Individual Stocks—Exasperating And Thrilling

How many of you have heard this story before? A friend shares over coffee or a beer how much money they’ve been making in Apple, Amazon, Tesla or Pfizer. You’re intrigued. After all, those guys at TABR have you in boring, old, index funds via ETFs for your stock market exposure.

You know, the S&P 100 (OEF) which went up 21% in 2020. Or even the S&P Large Cap Growth ETF (IVW), which went up 33%. But, hell, Apple was up 82%! Give me more of that!

This, of course, is easy to say with hindsight. It’s another thing to live through the maximum drawdowns which occur nearly every year with some of the greatest companies. We’ll see if you were paying attention, above. Pfizer? It’s certainly in the news these last 18 months, having developed one of the three vaccines which have been instrumental in solving the COVID virus. But, wait until you see the history of its stock price.

The data shows that 85% of large company active stock managers lagged the S&P 500 Index for the 10 years ending in 2019. Those are professional fund managers whose job is to beat the market. It’s a fair question. If they cannot do it, what makes you think you can?

We’ll explore that area this month, as I don’t believe the answer is as black and white as we might all want it to be. There is also a lengthy section on estate planning. Finally, a personal recommendation. If you have Apple TV, watch the new movie out called CODA (which stands for child of deaf adult). This is not to be confused with a different movie also called Coda, which is an expanded cadence in music. More on CODA below. I loved it, and think you will too.

The Thrill And Chill of Individual Stocks

I’ve already mentioned industry data that shows professional stock pickers have a hard time beating the market. Then there’s the groundbreaking study published in 2018 by Arizona State University professor Hendrik Bessembinder which found that “a randomly selected stock in a randomly selected month is more likely to lose money than make money.” Picking single stocks and holding a concentrated portfolio tends to be a losing strategy.

I can tell you that until I’m blue in the face, but it will not stop you from calling us up and saying, “Hey, would you buy me 100 shares of Costco in my IRA?” For this article, I scanned the list of restrictions we have embedded into the software Fidelity Investments provides us to manage your accounts. We use model portfolios, which are matched to a clients’ risk profile (Conservative, Moderate, Aggressive), but we’ve always allowed one-offs to be collaborative with client requests.

The restrictions I mention above allow us to run our models without inadvertently selling a clients’ position in a stock, which of course is not going to be part of our model. We currently work with over 200 households nationwide, and I just counted over 100 restrictions. This doesn’t mean that nearly 50% of our clients have an individual stock (or more) in their portfolio. Most of the situations involve one or two stocks. It might be “I inherited Chevron from my parents, and I’ve always wanted to hold onto it,” or “I had an insurance policy with Prudential and ended up with shares of the stock.”

Other times, it could be “I go to Starbucks several times a week, and like the coffee and experience, and think it would be a good investment.” For the most part, we have no idea where clients come up with their ideas, though I do think a few may be subscribing to the Motley Fool, a stock picking advisory letter. One thing I’m fairly certain of, though, is they’re not likely poring over financial reports, calculating quick ratios, free cash flow yields, debt levels and constructing discounted cash flow models to find out if a company is undervalued or not.

No, instead they are in many cases looking to have some fun, to have something to follow, to take an interest in something above and beyond their core portfolio, and at the same time, looking to maybe latch on to a stock that could really take off like a rocket. In fact, we’ve had six clients in the past 10 years or so who’ve done this to one degree or another and have had substantial success with a handful of companies. Look at the list below, in order of the greatest percentage gain.

Nvidia NVDA 4300%

Alphabet GOOGL 2800%

Shopify SHOP 1537%

Tesla TSLA 1400%

Tesla TSLA 1192%

Apple AAPL 277%

With one exception, every one of these has become worth anywhere from $150,000 to over $600,000. In other words, some substantial money. And—editor’s note here—I hope I’m not jinxing any of them by writing about this subject. This is intended to be educational, and hopefully, enlightening. These clients have been able to do something that for the most part, I don’t think I could do with my own money (though we do follow this strategy with our Passive Index account). What is that? Buy a stock, and leave it alone, for years. Look at the chart below, courtesy of our friends at www.stockcharts.com.

