Bob’s Retirement Plan. And New All-Time Highs Likely

There are a multitude of things we do at TABR. Managing money. College funding and planning. Social Security and pension decisions. Life insurance coverage. One of the biggest areas and commonalities is retirement planning. We’re usually the ones asking the questions, but TABR will celebrate its 20th anniversary in February of 2024.

Steve Medland and I are just a bit older (sic) than when we started the firm in 2004. It’s a fair question to ask, “So, Bob, when are you going to retire?” In a monthly update earlier this year, I promised to address this topic later in the year. Here we are. Read on for that narrative.

Meanwhile, stocks and bonds have been on a tear since the first of November. Momentum suggests even higher prices lie ahead, but after that, risks abound.

The State Of TABR

According to the Oxford Language Dictionary, retirement is defined as “the action or fact of leaving one’s job and ceasing to work.” By that description, I can tell you it won’t be happening any time soon. A dear friend, who also happens to be the best branch manager I ever worked with (that’s you, EW), told me a year ago at breakfast one morning, “Bob, you’ll never retire. You love what you do too much.” And, perhaps he is right.

I’ve been fascinated with markets since I was in public relations with the Angels, and I’ve been fortunate to have found a career that is as interesting and exciting as professional and college baseball, with way better financial rewards if one is good at what they do. I’m inspired by several friends and clients who are still working in their 70s and even 80s, and are better at what they do than ever before. They work not because they have to, but because they want to, and love what they do. They continue to serve people at a very high level. I think that’s fantastic.

I suspect my thinking would change a bit should grandchildren come into the picture, but that’s not on the horizon at present with our son, Adam, 29, traveling the world in his music/photography career, and daughter Caroline, 18, just beginning her college journey. And wife Michelle isn’t exactly pining for me to be home more, as she’s full on in her own journey, which you’ll be reading about next summer.

Besides the on-going challenge of the financial markets, the best part of our job are the many relationships with clients and others in our industry, some of which go back 35 years or more. It’s so gratifying to help and serve others. And candidly, we have advantages at this stage that we didn’t have many years ago and that a majority of advisors don’t have. It’s called perspective, which only comes with living through and learning from the biggest bull market in modern history, from 1982 to 1999, followed by the biggest bear market, from 2000 to 2009.

With many of our clients having just retired or being already retired, our process and disciplines of risk management are probably more important than ever before. Why not use our experience of the past 40 years to help them, and their children? At some point, I suspect a reduced role may be appropriate, such as working a few days a week instead of full-time, but still allowing for the on-going regular interactions with clients. Steve Medland and myself want the business to be sustainable, and that means bringing on board a third advisor to train in our process and methods. The dilemma is who, and when, and in what role.

I will have to update how I think of myself and my role, and what things I can give up, and other things that are non-negotiable. There are a few ways to go, such as finding an existing advisor who has some experience, versus finding a suitable candidate for example from the finance departments of Cal State Fullerton or UC Irvine and training them from the ground up. I can tell you this—in college, they can teach you financial acumen, but that is worthless without personability and empathy. People want to do business with people they like, and who are relatable. It should be assumed one has the financial knowledge, but I can also attest there are a lot of lousy advisors in our business (just as in any profession—lousy teachers, lousy doctors, lousy police officers, and on and on).

At present, Steve and I are in the midst of deciding whether or not to extend our lease (which expires in May 2024) for another 3 years, or another 5 years. When we add a third wheel, we think it would be nice to have a bit more space, but a lot of it is in how the space is configured. We have some wasted space in our location in Orange on the 13th floor, where we have been continually since May 2004, but the space that might be available may not meet our needs (too much, or too little). The shorter lease gives us an earlier out to explore things, where the longer one gets us a better deal where perhaps we try to change some things in our current space. We’ll see.

One of the main things I want to convey is what we have told many clients who have pondered their own retirement. We practice what we preach. And that is, you better have something to keep you busy and engaged. Otherwise, you’ll go downhill in a hurry. Of course, good health helps. So far, I’ve had pretty good luck in that department. Several years ago in one of our monthly updates, I did a piece on the Living To 100 website (www.livingto100.com), where you can put in all of your personal health information and it spits out your probably life expectancy. At that time, my “score” was 92. I’ve not done one since, but probably should. I don’t necessarily want to live that long, unless I have my full faculties and all.

Besides TABR and our kids, I continue to be heavily involved at Cal State Fullerton, where I graduated in 1981. I serve on our Baseball Leadership Committee which meets regularly with our coaches and athletic director and advancement director, where we deal with many areas that pertain to our baseball program. I continue to serve as an Equity Board member for Titan Capital Management, our senior level finance class where the students are managing about $3.5 million of the University’s endowment, applying principles they are learning in class. We review buy and sell reports, interact with our professors and dean and help mentor and teach on certain topics that augment what they are learning in class.

