The President’s tweets on tariff negotiations with China along with Federal Reserve interest rate policy have been dominating financial market behavior in recent weeks. Since cutting the Fed Funds rate by 0.25% on July 31, yields on government bonds have fallen by 50 basis points in just over two weeks, which is a massive move in the bond market.

You’ll see some media commentary that this has historically been bullish for the stock market, and there is some historical evidence of that, but because of some OTHER historical evidence, we’re not so convinced. We present the evidence for both below.

In addition, last year a really interesting book came out, authored by Michael Batnick, titled “BIG MISTAKES,” The Best Investors And Their Worst Investments. It gave me the idea to write about what I think is OUR biggest mistake in the handling of client portfolios. It happened several years ago, but it’s not a distant memory.

It was a painful process, and a valuable learning experience, one we hope will benefit us and our clients for years to come. Read on for some insight on what NOT to do.

Is This Easing Cycle Really Bullish For Stocks? We’ll See

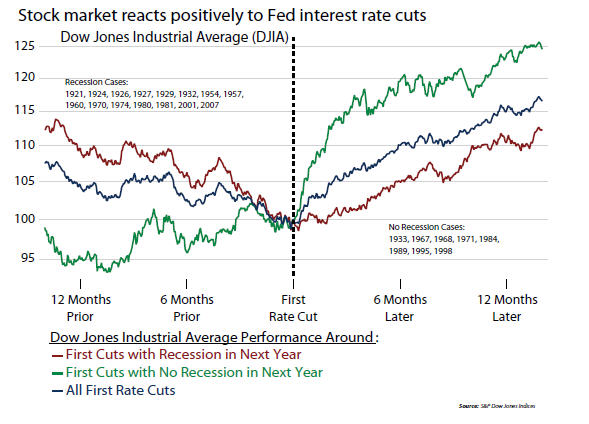

In general, and especially from the late 1970s to 1999, when the Fed cut interest rates (loosening monetary policy), the stock market has typically advanced. According to Ned Davis Research (see the chart below, courtesy of www.ndr.com), the Dow Jones Industrial Average has been up an average 16% in the year following a first Fed rate cut.

Starting in the year 1921, there have been 24 cases of a first cut, and stocks have been higher 18 times. Though limited in statistical scope, those are pretty good odds. If the recent cut is just “average” then one could expect the S&P 500 to be around the 3360 level a year from now (currently about 2900). If this is all we knew, it’s understandable where a bullish outlook could be warranted. But, there’s more to the story.

As stock market technician John Murphy noted last week, prior to the year 2000, bond yields and stock prices usually trended in opposite directions. In other words, as yields declined (remember, Treasury bonds yielded over 14% in 1980), stocks rose. This is best illustrated in the chart below, courtesy of www.stockcharts.com.

This 20-year period was marked by disinflation and falling bond yields, along with falling commodity prices. In the chart, the green arrows marked downturns in bond yields, while the black arrows denoted rising stock prices in response. That relationship changed after the year 2000, and since then bond yields and stock prices have generally headed in the SAME direction. The chart below shows the time period from 1999 to present, also comparing the 30-year Treasury Yield with the S&P 500. Last week, the 30-year Treasury Yield fell to its lowest level in history.

Where the concern is comes from the fact that we appear to be dealing with deflationary pressures the past 20 years, and currently. The last two major bear markets (2000 to 2002, and 2007 to 2009) were accompanied by falling bond yields. Could this be the beginning of the next one? Time will tell. At present, the probability of a recession is much more probable globally than in the U.S., and this is reflected in both negative yields (I cannot understand that concept) and much poorer stock market performance in comparison to U.S. markets. However, yield curve inversions using the 91-day Treasury Bill with the 10-year Treasury Note have typically led recessions by six to 12 months, so now that this indicator is flashing red, it will be especially important to watch the reaction of financial markets in coming months.

