As We Start the Year: A Few Thoughts on Retirement, Risk, Medicare, and Gratitude

As the new year begins, many people naturally find themselves reflecting—on where they live, how well protected they are, and whether they’re set up properly for what’s ahead. Year-end articles, rankings, and headlines tend to amplify those questions, sometimes in ways that are more unsettling than helpful.

In this month’s newsletter, I’d like to share a few observations that have come up repeatedly in recent conversations with clients. None of these are urgent or require immediate action. But all are worth thinking about as part of a thoughtful, long-term planning process.

“Best Places to Retire” Lists — A Different Perspective

Every year, a new round of “Best Places to Retire” lists makes the rounds. They’re fun to share, easy to scan, and often leave many of us with the same reaction: Are we missing something?

Earlier this year, Bob Kargenian and I were meeting with clients when the topic of “Best Places to Retire” lists came up. We pulled up a couple of them online and noticed that California cities were mostly absent from the top of the rankings.

One recent list by WalletHub ranked the top retirement destinations in the U.S. using factors like affordability, activities, healthcare access, and overall quality of life. Notably, there wasn’t a single California city in the top 25.

At first glance, that can feel discouraging. California is expensive, and these lists seem to confirm it. But it’s worth taking a step back and understanding what these rankings are actually measuring — and what they’re not.

Most of these lists are heavily weighted toward cost-based metrics, which makes sense on one level. Housing prices, property taxes, state income taxes, and general affordability dominate the scoring systems. When affordability is such a significant input, high-cost states like California and others are effectively disqualified before the analysis even begins.

That doesn’t mean the lists are “wrong,” but in practice, many of these lists are answering a narrower question: where retirement is most affordable based on a defined set of metrics. For many people, that’s not the same as asking: Where do I want to live?

There’s a reason cities and towns in California don’t rank well on affordability — and it’s the same reason they’re expensive in the first place. People want to live there. Climate, natural beauty, cultural amenities, healthcare access, walkability, and proximity to family all play a role. When demand is high and supply is limited, prices rise. That’s not a flaw in the system; it’s basic supply and demand.

It’s also important to remember that retirement isn’t just a financial decision. It’s a lifestyle decision. Most of the clients we work with aren’t seriously considering moving to a lower-cost city halfway across the country. They’re not comparing Laguna Beach to Bismarck or Santa Barbara to Sioux Falls and weighing the pros and cons. They’ve already made a lifestyle choice — consciously or not — and the financial plan is designed around that reality.

These lists can still be useful if they spark gratitude rather than comparison. They can serve as a reminder that while your hometown may come with higher costs, it also offers qualities many people value enough to pay for. Retirement planning isn’t about “winning” a ranking. It’s about aligning where you live with how you want to live, and making sure your finances support that choice.

Why an Umbrella Insurance Policy Matters More Than Most People Think

Insurance isn’t a particularly enjoyable topic, which is probably why umbrella policies are so often overlooked. They’re easy to ignore, rarely discussed, and only seem relevant when something goes wrong.

Earlier this year, a client was involved in a car accident that is likely to result in a lawsuit, and it quickly became clear that their existing auto insurance limits may not be sufficient. Unfortunately, they did not have an umbrella policy in place. Situations like this are a sobering reminder that even responsible, careful people can face liability risks that extend well beyond standard coverage — and why an umbrella policy can play such an important role in protecting assets that took years to build.

An umbrella insurance policy provides additional liability coverage above and beyond your auto and homeowners insurance. If you’re involved in a serious accident or lawsuit and the damages exceed the limits of your underlying policies, an umbrella policy is designed to step in. For example, if a contractor, landscaper, or other worker is injured while working at your home and suffers a serious injury, medical costs and potential legal claims can exceed the liability limits of a standard homeowners policy, leaving your personal assets exposed without umbrella coverage.

What surprises many people is how frequently standard policy limits can be exceeded. Auto accidents involving serious injuries, multi-vehicle collisions, or pedestrians can lead to claims well beyond typical coverage levels. And lawsuits don’t just target income. They target assets, putting your entire net worth at risk.

While we don’t sell insurance or receive compensation related to insurance products, we believe it’s important to help you stay aware of potential risks and discuss whether appropriate coverage is in place.