Finally, I continue to serve on the Finance & Investment Committee which oversees the University’s $135 million endowment. When not traveling, I usually run in the mornings five of every seven days, and besides countless books and magazines, I read four print newspapers Monday through Friday, five in print on Saturday, along with the digital version of the NY Times and The Athletic. See # 4 below.

Last week, we took our kids to New York City and among other things, saw Billy Joel perform at Madison Square Garden. He’s 74. Besides his 36 year-old daughter from Christie Brinkley, he also has two young girls, 8 and 6, who sang a Christmas song with him at the show. Hey, there’s an idea, Michelle! Did he walk a bit slower than normal? Yes. But, he was fantastic. In two weeks, we’re going to see the Eagles in Los Angeles for their final, final time. Both Don Henley and Timothy B. Schmitt are 76. They are making the best music of their lives. Why not help people, until you can’t?

In that vein, several weeks ago, long-time Wall Street strategist Byron Wien passed away at the age of 90. At Morgan Stanley, Wien became famous for his annual prognostications. In his most recent role at Blackstone, he was trying to get on a conference call just a couple of weeks before he died, being active until the end. Several years ago, he was about to present at a conference, which typically is targeted towards market views. But the organizer thought the audience would be more interested in hearing what Wien had learned in his career. So, he came up with a list, and then having seen such a positive response, added to it over time and updated it. Besides # 4, be sure to read # 20. Below are Byron Wien’s 20 Life Lessons, courtesy of Blackstone.com.

I was scheduled to speak about the world outlook at an investment conference in 2012, and shortly before my time slot, the conference organizer said the audience was more interested in what I had learned over the course of my career than what I had to say about the market. I jotted a few notes down and later expanded and edited what I said that day. Others have since encouraged me to share my thoughts with a broader audience. In the decade since, I have come back to them time and again to test their resonance and staying power, and find them still broadly applicable.

Here are some of the lessons I learned in my first 80 years, which I continue to practice as I enter my 90’s.

- Concentrate on finding a big idea that will make an impact on the people you want to influence. The Ten Surprises, which I started doing in 1986, has been a defining product. People all over the world are aware of it and identify me with it. What they seem to like about it is that I put myself at risk by going on record with these events, which I believe are probable and hold myself accountable at year-end. If you want to be successful and live a long, stimulating life, keep yourself at risk intellectually all the time.

- Network intensely. Luck plays a big role in life, and there is no better way to increase your luck than by knowing as many people as possible. Nurture your network by sending articles, books and emails to people to show you’re thinking about them. Write op-eds and thought pieces for major publications. Organize discussion groups to bring your thoughtful friends together.

- When you meet someone new, treat that person as a friend. Assume he or she is a winner and will become a positive force in your life. Most people wait for others to prove their value. Give them the benefit of the doubt from the start. Occasionally you will be disappointed, but your network will broaden rapidly if you follow this path.

- Read all the time. Don’t just do it because you’re curious about something, read actively. Have a point of view before you start a book or article and see if what you think is confirmed or refuted by the author. If you do that, you will read faster and comprehend more.

- Get enough sleep. Seven hours will do until you’re sixty, eight from sixty to seventy, nine thereafter, which might include eight hours at night and a one-hour afternoon nap.

- Evolve. Try to think of your life in phases so you can avoid a burn-out. Do the numbers crunching in the early phase of your career. Try developing concepts later on. Stay at risk throughout the process.

- Travel extensively. Try to get everywhere before you wear out. Attempt to meet local interesting people where you travel and keep in contact with them throughout your life. See them when you return to a place.

- When meeting someone new, try to find out what formative experience occurred in their lives before they were 17. It is my belief that some important event in everyone’s youth has an influence on everything that occurs afterwards.

- On philanthropy, my approach is to try to relieve pain rather than spread joy. Music, theatre and art museums have many affluent supporters, give the best parties and can add to your social luster in a community. They don’t need you. Social service, hospitals and educational institutions can make the world a better place and help the disadvantaged make their way toward the American dream.

- Younger people are naturally insecure and tend to overplay their accomplishments. Most people don’t become comfortable with who they are until they’re in their 40’s. By that time, they can underplay their achievements and become a nicer, more likeable person. Try to get to that point as soon as you can.

- Take the time to give those who work for you a pat on the back when they do good work. Most people are so focused on the next challenge that they fail to thank the people who support them. It is important to do this. It motivates and inspires people and encourages them to perform at a higher level.