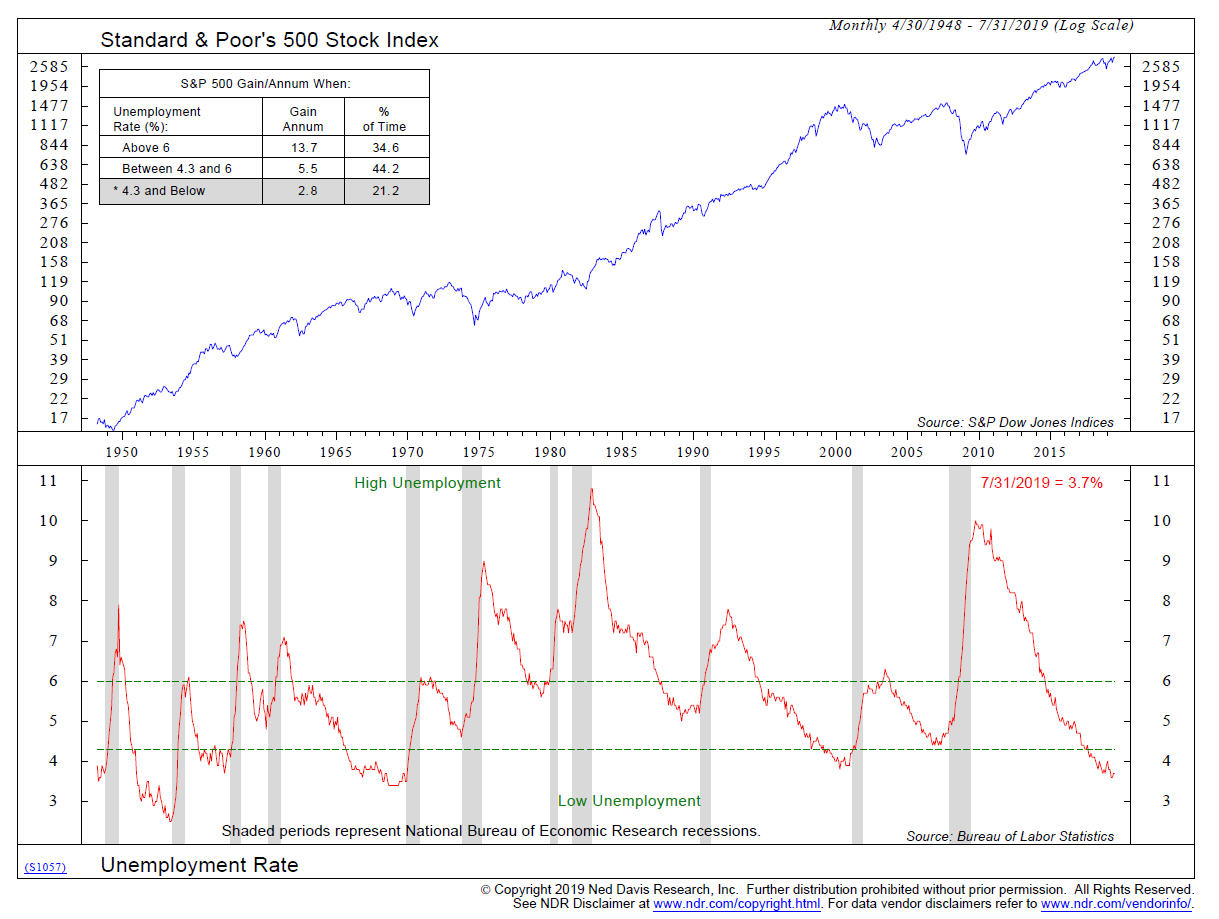

Low Unemployment Is Bearish, Not Bullish

From both an economic standpoint (and political), it is understandable that Washington and its various politicians would want employment trends to be as positive as possible. A mostly fully-employed workforce should make for happy campers, right? And happy campers make for happy voters. But, what about the stock market? I thought it was quite interesting that the data tell quite a different story.

