How Proposition 19 Can Reduce Your Property Taxes

In this month’s newsletter, I’ll recount a true story about my neighbor who got a terrible surprise on his property tax bill, although I’ve changed some of the details to protect privacy. Two months ago, he got a notice from the Orange County Assessor’s Office saying that his property tax bill had increased by $14,000 per year. He thought there must be some kind of mistake, but the notice was correct. The most frustrating part for him was that this unfortunate situation was completely avoidable, but as it turns out, it was also correctable.

My neighbor had inherited the home from his parents last year. His parents bought the home for $80,000 48 years ago in 1975, and under Proposition 13, their property tax basis had increased by the maximum allowable 2% each year since then. This resulted in a property tax basis of $200,000 last year, even though the home was worth $1.6 million.

With a 1% property tax rate, the parents were only paying $2,000 per year in property taxes. When the son inherited the property, he continued paying $2,000 in property taxes, based on the $200,000 assessment. That was until he got the letter saying his property tax bill increased to $16,000 per year, 1% of the new $1.6 million assessed value.

This surprise happened due to California Proposition 19, which was approved by voters in 2020. Had my neighbor or his parents known what you’re about to read below, they wouldn’t have been surprised by this huge jump in their property tax bill. As you’ll learn, Prop 19 has potential pitfalls for those who inherit properties, but it can be the best friend of homeowners who want to move to another home in California and keep their property tax basis.

California Proposition 19 is also known as “The Home Protection for Seniors, Severely Disabled, Families, and Victims of Wildfire or Natural Disasters Act.” It was a major ballot measure passed in the 2020 election.

The overriding goal was to make substantial changes to property tax rules in the state of California, with a particular focus on property tax transfers, exemptions, and revenue allocation for wildfire agencies and counties. For background purposes, I’ll begin with an overview of Proposition 19 and delve into its key provisions and implications for California residents, homeowners, and taxpayers.

The California property tax system, established under Proposition 13 in 1978, has been a cornerstone of the state’s tax structure for decades. Proposition 13 capped property taxes at 1% of the property’s assessed value (plus additional voter-approved taxes) and limited annual increases in assessed value to 2%. This resulted in a system where long-term property owners benefited from low property taxes, while new buyers often faced much higher tax bills due to reassessments at higher market values.

Proposition 19 was a response to the evolving California property tax landscape. Its goal was to address the unequal treatment of long-term homeowners and new buyers while also generating revenue for fighting wildfires in the state.

Prop 19 Provisions: Inheritance Exemptions and Property Tax Portability

Inheritance Exemptions

This is the part of the new law that is relevant to my neighbor’s situation, as Prop 19 significantly changed the property tax rules for inherited properties. Under the previous rules, inherited properties were often passed down to heirs without triggering a property tax reassessment, allowing them to continue paying based on the original assessed value.

Prop 19 limited this exemption, so now inherited properties are only eligible for reassessment exclusion if the heir uses the property as their primary residence. If the heir rents out the property, it will get reassessed to the current market value and result in higher property taxes. Prop 19 effectively ended the “parent-to-child” and “grandparent-to-grandchild” exclusions for inherited properties that were not used as primary residences.

As mentioned above, parents can transfer their home to their children, and it won’t be reassessed to the full market value if at least one of the children lives in the property as their primary residence. The value limit under Proposition 19 is calculated by adding the factored base year value (FBVY, i.e., the current taxable value) and $1 million.

If the market value is higher than this limit, the amount exceeding the value limit will be added to the current assessed value. Therefore, if the child meets the other qualifications and submits Form BOE-19-P, Claim for Reassessment Exclusion for Transfer Between Parent and Child, they are still entitled to the exclusion, albeit with an adjusted taxable value accounting for the excess over the value limit.

In my neighbor’s case, the home had a factored base year value (FBYV) of $200,000 and a fair market value of $1,600,000.

The excluded amount under Proposition 19 is $1,200,000 ($200,000 + $1,000,000 = $1,200,000).