- When someone extends a kindness to you write them a handwritten note, not an e-mail. Handwritten notes make an impact and are not quickly forgotten.

- At the beginning of every year think of ways you can do your job better than you have ever done it before. Write them down and look at what you have set out for yourself when the year is over.

- The hard way is always the right way. Never take shortcuts, except when driving home from the Hamptons. Shortcuts can be construed as sloppiness, a career killer.

- Don’t try to be better than your competitors, try to be different. There is always going to be someone smarter than you, but there may not be someone who is more imaginative.

- When seeking a career as you come out of school or making a job change, always take the job that looks like it will be the most enjoyable. If it pays the most, you’re lucky. If it doesn’t, take it anyway, I took a severe pay cut to accept each of the two best jobs I’ve ever had, and they both turned out to be exceptionally rewarding financially.

- There is a perfect job out there for everyone. Most people never find it. Keep looking. The goal of life is to be a happy person, and the right job is essential to that.

- When your children are grown or if you have no children, always find someone younger to mentor. It is very satisfying to help someone steer through life’s obstacles, and you’ll be surprised at how much you will learn in the process.

- Every year, try doing something you have never done before that is totally out of your comfort zone. It could be running a marathon, attending a conference that interests you on an off-beat subject that will be populated by people very different from your usual circle of associates and friends, or traveling to an obscure destination alone. This will add to the essential process of self-discovery.

- Never retire. If you work forever, you can live forever. I know there is an abundance of biological evidence against this theory, but I’m going with it anyway.

Current Momentum Suggests New Highs Ahead. After That, Who Knows?

For much of this year, it seemed the stock market was being dominated by 7 stocks, the largest components in the S&P 500. Since the October 31 low, however, that’s no longer the case, as the rally has broadened out to include virtually all styles, though I will say international stocks continue to lag U.S. stocks by a wide margin. Look at the gains in the five areas noted below, from the close on October 31 to the close on December 27.

S&P 500 Index (large stocks) +13.99%

Nasdaq 100 Index (large tech) +17.30%

S&P 600 Index (small caps) +23.80%

S&P 400 Index (mid caps) +18.50%

Vanguard Total Int’l Index +11.90%

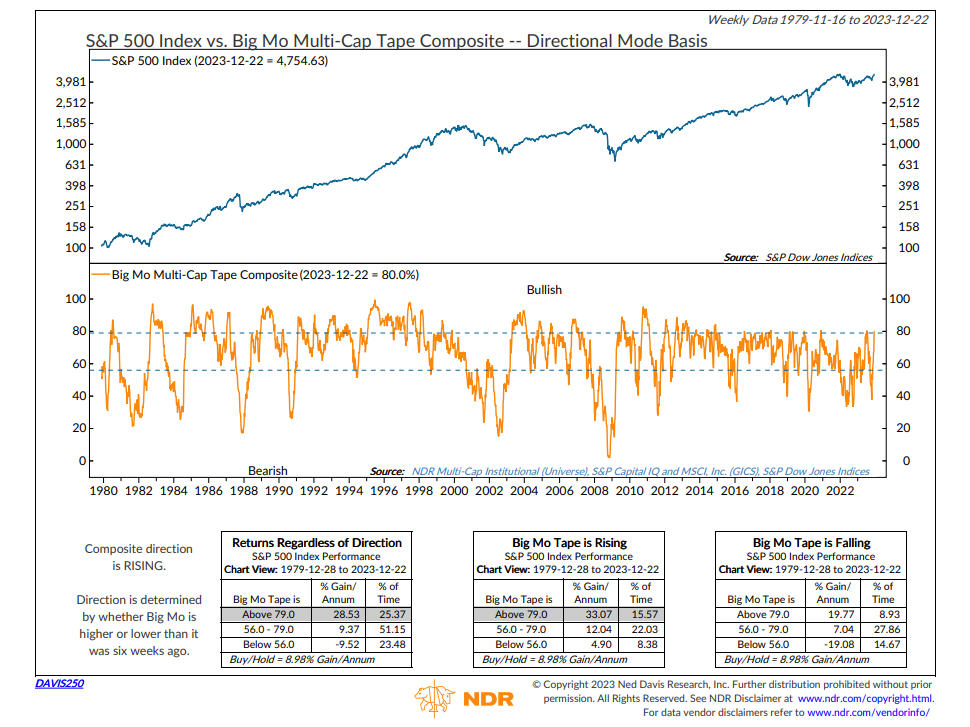

This broad participation is confirmed by an indicator Ned Davis Research maintains, called their Big Mo Tape Composite. It measures weekly the percentage of sub-industries in uptrends. A chart is below, courtesy of our friends at NDR (www.ndr.com).