The chart above, again from Ned Davis Research, shows the unemployment rate back to 1948. In the 71-year history of this data, when the unemployment rate has been below 4.3%, as it is now and has been for a couple of years now, the S&P 500 has compounded at the rate of just 2.2% per annum (over 21% of the time period). As the mode box shows in the upper left portion of the chart, it is a much more bullish story when the unemployment rate is above 6%. The data throws conventional wisdom on its head. This implies that most of the good news on the economy may already be baked in the cake.

The Cost Of Owning Pets (Don’t Shoot The Messenger)

By Bob Veres

What does it really cost to own a pet? More than non-pet-owners probably realize, although if you do own a dog, cat or fish, you probably have a good idea that they’re not cheap.

Start with the initial expenses. You can bring home a rescue pet—not just dogs and cats but also rabbits, guinea pigs, hamsters, birds, reptiles and sometimes fish—for the cost of a one-time fee (sometimes $0) and, for the mammals, the cost of vaccines, spaying/neutering and a microchip, which can run upwards of $500. Purebred dogs and cats obviously cost more, sometimes much more. The website Rover.com puts the average one-time cost of bringing a dog home at $838.

What about ongoing expenses? Hamsters, guinea pigs and rabbits need their bedding changed regularly, plus occasional toys and treats. Add in food, and the cost averages $600-$700 a year. Cats and dogs need food, treats and toys, yearly medical checkups, flea and tick prevention and licenses. Cats cost an average of $670 a year, while dogs can cost more than $1,000, depending on size and, therefore, food costs. Those figures don’t include the cost of walkers or sitters—or medical bills if your pet becomes injured or ill.

Of course, it’s hard to be logical about the financial decision of acquiring a pet that will become a loved family member. Just be aware of the costs and budget for them ahead of time.

Brokerage Firm Sweep Accounts (Or Getting Screwed By Schwab)

In the past few weeks, a media and print war has erupted between the two largest independent brokerage custodians, Fidelity Investments, and Charles Schwab. Fidelity shot the first arrow, declaring in print ads that their money market fund sweep options were paying a yield that was nearly 8 times that of their rival, Schwab and an even larger multiple compared to the old guard Bank of America / Merrill Lynch unit.

First, the gist of this ad is absolutely true. Schwab and Merrill Lynch use bank account sweep options as their default, under the guise of “safety.” That’s a bunch of crap. To the uninformed, which likely involves millions of customers at Schwab and Merrill, it’s a way to pay below market rates, keep the difference, and earn hundreds of millions of dollars in extra earnings each year.

Recently, I investigated the Schwab Bank sweep option and was told via on-line chat that the yield was all of 0.26%. I already knew that Schwab had other money fund options that pay market rates, but the customer service person had absolutely no idea how to get me there. For comparison, the default option at Fidelity for retirement accounts is Fidelity Government Cash Reserves, currently yielding 1.88%. For taxable accounts, Fidelity uses Fidelity Treasury Money Fund at 1.81%. What’s key here is the client (and importantly, the advisor where an advisor is involved) doesn’t have to do anything. When there is a deposit, the money “sweeps” into this core cash account and begins to earn interest until such time it is moved or used for other purposes.

This weekend, after Schwab realized they were getting their head bashed in, they responded with their own full page ads, claiming victory, in that the Schwab Value Advantage Money Fund actually yields 2.04%. That’s actually true. But, the customer first has to know about it, and second, they have to go through the effort of buying the fund. Or, the advisor has to buy it. Do you have any idea what a pain in the ass this is? Schwab and Merrill, to name two, are counting on the clients and advisors to not deal with it. It’s their dirty little secret, which goes right to their bottom line. This is plain wrong, and certainly not in the best interests of the client. If you think these firms are in favor of the Fiduciary Rule, think again.

Full disclosure—the custodian for our clients at TABR is Fidelity, and has been since our beginning in 2004. Fidelity is not perfect, but their technology is excellent, and customer service for us has been outstanding. In this area of “sweeps” they are far and away the leader in the industry, in my view. I cannot speak from experience regarding the Vanguard platform, but it’s my understanding their sweep option is the Vanguard Federal Money Market Fund, and its recent yield was 2.13%. Bravo for them. But if you’re a customer of Schwab, E*Trade, Edward Jones, LPL Financial, Merrill Lynch, Morgan Stanley or TD Ameritrade, beware. You snooze, you lose.