Major publications have written about the rise in large personal liability claims and the growing gap between standard insurance coverage and real-world legal exposure. One common theme across these articles is that umbrella policies are relatively inexpensive for the amount of protection they provide, particularly for households with significant savings or investment assets.

A common misconception is that umbrella coverage is only for the wealthy or the reckless. In reality, liability exposure has less to do with lifestyle and more to do with what’s at stake, and anyone with meaningful assets has something worth protecting. Even careful drivers and homeowners can find themselves in situations where liability claims escalate quickly.

That’s where an umbrella policy can come in. They’re essential to protect your assets, and they’re also surprisingly affordable, with an average cost of $383 per year for $1 million of coverage.

Umbrella insurance isn’t about expecting something bad to happen. It’s about acknowledging that risk exists even when you’re responsible, cautious, and insured. Much like estate planning or long-term care decisions, it’s a form of risk management designed to protect what you’ve already built.

As part of a broader financial plan, insurance decisions should be revisited periodically — especially as assets grow, lifestyles change, or coverage limits remain static while potential liabilities increase.

Medicare Help Is Expanding — and We’ll Help You Navigate the Right Resource

Medicare decisions have become increasingly complex over the years. Plan options, enrollment timing, supplemental coverage, prescription drug considerations, increased IRMAA premiums, and ongoing changes make it difficult for many people to know where to start or who to trust.

Recently, Fidelity announced that it is expanding its Medicare-related services, adding another option if you’re looking for information and support as you approach Medicare eligibility or reassess existing coverage.

While additional resources can be helpful, more options don’t always make decisions easier. Medicare isn’t one-size-fits-all, and the “best” solution depends heavily on individual circumstances, health considerations, and preferences.

Over the years, we’ve worked with a Medicare specialist, Steve Lujan, who has helped many of our clients navigate these decisions. He understands the nuances, stays current on changes, and focuses on helping people make informed, practical choices rather than pushing a particular product.

Going forward, whether you’re interested in Fidelity’s new Medicare resources, prefer working with an independent expert like Steve, or simply want help understanding the landscape, our role is the same: to help connect you with the right resource for your situation.

If you have upcoming Medicare decisions — whether you’re nearing age 65 or reviewing existing coverage — please let us know. We’re happy to help point you in the right direction.