The difference of $400,000 ($1,600,000 – $1,200,000 = $400,000) is added to the property’s FBYV.

The adjusted base year value is $600,000 ($200,000 FBYV + $400,000 difference).

My neighbor’s new taxable value should therefore have been $600,000 instead of $1.6 million, saving him about $10,000 per year.

Fortunately, the Form BOE-19-P application can be filed within three years of the date of the transfer date. After the awful surprise, my neighbor filed the form and is now saving $10,000 per year in property taxes.

Property Tax Portability

Another important aspect of Proposition 19 is the significant change in property tax portability, and this is the area of the new law that’s relevant to many of our clients. Under this provision, homeowners who are 55 years of age or older, severely disabled, or victims of natural disasters can transfer their primary residence’s assessed value to a new home of equal or lesser value anywhere in California. Property owners can file the transfer of taxable value up to three times during their lifetime.

This allows eligible homeowners to downsize or relocate without triggering a reassessment of the current market value. Under prior law, this was only available to homeowners within the same county or in counties that had reciprocal agreements, so few got to take advantage of this benefit.

This property tax portability is a substantial benefit, allowing the flexibility to move without the threat of significantly higher property tax bills. Part of the thinking was that this would encourage seniors to downsize or relocate closer to their families, thereby freeing up larger homes for younger families. Another argument in favor of Prop 19 was that it could potentially stimulate the real estate market and increase housing inventory.

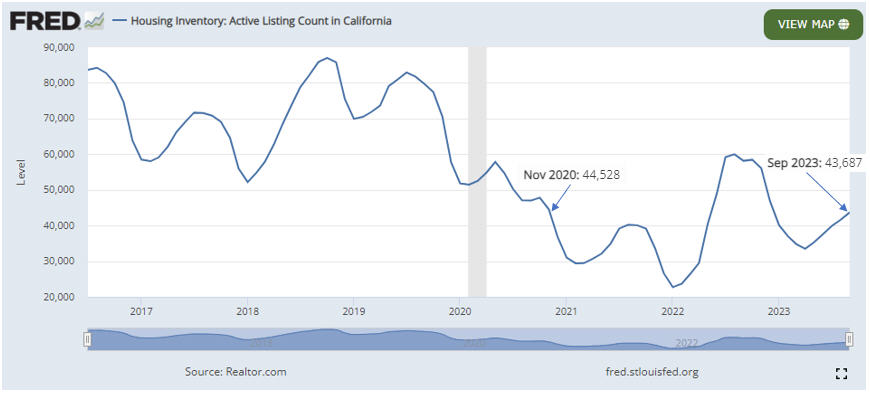

As an aside, increasing housing inventory has not happened. According to Federal Reserve Economic Data (FRED), California housing inventory active listings were 44,528 when Prop 19 was passed in November 2022, and 43,687 in September 2023, the most recent data available. Of course, that could be due to homeowners being unwilling to move with 30-year fixed mortgage rates above 7.5%, but that is a discussion for another newsletter.

So how does property tax portability work?

If the market value of the replacement property is less than or equal to the market value of the home you’re selling, then the current taxable value of the original home will transfer to the replacement home without an adjustment. For example, if my neighbor’s parents had downsized their $1.6 million home to, say, a $1.1 million home during their lifetimes, their new property tax basis would have stayed at $200,000 for the $1.1 million home.

If the market value of the replacement property is greater than the market value of the home you’re selling, the difference will be added to the transferred value. For my neighbor’s parents, selling their $1.6 million home and moving into a $2 million home, would have required that $400,000 difference to be added to the taxable value.

In this example, $400,000 + $200,000 would result in the new $600,000 taxable value. Still, a $600,000 property tax basis is a lot better than $2 million, saving them $14,000 per year, assuming a 1% property tax rate. (This also assumes that the replacement property is purchased before the original property is sold. If that’s not the case, the value of the original primary residence would need to be increased by 5% or 10%, but we’ll ignore this adjustment for simplicity).