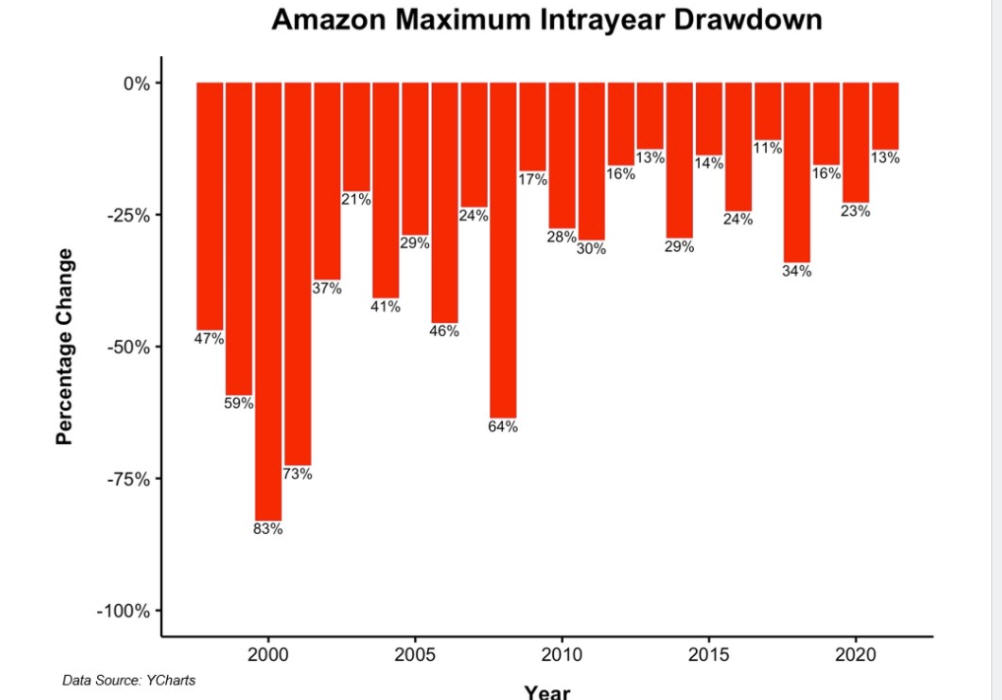

Who wouldn’t have wanted to buy Amazon in 2002 at under $8 per share, and still own it today? It’s at $3349 per share. It has gone up by a factor of 418. But, even if you had been lucky enough (smart) to buy it back then, or even a bit earlier in 1999, look at what you would have had to endure each year to get to today.

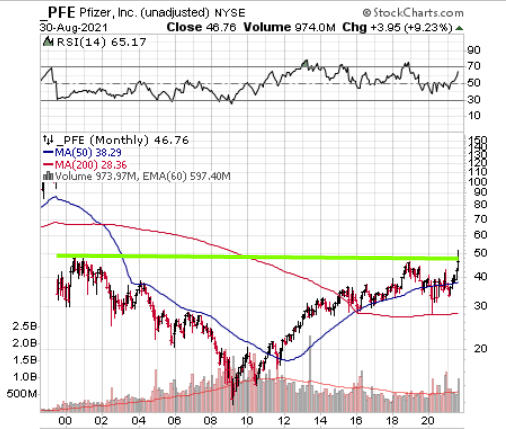

The chart above is courtesy of Y Charts, and Michael Batnick, a terrific writer at An Irrelevant Investor. It shows the intra-year drawdown for Amazon for each year since 1998. For the first 11 years, the losses ranged from -21% to -83%, with six of them greater than -46%, or nearly half your money. We know, with the benefit of hindsight, that Amazon sits where it is today. But, could you have endured the ride to get there? Many companies double, triple and even go up seven-fold, and then disappear. They certainly don’t all turn out to be Amazon. Hardly any, in fact. You could just as easily end up with Pfizer. See below, also from www.stockcharts.com.

The stock today, still trades (on a price basis) below the all-time high set in April 1999 at 47.47. That’s right. It’s gone nowhere for over 22 years. One of the greatest drug companies in the world. Thank goodness Pfizer pays a dividend, and a decent one at that. It is ironic that if you bought Pfizer stock today, it pays a current yield of 3.34%. Since its all-time high in April 1999, the compound return of the stock, including dividends, has been 3.3%. In other words, all of the return to shareholders during the 22 year time span has been dividends.