Bonds Are Better Than Stocks—Lately

Long time stock pros may gloat that “bonds are boring” but they don’t have much to boast about during the last 19 months. Thanks to the tailwind of falling yields, bond investments have beaten three different stock benchmarks in this period. See the table below, where all the returns include reinvested dividends.

| Fund/Index |

1-16-2018 |

8-16-2019 |

Total Return |

| TLT IShares 20 yr Treasury Bnd |

119.95 |

146.13 |

21.82% |

| GLD Spider Gold Trust |

1271.70 |

1427.80 |

12.27% |

| VBMFX Vanguard Total Bond |

10.24 |

11.18 |

9.17% |

| VFINX Vanguard S&P 500 |

249.33 |

267.24 |

7.18% |

| IJR IShares S&P SmCap 600 |

77.17 |

75.64 |

-1.98% |

| VGTSX Vanguard Total Int’l Fd |

18.26 |

15.98 |

-12.48% |

In this time period, the yield on the 10-year Treasury Note has declined from 2.54% to 1.53%. We’re certainly not advocating an investment in 20-year Treasury paper. We’d all love to earn 20%, but we rather want to note the vast majority of this return was not from yield, but from capital appreciation. The duration on the TLT fund is 17 years, so one had better have a risk management plan in place. If rates were to rise 1% from current levels, this fund would lose about -17% in value, not counting dividends.

Nonetheless, the more modest risk Vanguard Total Bond Market Fund still beat the S&P 500 Index over this period, and did so without dealing with a -20% drawdown that the stock market had to deal with during last year’s 4th quarter.

For a much longer term perspective, see the chart above courtesy of Ned Davis Research, which shows the asset class returns back to 1926 for large company stocks, corporate and government bonds, gold, treasury bills and inflation. This certainly reinforces the notion that stocks are the best long term investment. But, there aren’t any investors I know who have a 95-year time horizon. And, pay attention to the annualized standard deviation, which is a measure of volatility. Stocks are more than 3 times as volatile as corporate bonds. Many investors are not wired to deal with the down volatility that is part of the process of owning the stock market.

So, take the above data with a grain of salt. With 10-year corporate paper yielding less than 3% and the yield on the 10-year Treasury below 1.60%, we know one thing. You’re not going to earn 5.6% buying and holding those bonds for the next 10 years. And, it’s quite unlikely the S&P 500 will earn 10% compounded the next 10 years, given its current valuation levels. A number of forecasting models (some of which we’ve featured in past writings) are suggesting low single-digits going forward, at least until such time stocks actually fall significantly (more than -20%). There are certainly challenges ahead, so maybe one should just enjoy the fact that 8 months into the year, U.S. stock indexes are up on average over 16% for the year. It won’t always be that way.

Our Biggest Mistakes

First, a brief background which I think is relevant. I started using what I call mechanical timing models to time the stock and bond markets back in 1988 after I discovered that subjective forms of technical analysis were just that—too subjective. During the period from 1988 to 2003, I made the decisions on what funds to own and how much, using a variety of stock and bond market models that we had gleaned from various research sources. Quick reminder—TABR stands for Technical Analysis Based Risk-Management, so technical/quantitative models and objective data are a big part of what we do on the investment side.

When we formed TABR and began using the Fidelity Investments platform, we had access to some mutual fund managers that were not available to us at Prudential Securities. Fascinated with their disciplines and track records, we established approximate 3% positions in the Leuthold Core Investment Fund and the Hussman Strategic Growth Fund. These were funds which used their own models on stocks and bonds to adjust exposure, but they operate very differently.

Leuthold is an allocation fund, with a mix of 70% stocks and 30% bonds. The stock exposure can never be lower than 30% and never be more than 70%, and is adjusted based a large number of indicators that make up their Major Trend Model, encompassing a variety of technical and fundamental approaches. Hussman has his own models, but puts much more emphasis on fundamentals than technicals, in my view. In any case, the commonality is that we placed them into client portfolios (always including our own accounts!), and leave them alone, unlike the rest of the money we manage.