In order to qualify based on being at least 55 years of age, you would need to submit form BOE-19-B (Claim for Transfer of Base Year Value to Replacement Primary Residence for Persons at Least Age 55 Years) to the County Assessor where the replacement property is located. Form BOE-19-D, BOE-19-DC, or BOE-19-V would be required for those qualifying based on disability, wildfire, or natural disaster.

If you’re curious, the goal of Prop 19 was to increase resources to combat wildfires in California. The proposition therefore allocated a portion of the revenue generated from property tax changes to wildfire agencies and counties with the goal of improving firefighting efforts and emergency preparedness. The funds are also allocated toward acquiring critical equipment and resources for fighting wildfires.

The Prop 19 rules can get complicated. If you have further questions, the California State Board of Equalization website and fact sheet may be helpful, or you can call me to discuss your particular situation.

Are We Headed for a Soft Landing?

Two weeks ago, Ned Davis Research (NDR) published a Macro Update saying that the weight of the evidence continues to suggest a soft landing is the more likely scenario for the US economy. Of the ten indicators cited in their US Recession Watch Report, only two are flashing negative signals, indicating a low risk of recession. Some of their positive indicators include the fact that US consumer spending is strong, excess savings and the job market are robust, and real wages are rising as inflation recedes.

However, not everything looks rosy. NDR estimates that a government shutdown would subtract more than 0.1 percentage points from real GDP for each week that it lasts, and if the UAW strike turns into a full-fledged walkout, real GDP could drop, and inflation could rise. These factors, along with rising oil prices, could eventually result in a recession.

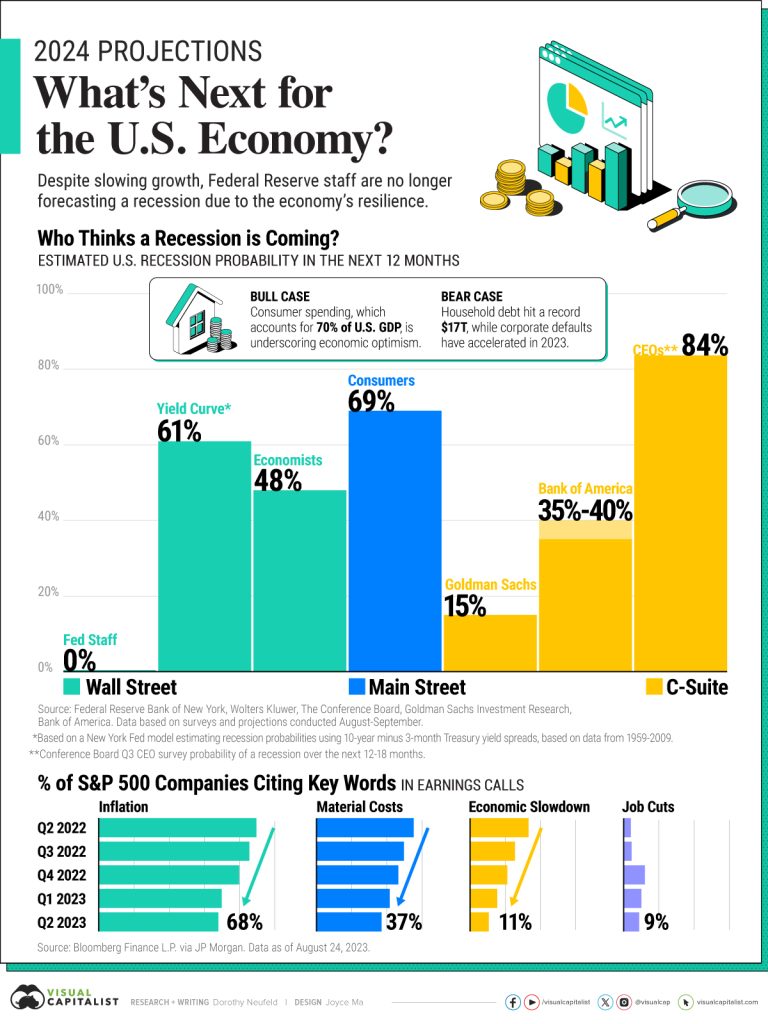

NDR is a credible global provider of independent investment research, and I put trust in their research since they use a disciplined weight-of-the-evidence approach. At TABR Capital Management, we don’t put much weight on random opinions, but I thought the disparity in the chart below was noteworthy.