Had you purchased Pfizer at $47 in 1999, you had no way of knowing that 10 years later, the stock would be below $10. Given that the U.S. stock market goes up over the long term, I’m sure that wouldn’t have been an expectation. Yet, that’s the point. Individual stocks are not the market. Some will come back. Some won’t. As writer Ben Carlson suggested earlier this year in his column “Owning The Best Stocks Is Hard,” he wrote “Drawdowns are always far easier to deal with in the past than in the present. You know the length and duration of past losses. When stocks are down in the present, you never know how bad the losses will get or if/when they will come back from those losses. Picking the winners is hard. Holding onto them might be even harder.”

I couldn’t agree more. Kudos to those who have been successful in this area. There aren’t many. In my own case, I don’t think I’ll ever go back to using fundamentals to pick stocks. I need something that adapts to the market environment, and for me, that is relative strength and the technical indicators that go with it. We have a limited history at this time, only going back to February 2020 in real time, with our OEX Relative Strength strategy, but we believe it to be based on sound principles which will hold up over time. We’ll be reporting on its process and results over time. It is always fully invested in stocks and never plays defense, a bit opposite of our tactical work. If you want juice in your portfolio mix, this would be it.

How To Have Your Own Disneyland Magic Dream Key—For Free

Some of you may remember Peter Lynch, the former portfolio manager for the Fidelity Magellan Fund. Lynch became famous for his spectacular returns running the fund from 1977 to 1990, when it compounded at 29% per annum. Though there are other important features to his process, in simple terms, Lynch recommended investing in what you’re familiar with, in what you know. In that vein, I came up with an example of how you can take something you may love, and have it pay for your entertainment.

Disneyland is a world-wide favorite (and its East Coast counterpart, Walt Disney World), right here in Anaheim, CA. I can actually see the Matterhorn from my 13th story office window. Because of capacity issues at the park (not enough space, too many people wanting to come), Disney last year decided to eliminate their annual pass program. It was recently replaced with their new program, called Magic Keys. There are a few different levels of the program (much like the past), but for illustrative purposes, we’ll focus on the top premium pass, now known as the Dream Key. It costs $1399 per year, and comes with free parking, and admittance to one or both of the parks (California Adventure here in SoCal) any day of the year, but you must make a reservation in advance.

Let’s face it. That’s not chump change. That’s $2800 for a couple. Or for a mom and daughter (as is the case with the Kargenian family). It’s not a cheap vacation, or entertainment, but as many of you know, the kids love it, and so do many adults. We just went for a week to Disney World in late June. Besides tickets, throw in airfare, hotels and food. Those of you who have done this, you already know what I’m referring to. But, here’s my point. For a one day, park hopper pass to Disneyland, the cheapest ticket is $159. You can bitch about it, or you can put Disney to work for you.

From December 31, 1999, to September 2, 2021, Disney stock has compounded at 10.1% per annum, including dividends. The company has an unbelievable brand, which includes the theme parks, ESPN, and countless movies. Their revenue in 1999 was $23.4 billion, and was $65.39 billion in 2020, a near triple. I can’t tell you if the stock will grow 10% per annum in the next 20 years, but let’s say because of size and other factors, the growth rate slows to 8%. If you invest $35,000 today in Disney stock, and it compounds at 8% per annum, that would be equal to $2800 per year, enough to pay for your two annual Dream Keys. And there’s your “free” Magic Key. You can apply this thinking to many other companies that provide services we all use. Think of Comcast, Verizon, Home Depot, Exxon, Pay Pal, Bank of America, VISA, Johnson & Johnson, JP Morgan, Apple, Google, and Amazon. Let them work for you. By investing in them, you are growing with them. What do all of those companies have in common? They’re all members of the S&P 500 Index, so if you’re not into picking stocks, all you have to do is own the fund or ETF that replicates the index.