Hussman is also considered more of a hedged/equity fund, as he will take exposure down to zero, and can often act like an inverse fund if his work is really negative. In any case, they performed really well through the early part of 2009, and especially well during the bear market from 2007-09. Hussman was so good that from about December 1999 to March 2009, his fund compounded at around 8% per annum while the S&P 500 actually lost money. This got the attention of the financial press, and just a few days past what would turn out to be the exact bottom of the bear market, the Wall Street Journal featured Hussman on its front page. Whether there is any relation or not, that turned out to be the PEAK of John Hussman and his fund.

With us, over the ensuing years (2009 to around 2012), not only did we become more enamored with Hussman and his weekly research writings, we added two additional funds that were in the alternative/hedged equity style, PIMCO All Asset All Authority, managed by Rob Arnott, and the Marketfield Fund, managed by Michael Aronstein. Throw in the approximate 5% weight that we had maintained in gold funds using the Van Eck International Investors Fund (with a gold timing model), and by the end of 2012, of the maximum 60% that we allocated to equities for a Moderate Risk account, we had allocated over 20% to these five funds. Funds whose exposure we were not managing(except Van Eck), but rather trusting in the managers.

For those that don’t remember, here’s what then happened. In 2013, the S&P 500 Index gained over 30%. Even balanced portfolios where bonds were contributing very little should have earned returns in the mid-teens. Though Marketfield and Leuthold had respectable years with gains in the 16-18% range, Hussman, PIMCO and Van Eck all lost money. In fact, since 2009, Hussman’s fund has made money in only two of the past 10 years, during a period when the S&P 500 has more than quadrupled. His assets under management have gone from a peak of around $6.5 billion to under $350 million.

And, what happened to us? Well, because of this concentration in alternatives/hedged equity, our performance in the 2012-2014 period was akin to horse manure. Plain and simple. It was because we put too much trust in others, instead of our own work, and our own research, which had served us quite well for over two decades. In hindsight, it also took us too long to realize we needed to make some drastic changes and get back to our roots. We eliminated gold in June 2013, Marketfield in October 2014, Hussman in December 2014 and the final remnants of PIMCO All Asset in July 2015. All of the allocations were put back into traditional equity funds on our various stock market risk models. Let me show you what has happened to these four funds since we eliminated them, in comparison to just owning the S&P 500 Index.

| Fund Name |

Date of Removal |

Gain Since Removal |

Gain In S&P 500 Since Removal |

| Van Eck International Investors |

6-20-2013 |

29.7% |

104.7% |

| Marketfield Fund |

10-13-2014 |

-4.6% |

69.1% |

| Hussman Strategic Growth |

12-23-2014 |

-32.1% |

51.7% |

| PIMCO All Asset All Authority |

7-7-2015 |

7.79% |

50.26% |

I guess you could say the data certainly validates our decision to eliminate them from portfolios, but I really believe the bigger lesson is trusting your own stuff, and not too much of others. Trust, but verify. You’ll note that the Leuthold Fund is not on the above list. We continue to own a small piece of it, around 2-3%, because we understand their methodology. The same is true of the Sierra Strategic Income Fund, which we added to our bond strategies several years ago. We don’t “time” that fund, as we know the models that the managers use, and we’ve personally known one of the managers since 1984. We don’t trust the models of Hussman, PIMCO All Asset or Marketfield, and never will.

A note about models. Every model has a flaw, and there are no perfect models. This is why we think it’s important to diversify models and strategies, and to understand how each model works. If a model can get “stuck” in or out of the market because of its set of rules, it is really important to know this. For instance, stock market models that rely on monetary conditions may be distorted in today’s market. This is why the majority of the stock market models we use are more dependent on stock market indicators rather than “external” indicators. External indicators include monetary, sentiment and fundamental metrics.

