number Of New Highs Is Typically Bullish

As somebody once said, the most bullish thing the stock market can do is go up. And it continues to do that, with several market indexes making new highs last week. One of the breadth measurements we follow is the number of stocks making new highs on the NYSE during uptrends, and the number of stocks making new lows during downtrends. Stocks have been in an uptrend since late March of last year, and a few weeks ago, the number of stocks making new highs reached 511 on March 11. That is the largest number of new highs since May 2013. That is illustrated on the chart below, courtesy of the McClellan Market Report.

When the number of stocks making new highs keeps expanding as market indexes make new highs, this is considered confirmation of the market uptrend, and past history suggests the market will continue higher until fewer stocks stop participating in the rally. When a series of fewer highs takes place, a negative divergence takes place which is quite common at a market top. The lead time for these divergences can be a few months to over one year, and in rare cases, there’s no lead time. Dorsey Wright published some research showing the past occurrences with at least 500 stocks making new 52-week highs, and that table is shown below.

There have been only 8 prior cases in the past 40 plus years. You can see that going one year out, every occurrence showed a gain, with median returns of over 15%, well above the norm for all one-year periods. As noted above in the section on Howard Marks, no rule works all the time. We can’t know what will happen in the next 11 months, and I should note the S&P 500 is already up 4.8% since March 11, so some of the gains have already been pulled forward, but it’s encouraging that this version of market breadth is still giving off good vibes.

Tax Deadlines And Other Minutiae

In case you’ve been under a rock, the IRS has extended the deadline for most individual taxpayers to May 17, and until June 15 for taxpayers in Texas, Oklahoma and Louisiana. By default, this extends the deadline for funding IRA contributions and other actions to May 17. I should note, however, that for those taxpayers who make estimated tax payments (like myself), the deadline for the first installment for 2021 is April 15, which is this Thursday. Don’t get the tax return filing deadline confused with the deadline to make estimated tax payments. I also wanted to note a key opportunity for any of you (or your children) who have been laid off over the past year. The recent American Rescue Plan which was passed by Congress has a benefit where one can adopt employer-based health insurance coverage from their prior employer under COBRA, which will be available for free from April 1 to September 30, as employers will be eligible for a payroll tax credit to directly offset the cost of the COBRA.

For those of you who use a CPA or other tax preparer, do them a favor and get all your data to them. Don’t expect these deadlines to be extended every year.

Portfolio Allocations

Since last month, the one stock market risk model that had flipped negative went back to positive, so equity allocations within tactical accounts are back to being 100% fully invested, all concentrated in small cap, microcap and midcap ETFs. Our risk model for high yield corporate bonds made a new yearly high this past weekend, and that model has been bullish since November 9. Sentiment has been exceedingly optimistic for weeks and months, but stocks keep advancing. This is why sentiment indicators, much like valuations indicators, are not necessarily good for timing. At some point, the evidence will change, but at present, all of our work is in a positive mode, which has been the case for the better part of six months and beyond.

Material Of A Less Serious Nature

With Disneyland having been closed for over one year (note—I can see the Matterhorn from my 13th story office window), and now set to re-open, much to the delight of millions of people, including our 16-year old daughter, I thought it would be appropriate to share a little Disney humor. We all need to laugh. . .more.

Mickey Mouse was deep in the middle of a terrible divorce from his wife, Minnie. As he was speaking to the judge regarding their separation, the judge cuts him off. “I’m sorry, Mickey, I am not able to legally separate you two. I cannot do it based on the grounds that you have confirmed to me that Minnie is mentally unstable.”

Frustrated, Mickey retorts, “No, no, no. I didn’t say Minnie was mentally unstable. I said Minnie was F@#*ing Goofy!”

In the spirit of full transparency, all of us at TABR have either been vaccinated with the J&J version (one shot) or are awaiting their second booster. We’re seeing clients regularly, in the office, or at lunch or breakfast meetings, to each person’s comfort level and we’re excited to be able to see so many of you in person for the first time in over one year. The fight is not over with COVID, and who knows, as more knowledge is acquired, we may all be dealing with an annual COVID shot in the future, much like the current flu shot. It sure seems like we’ll be in a better place by the end of June, with hopefully another 100-150 million Americans getting the vaccine by then. Here’s to normalcy, sooner rather than later. The only thing better than baseball being back with limited fans would be baseball back with a stadium full of people. Oh, guess I forgot. They already did that. . . .in Texas!

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

Inverse ETFs

An investment in an Inverse ETF involves risk, including loss of investment. Inverse ETFs or “short funds” track an index or benchmark and seek to deliver returns that are the opposite of the returns of the index or benchmark. If an index goes up, then the inverse ETF goes down, and vice versa. Inverse ETFs are a means to profit from and hedge exposure to a downward moving market.

Inverse ETF shareholders are subject to the risks stemming from an upward market, as inverse ETFs are designed to benefit from a downward market. Most inverse ETFs reset daily and are designed to achieve their stated objectives on a daily basis. The performance over longer periods of time, including weeks or months, can differ significantly from the underlying benchmark or index. Therefore, inverse ETFs may pose a risk of loss for buy-and-hold investors with intermediate or long-term horizons and significant losses are possible even if the long-term performance of an index or benchmark shows a loss or gain. Inverse ETFs may be less tax-efficient than traditional ETFs because daily resets can cause the inverse ETF to realize significant short-term capital gains that may not be offset by a loss.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.