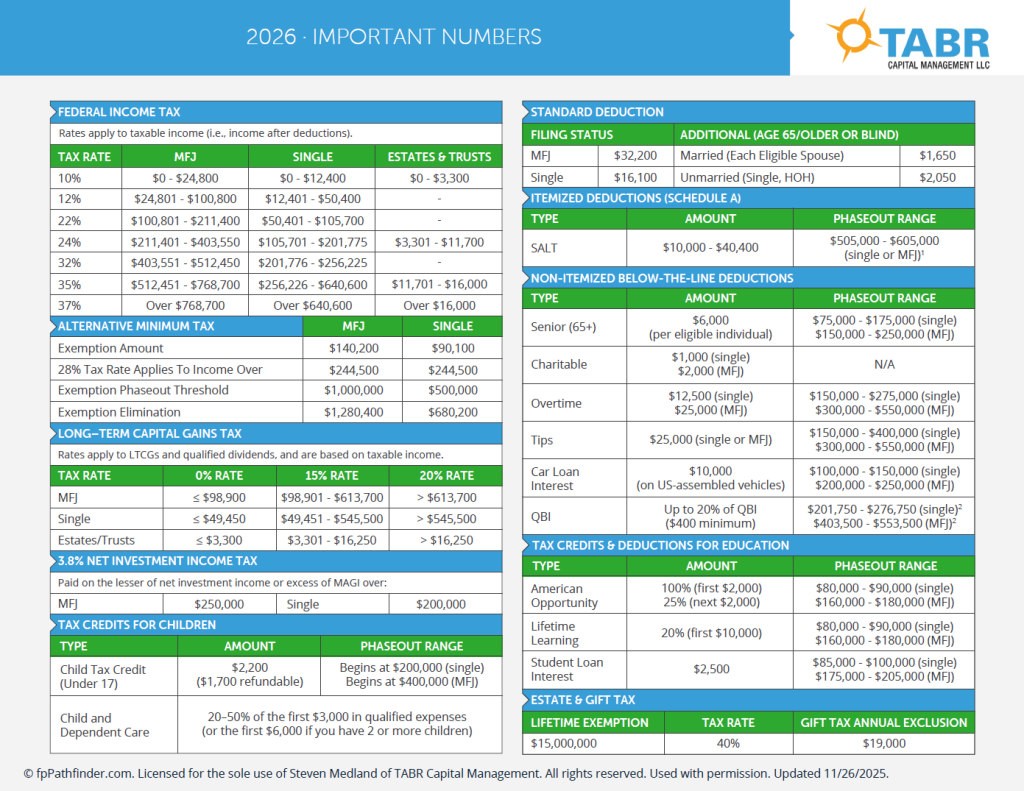

Important Numbers to Keep in Mind in 2026

As we start the year, we wanted to share a two-page reference that many clients find helpful to keep handy.

Attached below is a summary of key financial planning and tax numbers for 2026, including income tax brackets, capital gains thresholds, retirement plan contribution limits, Social Security and Medicare figures, estate and gift tax limits, and more. While not all of these numbers will apply to everyone, having them in one place can be useful when thinking about planning decisions throughout the year.

This document isn’t meant to encourage action on its own, and it certainly doesn’t replace personalized planning. Instead, think of it as a reference point — something to bookmark or save for those moments when a question comes up, and you want quick context around current limits and thresholds.

If you have questions about how any of these numbers apply to your specific situation, or if you’d like to talk through planning opportunities for the year ahead, please don’t hesitate to reach out.

Portfolio Allocations

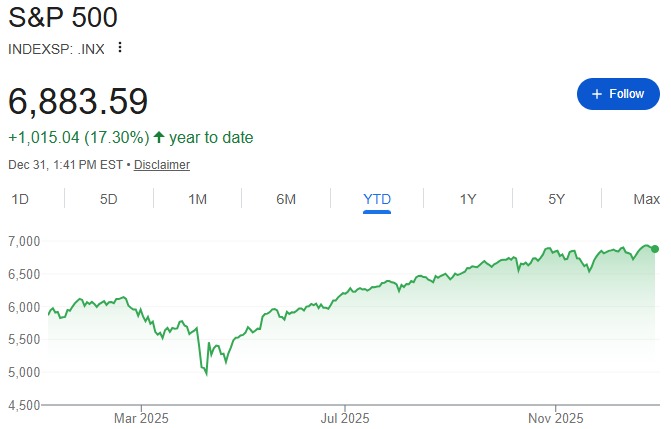

We haven’t made any changes to our portfolio allocations since Bob Kargenian wrote last month’s newsletter about four weeks ago.

Our tactical equity allocations remain 100% invested in stocks, as all five of our stock market risk management models are still in positive mode. In addition, our high yield bond risk model remains bullish, as it has been since its May 2025 BUY signal.

A few days after Bob’s update, the Federal Reserve did, in fact, lower interest rates by 0.25% to its current range of 3.5% to 3.75%. Since then, the stock market has moved very little overall and is ending the year near record highs.

Bob will provide a more detailed market update, along with updated annual performance numbers, in the next newsletter.

A Year-End Thank You from TABR

As we close out the year and look ahead, I want to take a moment to say thank you.

Trust is not something we take lightly. Allowing us to be part of your financial life — your planning decisions, your questions, and your long-term goals — is something we’re deeply grateful for.

This work is ultimately about people and families, and the lives behind the numbers. It’s a privilege to work with thoughtful clients who value perspective, planning, and long-term thinking.

On a personal note, this past year has been a reminder of how important family and time together are. Like many families, ours has evolved over the years, and the holidays are a meaningful opportunity to slow down and appreciate that. The photo below was taken on Christmas morning with Izzie and all four kids — a moment we were grateful to share together as the year came to a close.

As 2026 begins, all of us at TABR — Bob, Sylvia, Jamie, and I — wish you and your family a happy, healthy, and fulfilling year ahead. Happy New Year, and thank you, as always, for your continued trust and confidence.

Best regards,

Steven W. Medland, MBA, CFP®

Partner

TABR Capital Management, LLC (“TABR”) is an SEC-registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure website (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs, and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore, the performance shown is net of TABR’s investment management fees, and also reflects the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes, and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services, and it is not known whether the clients referenced approve of TABR or its services.