Estate Planning—An Essential Reminder

You’ve probably heard this anecdote, that was attributed to Benjamin Franklin. There are only two certainties in life—death and taxes. Though it’s hard to understand this when you’re twenty, you begin to understand it more when you reach 40, and certainly 60. Mainly, that as you get older, you typically pay more of the latter (since you are usually earning more in your later years), and you inevitably get closer and closer to the former. Life takes all of us through a similar cycle. I started in this business when I was 24. I’ll be 64 in November. In the 1980s and 1990s, virtually none of our clients died. Now, we encounter this several times per year. My parents are both gone, my dad having passed in 1995, and all of my aunts and uncles are gone. In fact, that culminated this past February, when I lost 3 aunts and uncles in a span of less than three months.

We all know that we don’t know when death will call us. It’s a tough subject for many, which is perhaps why according to a Caring.com study, only 42% of adults have an estate plan in place, which would include a will or living trust. We routinely come across prospective clients in their 50s and 60s who have no estate plan in place. Many of these people have $millions of dollars in assets. Given that I’ve now lived through the experience of being responsible as a Trustee for one of my aunts, and all that goes along with that, I thought it would be timely to remind many of you what to expect in the event you are thrust into that role for a parent, sibling or friend. For those of you in your 30s or 40s, it’s a good reminder to perhaps have a conversation with your parents (if they are willing), simply to help be better prepared for when something was to happen. And, for those of you who have nothing in place, maybe this will be the nudge to get you off your procrastination and get it done. I believe you’ll sleep better at night, knowing all is taken care of.

Before I delve into all of the things I got involved with, below is a brief summary of 9 lessons you should be aware of. There’s a really helpful piece on these called Courtside Seat (III), by attorney Robert Port, which was published in July on the Humble Dollar personal financial planning website. Here’s a link to the entire article. https://humbledollar.com/2021/07/courtside-seat-iii/. There are more details about each lesson in the piece.

Lesson 1 Yes, You Need A Will Or Trust

Lesson 2 Yes, You Need Other End-Of-Life Legal Documents

Lesson 3 Keep Your Beneficiary Designations Current

Lesson 4 Make Sure The Person Holding Your Power Can’t Abuse That Power

Lesson 5 Be Careful With Joint Accounts

Lesson 6 Elder Financial Abuse Is More Common Than You Think

Lesson 7 Your Trust Is Only As Good As Your Trustee

Lesson 8 Even Though Your Divorce Is Behind You, Your Financial Entanglements Might Not Be

Lesson 9 Being Part Of A Family Business Can Be Wonderful—Until It Isn’t

Probably the main message I want to convey is how much work is involved for a Trustee, even when everything is in place and done correctly. That was the case with my Aunt Alice, my mother’s remaining sister, who lived in Clovis, CA, right next to Fresno. It is staggering to think how difficult things would have been had she not had everything in place.

She had a Trust, and the home she had lived in since 1963 was in the Trust (that’s really important!). I was successor trustee to her, since her husband, my Uncle Charles, had passed away in 2014, and she had no children of her own, only two nephews and a niece. In addition, my brother and myself were designated as power of attorney for healthcare decisions should she become incapacitated. Unfortunately, that’s exactly what happened, and it took place instantly.

Last September, I received a call one morning from the Clovis Police Department, indicating they had to enter her home after a neighbor had become concerned since she wasn’t answering the phone and a couple of days worth of newspapers were accumulated in the front yard. They had found her unconscious, suggesting she may have been that way for a day or so. She spent a week in the intensive care unit, and I had to immediately get involved from over four hours away, with no ability to see her given Covid lockdowns, and she had no ability to speak at this juncture.

Thanks to having relationships with the Medicare/Medical Certified nursing home in Fresno that my other aunt had stayed at (my mother’s other sister), not to mention my cousin’s relationships there, I was able to get her into their skilled nursing care upon her immediate discharge from the hospital. Fortunately, we had all of her Trust documents from the estate attorney in Fresno, who has served several of our clients, or we knew if something was missing, we could get it from them if necessary.

Once we had secured the most pressing need, being my aunt’s medical care, we turned our attention to dealing with her home, finances, and all related obligations. A family friend of hers was tremendously helpful, and he met us at her residence with a key to the house, though a couple of years prior, my aunt had told me of where she kept the “spare” key, in the event something like this were to happen.

My brother and I were able to secure the house until we had more time to deal with it, and I was able to find almost all of the documents I needed to deal with her monthly expenses and income. This ranged from bank statements to auto insurance, homeowners insurance, the trash and water bills, electric and gas bills, satellite TV, the newspaper, the phone, the security system for the house, her pension, Social Security, Medicare and her Medicare Advantage health care plan.