All in all, there is a need for healthy skepticism about celebrated money managers. “Investors are prone to latching on to star managers, believing they’ve got the individual as the secret sauce, and that only they can potentially outperform the market,” says Todd Rosenbluth, director of exchange-traded fund research at CFRA Research. “People are fallible. Investments move in and out of favor. You should be buying a fund, not putting money to work for a specific manager.”

We’ve definitely learned that lesson, the hard way. We believe we’re better today than we certainly were in 2012-14, and even better than in 2008, when our performance was pretty decent, but could have been even better. Most importantly, we’re quite grateful for all the clients who stuck with us during the rough patch. Someday, there will be another big decline, and our aim is to reward the confidence that has been placed in us by protecting capital, but also to continue to participate reasonably well in up markets, when the trend evidence is compelling, as it has been for parts of the last three years.

Investment Allocations

At present, tactical equity portfolios remain 85% invested in stock funds. There have been no exposure changes for nearly two months, and equity exposure has been 70% to 85% since February 19. There was one change on the selection front within stock exposure, as at month-end, our allocation in the I Shares Emerging Market Index (IEMG) fell out of our rankings and was replaced with the I Shares Mid-Cap Growth Fund (IJK).

Though corporate high yield bond funds have weakened a bit off of their all-time highs a few weeks ago, they have not generated a SELL signal. Overall, our positions are in a moderately bullish mode, despite the increased volatility of the past couple of weeks.

Material Of A Less Serious Nature

A Wife’s Diary:

Tonight, I thought my husband was acting weird. We had made plans to meet at a nice restaurant for dinner. I was shopping with my friends all day long, so I thought he was upset at the fact that I was a bit late, but he made no comment about it.

Conversation wasn’t flowing, so I suggested we go somewhere quiet and we could talk. He agreed, but he didn’t say much. I asked him what was wrong. He said, “Nothing.” I asked him if it was my fault that he was upset. He said he wasn’t upset, that it had nothing to do with me, and not to worry about it.

On the way home, I told him that I loved him. He smiled slightly, and kept driving. I can’t explain his behavior. I don’t know why he didn’t say, “I love you, too.” When we got home, I felt as if I had lost him completely, as if he wanted nothing to do with me anymore. He just sat there quietly, and watched TV. He continued to seem distant and absent.

Finally, with silence all around us, I decided to go to bed. About 15 minutes later, he came to bed. But I still felt that he was distracted, and his thoughts were somewhere else. He fell asleep—I cried. I don’t know what to do. I’m almost sure that his thoughts are with someone else. . .my life is a disaster.

Her Husband’s Diary:

Boat wouldn’t start, can’t figure it out.

Just so you know, that would not be my diary! I couldn’t fix a boat if it hit me. But when the Stars lose a 7th game in double overtime with a chance to go to the Western Conference Finals, and miss the game-winning goal by perhaps 3 inches, don’t expect me to be smiling.

Well, school has officially started for many, including our high schooler, with the rest after Labor Day. By mid-September, college and pro football will be in full swing, with baseball playoffs approaching. As for markets, they’re with us every day! Thanks for your continued trust and confidence in all of us at TABR.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

Inverse ETFs

An investment in an Inverse ETF involves risk, including loss of investment. Inverse ETFs or “short funds” track an index or benchmark and seek to deliver returns that are the opposite of the returns of the index or benchmark. If an index goes up, then the inverse ETF goes down, and vice versa. Inverse ETFs are a means to profit from and hedge exposure to a downward moving market.

Inverse ETF shareholders are subject to the risks stemming from an upward market, as inverse ETFs are designed to benefit from a downward market. Most inverse ETFs reset daily and are designed to achieve their stated objectives on a daily basis. The performance over longer periods of time, including weeks or months, can differ significantly from the underlying benchmark or index. Therefore, inverse ETFs may pose a risk of loss for buy-and-hold investors with intermediate or long-term horizons and significant losses are possible even if the long-term performance of an index or benchmark shows a loss or gain. Inverse ETFs may be less tax-efficient than traditional ETFs because daily resets can cause the inverse ETF to realize significant short-term capital gains that may not be offset by a loss.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.