BULL-IEVE It or Not?

Our last monthly email was published on Monday, June 27, which in hindsight, turned out to be the conclusion of the two-day selloff in global stock markets associated with the United Kingdom Brexit vote.

In those two days, the S&P 500 fell nearly 6%, but has since rebounded nearly 9%, to a new all-time high. The rally has been broad-based, with small, midcap and international indexes also gaining between 9 and 11% from the low. A number of momentum indicators have generated strong thrust signals, a couple of which we’ll outline below. Historically, though the number of occurrences are limited, past results have tended to be bullish for stocks.

Think of a rocket ship with boosters. The boosters generate a tremendous amount of thrust to lift the rocket off the launching pad, and even after the boosters have flamed out, the rocket keeps on going, not just from its own engines, but from the momentum. When upside momentum such as this takes place in the stock market, it has typically lasted several months.

The 10-day Average of the Advance/Decline Ratio

Many technical analysts track this indicator, which is a 10-day simple average of advancing stocks versus declining stocks. One will get different results when using different thresholds, but most analysts focus on when the ratio rises to 1.9 to 1 or higher. The table below is taken from Dan Sullivan’s Mutual Fund / ETF Letter. Sullivan restricts his signals to when the ratio rises to a 2 to 1 margin or more.

| Signal Date | 3 months | 6 months | 12 months |

| 07/13/1949 | 7.85% | 13.63% | 14.03% |

| 11/20/1950 | 8.47 | 8.03 | 12.01 |

| 01/25/1954 | 7.92 | 18.29 | 36.71 |

| 01/24/1958 | 0.60 | 10.30 | 32.26 |

| 07/11/1962 | -0.42 | 14.62 | 20.51 |

| 01/16/1967 | 4.01 | 5.87 | 5.14 |

| 12/04/1970 | 10.07 | 13.00 | 4.85 |

| 01/10/1975 | 18.59 | 32.35 | 40.01 |

| 01/06/1976 | 10.51 | 10.70 | 12.28 |

| 08/23/1982 | 11.27 | 23.08 | 33.85 |

| 01/14/1987 | 10.71 | 21.93 | -5.84 |

| 02/05/1991 | 5.50 | 7.20 | 16.83 |

| 03/23/2009 | 7.03 | 25.37 | 40.03 |

| 07/12/2016 | ? | ? | ? |

| Average | 7.85 | 15.72 | 20.21 |

Using Sullivan’s criteria, there have only been 13 prior signals since 1949, and only one of those resulted in lower prices one year later, that being a near -6% loss following the 1987 occurrence. The data above is based on using the Dow Jones Industrial Average.

In a similar study, Ned Davis Research (NDR) uses a criteria of 1.9 to 1. A similar signal was generated on July 11, using this ratio. They have data going back to 1947, and with a little less stringent criteria, there have been 47 prior cases. Interestingly, 25 of these took place from 1947 to 2002, while 22 have occurred since 2003, perhaps due to the increased use of ETFs and high frequency trading. But, the message is similar, in that the vast majority of outcomes have tended to be positive.

According to NDR’s study, looking out 252 days later, 43 of the 44 prior cases that have been completed have resulted in gains, with the only loss the same one as in Sullivan’s study above. The median gain was just over 17%. When looking out 126 days later, 39 of 45 completed signals have shown positive results, with a median gain of 10.5% and the largest loss being -13.3% in 2011.

Market Implications

There are never guarantees with markets, only probabilities. Minimal declines are hallmarks of momentum thrusts. Applying this to the S&P 500, the old high of 2130 now becomes support. The index currently sits at 2170. There should not be a decline of more than 3% to 5% in the next three months if there is to be another bullish outcome.

On the positive side, the advance/decline line has confirmed the recent high, and major tops usually have a divergence similar to the one in May 2015. We are watching crude oil and high yield bonds. Crude oil has quietly declined over 20% since early June, now sitting at $40. Corporate high yield bonds also rallied sharply off the stock market Brexit lows, but have rolled over a bit in the past week while stocks have gone sideways. This bears observation, as divergences between high yield and the stock market have typically been good warnings of future trouble for stocks.

The Fed and the Election

Despite the chatter last week from Fed Chairwoman Janet Yellen that an interest rate hike could be on the table for their September meeting, that is very unlikely to happen. Though the stock market is at or near its high, the Fed is quite data dependent, and the economic reports continue to show very slow growth. Since the Fed is terrified of spooking financial markets, even with a minuscule 25 basis point increase, the likelihood is the Fed will not do anything until after the election. I suspect they don’t want to be accused of interfering with the outcome, and the odds are stocks will decline after the next increase in rates, whenever that may happen.

If an increase is to come in the Fed Funds rate, my guess is that it will take place after the election, in December. I’m certainly hoping for an increase, for the sake of bond and money market yields, but we’ll have to see.