Given her condition, I knew she was never going to return home again, so I had the address changed on all of the various accounts, but still had to become trustee on her bank accounts at Wells Fargo, so that I could write checks and pay the bills. Fortunately, a couple of years ago I had set up online access for her which allowed me to help her if necessary, but I still had to provide the bank with a letter from her doctor certifying that she was unable to act on her behalf anymore.

That proved to be a bit more difficult than it should have been, only because the doctor wasn’t paying attention to details. The bank needed the letter from the doctor on letterhead. I even wrote the letter for the doctor, emailed it to him, and said, please send this back to me, signed on your letterhead. Several days later, I received an envelope from the doctor, with the letter photocopied together on a blank piece of paper. I wanted to wring his neck. I had to call him and ask as nicely as I could, “do you know WTF letterhead means?” That whole process was delayed about two weeks thanks to this.

However, once I got checks in the mail that I could use as trustee and pay the bills, pretty much everything began to run smoothly. We still had to sell her car, though, and knew eventually we’d have to deal with her home. She had a 2012 Mercedes, and I knew I had to change the registration on the car before we could sell it, and deposit the proceeds in my aunt’s checking account.

I dutifully went down to the local Auto Club of Southern California office on a Saturday with the registration and paperwork showing I had power of attorney, thinking I would sign some forms and get it processed. Then, the clerk asked me, where’s the title to the car? I’d totally forgotten about the title, and honestly had no idea where that would be in her house.

To replace a lost title, I had to complete a form and my aunt had to sign it, along with me. I explained she was incapacitated and likely couldn’t sign, which is why there is a power of attorney. She told me the DMV doesn’t honor power of attorney forms. I’m thinking, “why the heck do we have these estate planning documents if the government doesn’t honor them?” The clerk looked at me and asked, “Can she sign an X?” I’m like, “Ma’am, we’re in COVID lockdown, I can’t even see her in person.” Then my smart brain kicked in and I said, “Don’t worry about it, I’ll figure it out.” By the way, we also had to get the car smog checked and submit a certificate with the title replacement form.

Within the next week, I had my brother drive to Fresno and take the car into get smog checked, and he mailed the new smog certificate to me. I then took the paperwork back to the Auto Club, including the transfer form signed by my aunt (which was impossible, just so you know). I thought I was home free, until the clerk was processing everything and then says, “Oh, we also have to have this form signed, which verifies the odometer of the car at the time of transfer and the smog check, and it must be signed by your aunt (the seller), and by you.”

I showed her the smog certificate, which had the odometer listed, but no, that wasn’t good enough. We had to sign the forms. So, knowing I was not going to win, I took the forms, went home, waited a week, had my aunt sign the form (again, that was impossible), and took everything back and gave it to the clerk. Four weeks later, the new title showed up in the mail, and a couple of months later, I was able to go to Fresno and sell the car to CarMax in a relatively painless transaction, and deposited the check to my aunt’s checking account.

Yes, all of that just to deal with the car. My aunt passed away on February 6. We then had to plan her memorial service and sell her house. Thanks to the help of my uncle’s family from Reno, plus my wife and son along with an amazing non-profit in Visalia that our office manager Mary Hernandez had remembered, we were able to completely clean out my aunt’s home in two days. Working with a terrific realtor that my cousin in Fresno referred me to, he coordinated everything for me, from painting to flooring and cleanup, so the house could be shown totally empty.

With Fresno being the hottest housing market in all of California, in early March we listed my aunt’s house for sale, and within 3 days had 9 offers, all over the asking price, ranging from $1000 to $30,000 higher, entered into a contract and closed an all-cash offer within 30 days.

We’re still not totally done with our duties, though. My aunt had shared that the favorite place she and my uncle would visit and vacation was in Bandon, Oregon. Uncle Charles was cremated and so was my Aunt Alice, and her wish is for me to take both of them (their urns are sitting in my closet) up to Bandon and somehow figure out how to legally dump them in the ocean together. To honor them, that trip is in our future.