Last week, the indicator reached the 80% level, one of the highest readings in 10 years. This is pretty rare territory, with the market in this mode only 25% of the time since 1979. Here’s the message. When the market is this strong and broad, a peak in stock prices rarely takes place. It’s typical that a series of lower highs in this measure and others would take place in coming months before the final peak in price. This is why we think prices are likely to eventually head higher during the first quarter.

However, the charts below suggest prices have been pulled forward, and a pullback seems likely starting very soon. Below is the weekly chart of the SPY (S&P 500 ETF). This is courtesy of www.decisionpoint.com.

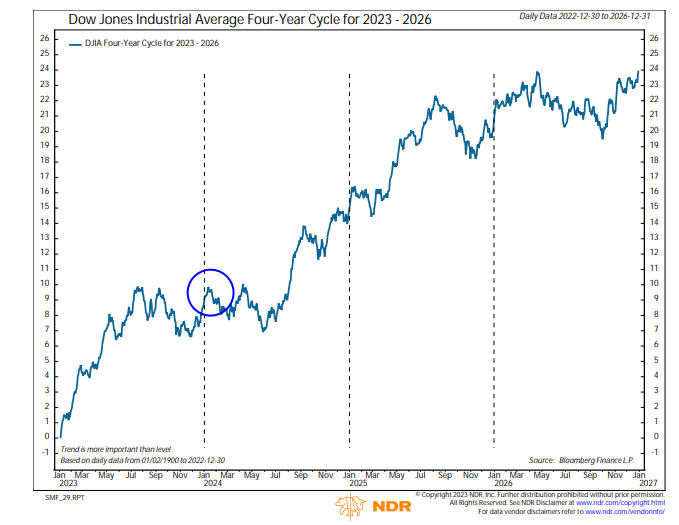

The warning from this chart is that the RSI Indicator (top clip) has just reached the 70 level. That’s not an automatic sell since there really aren’t any divergences yet, as there were in late 2021 (see bottom clip of the PMO, which is the Price Momentum Oscillator). But, stocks are definitely overbought here. The second warning is coming from the 4-year cycle, which correctly called for a year-end rally, but is now peaking, per the chart below from Ned Davis Research.

If the cycles are correct, stocks should have trouble making progress through much of the first half of 2024. This wouldn’t be surprising, as the rally of the past two months has flipped sentiment from pretty pessimistic to wildly optimistic. How much more good news can there be? We’ll find out soon enough.

Our positioning in client accounts remains nearly fully invested, with 5 of our 6 stock market risk models in a positive mode, dictating about 83% tactical exposure, along with being fully invested in high yield bond funds since early November. We’ll have more on stock market valuations and fixed income in our January update, along with a summation of 2023. Bond yields have dropped over 100 basis points in just about 7 weeks. This has been great for bonds, which were almost uniformly negative for the year in late October, but it also means future returns will be lower from here.

The TABR Christmas Card And Shutterfly

A quick administrative note. For those of you who received our annual Christmas card, we became aware (from mailing one to ourself!) that many if not all of the cards were delivered with an address, but no name. Shutterfly told our staff they made a printing error due to their volume of business, apologized, and credited us 50% of the cost of the shipment. So, please know, we intended to put your name on it!

Material Of A Less Serious Nature

A girl asks her boyfriend to come over for dinner. The girl tells her boyfriend that she would like to do it for the first time. The boy is ecstatic, but he has never done it before. So, he goes to the pharmacist to get some protection.

The pharmacist helps the boy for over an hour and tells the boy everything there is to know about protection. At the register, the pharmacist asks the boy whether he would like the 3 pack, the 10 pack or the family pack. The boy picks the family pack, because he thinks he will be really busy since it is his first time.

The boy shows up at the girl’s house and she takes him to the dinner table, where his family is sitting. The boy quickly offers to say grace and bows his head. A minute passes and the boy is still in deep prayer, with his head down. This continues for 5 minutes and there is no movement. Finally, the girl leans over and whispers, “I had no idea you were so religious.” The boy whispers back, “I had no idea your father was a pharmacist.”

Yes, life is full of surprises, and there promises to be more of them in 2024. We hope that you enjoyed a Merry Christmas and Happy Hanukkah and will be ringing in the New Year. With tragic wars going on in the other side of our world, I came across some verses from my favorite Christmas song, O Holy Night, that sum up my wish.

Truly He taught us to love one another

His law is love and His gospel is peace

And in His Name

All oppression shall cease.

Thank you for the trust and confidence you place in all of us at TABR, and for allowing us to serve you.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.