Speaking of the election, investors may get a clue as to whether Hillary or Donald will win, by observing the performance of the stock market from August to October. Though limited in scope from a statistical standpoint, in 19 of 22 prior cases, when stocks gained in this three month period prior to the election, the incumbent party won. In English, if stocks are up, the odds are with Hillary, and if they’re down, the odds are with Donald.

Investment Allocations

Our stance with portfolios should be considered moderately positive. Tactical equity exposure is at 65%, with another 3-5% in real estate, and our corporate high yield bond model remains on its February 29 buy signal. So, we are participating in the advance, but are not fully invested. Holding us back from increased exposure are seasonal considerations and an interest rate model. The TABR Dividend Stock account is 80% invested.

What’s Not to Like?

Though the short term technical condition of the market is mostly bullish, not everything is hunky dory. The New York Composite Index, made up of nearly 3200 companies (in comparison to the S&P 500) is below where it was in July 2014, along with the Dow Transports and international stocks as represented by the Vanguard Total International Index Fund. In addition, the Russell 2000, a representative small company index, is barely above its July 2014 levels.

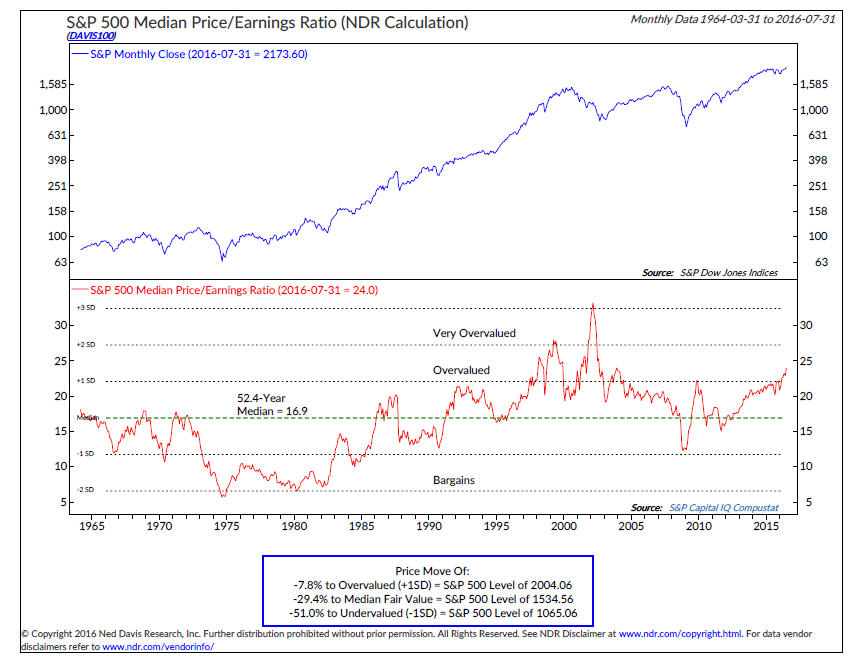

The fundamental valuations of stocks, using various methods, suggest a very expensive market relative to history. Below is a chart courtesy of Ned Davis Research, showing the S&P 500 and its Median Price Earnings Ratio.

Using this study, stocks would need to decline almost 8% just to get to overvalued territory, which is defined as 1 standard deviation above the 52-year median. To get to the median would require a decline of nearly 30%. As I have noted many times before, fundamental valuation indicators are almost useless for timing, but they are helpful for risk and historical context. From a historical perspective, stocks have only been this expensive three prior times—1929, 2000 and 2007.

At some point, what investors pay for stocks will matter, but as we’ve noted above, the technicals are presently mostly positive. When that evidence changes, risk will be on a different level.

Material of a Less Serious Nature

Conjoined twins walk into a bar in Toronto and park themselves on two bar stools. One of them says to the bartender, “Don’t mind us; we’re joined at the hip. I’m John and he’s Jim. Two Molson Canadian beers, draft please.”

The bartender, feeling slightly awkward, tries to make polite conversation while pouring the beers. “You fellas been on vacation lately?”

“Off to England next month,” says John. “We go to England every year, rent a car and drive all over the place, don’t we, Jim?”

“Ah, England!” says the bartender. “Wonderful country, the history, culture and especially the beer.”

“Nah, we don’t like that British crap,” says John. “Hamburgers and Molson’s, that’s for us, eh Jim? We can’t stand the English people either, they’re so arrogant and rude.”

“So why keep going to England?” asks the bartender.

John replies: “Gives Jim a chance to drive. . . ”

Thanks, as always, for reading this far. I know—some of you just skip right to the joke and move on! We’re grateful for the trust and confidence you express in us daily.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov.).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.