My aunt’s situation was relatively simple. Other families and individuals, including businesses, are much more complex. Though the details were lengthy, I wanted to give you a realistic glimpse of what is involved in being a trustee for a family member or friend. Do not take it lightly. It is a lot of work, and not everyone is cut out for it. Steve Medland and I often give clients advice in this area in helping them choose which of their children might be best suited for this role.

And remember, the above might be the tip of the iceberg if you DON’T have an estate plan or will. You will be inflicting unnecessary pain and burden on friends and family if you fail to take care of this area.

Besides the very helpful article noted above, I also came across a nine-part series on these topics put together by Stack Financial Management. You can access the series here at www.stackfinancialmanagement.com/category/estate-planning/

Portfolio Allocations Update

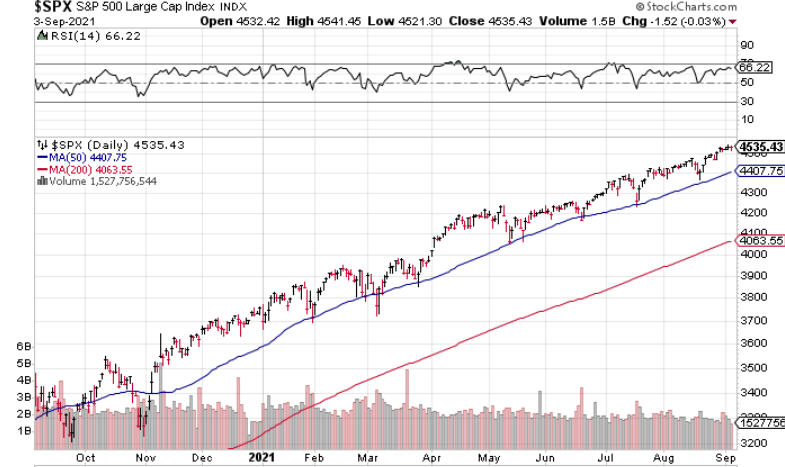

There’s not much change to report in this area. As the chart below of the S&P 500 shows, courtesy of www.stockcharts.com, the uptrend that began last November has lasted over 10 months, with the index touching its 50-day moving average 8 times, and rebounding each time.

A lower low is required to break this pattern, and that won’t happen at this juncture until 4370 is violated. One of our six stock market risk models has been whipsawed several times this year, but equity allocations have never been below 80% or so, and again are at 100%. We have had one shift in relative strength, with one position in small caps (IJR) being replaced with large growth (IVW). The other two remain in mid value (IJJ) and small value (IJS).

Our gold model was temporarily positive for a few weeks, but the trade was closed out with a small loss. And finally, our high yield bond funds are making new highs, having turned bullish last November.

Go See CODA

From time to time, many of you share with us great recommendations on books or movies, or shows on Netflix and other mediums. We thought we’d return the favor this month. CODA is a heartwarming tale of love, family, dreams and inclusion and will have you laughing, thinking, wondering, and likely crying. Below is a link to the trailer. Enjoy.

Material Of A Less Serious Nature

One bright, beautiful Sunday morning, everyone in the tiny town of Johnstown got up early and went to the local church. Before the services started, the townspeople were sitting in the pews and talking about their lives, their families, etc.

Suddenly, Satan appeared at the front of the church. Everyone started screaming and running for the exit, trampling each other in a frantic effort to get away from this evil incarnate. Soon everyone was evacuated from the Church, except for one elderly gentleman who sat calmly in his pew, not moving, seemingly oblivious to the fact that the ultimate enemy was in his presence.

Now, this confused Satan a bit, so he walked up to the man and said, “Don’t you know who I am?”

The man replied “Yep, sure do.”

Satan asked, “Aren’t you afraid of me?”

“Nope, sure ain’t,” said the man.

Satan was a little perturbed at this and queried, “Why aren’t you afraid of me?”

The man calmly replied, “Been married to your sister for 48 years. . .”

The next 30 days could decide the Kingdom. What? Of course—my Giants, or the Dodgers (yuck)? And the NFL starts next Sunday. May my 49ers get back to the Super Bowl, and win this time. School is in full swing. A great time of year.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any. All performance data reflect the reinvestment of dividends and capital gains, where applicable.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money. This letter contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness. This letter contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, there is no guarantee that any views and opinions expressed herein will come to pass.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.