While 84% of CEOs and 69% of consumers think a recession is likely within the next 12 months, 0% of Federal Reserve staff think it’s likely. It looks like the Fed has a lot more confidence in their ability to influence the economy than the rest of us do.

Social Security Cost of Living Adjustment (COLA)

Last week, the Social Security Administration announced the 2024 cost of living adjustment (COLA) will be 3.2%. This is well below the near-record 8.7% increase for 2023, but it’s still above the 2.6% average over the last 20 years.

TABR Investment Allocations

While NDR’s research informs our investment decisions, we don’t manage money based on predictions. We use data from our quantitative models, reflecting what’s actually happening in the markets, and adjust our investment positions accordingly. In the weeks since Bob Kargenian wrote our September Monthly update, there have been quite a few changes in our investment allocations.

In early September, our stock market models were mostly positive, and we had 80% exposure to stocks (e.g., a Conservative account with a maximum of 40% in stocks would have had about 32% of the entire account in stocks – 80% of the 40% maximum).

Since then, three of our six stock models gave a sell, and we dropped our stock market exposure to 33% before increasing back to our current 50% allocation when one of those models went back on a buy signal. The present 50% exposure feels like no man’s land, but eventually, the market trend will resolve into more of an uptrend or downtrend, and we will raise or lower our stock allocations accordingly.

We also got a high yield bond sell signal from one of our two models on October 10, and we sold 60% of those positions. We’re on alert to sell the remaining high yield bond positions if our second model gives a sell signal. Our model for the PIMCO Income Fund also turned negative.

Finally, on October 12, our gold model went on a sell signal, so we sold out of our IAU (iShares Gold Trust) position.

Homes For Our Troops

Since 2014, TABR has been providing pro bono financial planning through Homes For Our Troops, an organization that provides specially adapted, mortgage-free housing for severely injured veterans. On the last Saturday in September, I was honored to attend the key ceremony where Erik Galvan and his family received the keys to their new home in Fallbrook, California.

In 2011 at age 19, Erik lost both legs and his right hand when on patrol as a Marine infantryman in Afghanistan. He has since earned his master’s degree in social work at the University of Southern California and is involved with Wishes for Warriors, a nonprofit helping combat-injured Veterans experience therapeutic outdoor activities.

While Erik can get around with his prosthetics, they cause pain and discomfort, and his family’s previous home wasn’t wheelchair accessible. His new specially adapted, custom HFOT home is not only wheelchair accessible, but it also has adaptations like lower countertops, pull-down shelving, and a roll-under stove.

All these features allow him to focus on his wife and young son, not to mention his passion as a home chef. I’m so happy to be a small part of their new beginning and thankful for organizations like HFOT that support our veterans.

Fall is Here

It’s hard to believe that summer ended three weeks ago. My daughter Audrey is now a junior, and my son Conrad is a freshman, both in high school. Now that they’re in the same school again, it’s made things easier with them being on the same schedule. This summer, we got to vacation in Italy, a trip that we had postponed from the original June 2020 schedule due to COVID-19. How was that for timing the original trip?

Well, better late than never, as they say. Below are a few of my favorite pictures in Rome and Positano, on the Amalfi Coast. We also got to spend a day on the island of Capri, which was beautiful.

All of us here at TABR Capital Management wish you and yours a wonderful fall and are grateful for your continued trust and confidence.

Best regards,

Steven W. Medland, MBA, CFP®

Partner

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.