Introducing My New Book, Spiraling Up

As Bob Kargenian mentioned in last month’s newsletter, I will write the TABR Capital Management newsletter about every four months going forward. In this month’s newsletter, I’m thrilled to introduce my new book, Spiraling Up: Discover Financial Serenity, Make Work Optional, and Live Happily in Retirement, which is being launched today.

The best way to give you an idea of what the book is about is to share my publisher’s book description:

Why do some people effortlessly achieve financial success, yet others never do?

You’ve worked hard to become financially successful, but you still feel frustrated. Unfortunately, rising inflation, rampant consumerism, and the growing length of retirement make this scenario all too common. A million dollars just isn’t what it used to be. How can you finally stop worrying and begin enjoying the fruits of your success?

In Spiraling Up, financial planner Steven Medland lays out a deceptively simple plan to confidently grow and protect your wealth. Through clear and compelling real-life stories, he illustrates the proven principles that lead to financial serenity, making work optional, and living happily in retirement.

So, how do you create the virtuous cycle that leads to spiraling up financially? This book gives you the secrets that informed investors use to achieve financial freedom and retire with confidence. They will work for you, too.

This month I’m going to share the Spiraling Up Introduction, below, followed by some thoughts about inflation at the end of the newsletter.

Introduction

The Path to Wealth Is Simple, but Not Easy

When I was a junior in high school, the stock market crashed on October 19, 1987, a day that would go down in history as Black Monday. The Dow Jones Industrial Average lost over 22% of its value in a single day, and financial markets lost an estimated $1.7 trillion worldwide.

The next day, my high school economics teacher told my class that we should save a copy of that day’s Los Angeles Times because we were witnessing history.

My teacher also told my class that if we saved just $4,000 every year for 40 years and invested it wisely, we could all become millionaires by age 58. I went home and asked my dad if that was true, and he said it was. Then I asked him, “Why doesn’t everyone do that?” He replied, “It’s not easy, but with the right plan, the discipline to follow it, and enough time, just about anyone can become wealthy.”

It is now decades later, and after working with hundreds of wealthy families, most who are self-made, I believe my dad’s formula has withstood the test of time.

Overcoming the Powerful Forces Aligned against Us

However, as my dad said, it’s not easy. Simple, yes; easy, no. Some may have the right plan, the discipline to follow it, and enough time, but each of those elements is littered with roadblocks.

The deck is stacked against us when it comes to achieving financial and investment success. An insidious system is sabotaging our financial success, even if—and maybe especially if—we aren’t aware of it.

One of those forces is consumer culture, or feeling compelled to spend our money on certain material goods to attain the “right,” socially acceptable lifestyle. Consumption may help us temporarily feel better, but those feelings are fleeting. This is closely related to the concept of “Keeping up with the Joneses,” which originated in a comic strip of the same name back in 1913, demonstrating that using your neighbors as a benchmark to acquire more and more material goods is not a new phenomenon.

The media and social media are also significant factors. The media is supported by advertisers with one goal only—to part you from your hard-earned money—and social media bombards you with an idealized view of everyone else’s lifestyle. People tend to post pictures of themselves basking on a Hawaiian beach at sunset, not grinding away at the office or reaching their financial goals. These factors make us want to spend money on shiny stuff for instant gratification instead of focusing on longer-term objectives.

If these things aren’t challenging enough, we also live in an era when major structural changes are occurring in our retirement system itself. Employers have largely stopped offering pensions, so the burden of retirement savings falls squarely on us. And this is happening in a time when the Social Security system is underfunded and systematically falling behind relative to inflation.

Another challenge most of us struggle with is our own self-limiting beliefs. A limiting belief is an idea we think is true, but that constrains us in some way. These are often either handed down from our parents or have developed in our minds without ever being challenged. For example, believing that you have no control over becoming wealthy would likely prevent you from trying to build wealth in the first place.

I’m Financially Successful: Why Don’t I Feel That Way?

If you have had financial success but still aren’t where you want to be, you may have struggled internally with the above issues, even if you haven’t been able to articulate them. If that’s the case, I can assure you that you are not the only one who may be “wealthy” yet still feel anxious about your finances. And you’re also not alone if you haven’t understood how the above forces have been holding you back, or why you feel stuck while others around you appear to be racing ahead.

The good news is that you can overcome these challenges with the right knowledge, mindset, and skillset. Working with hundreds of families who have built their wealth gradually has taught me the rules to reaching financial security, but over time, I realized something was still missing.

I struggled with seeing objectively wealthy clients who still felt poor, and I’ve experienced some of the same feelings myself. However, I couldn’t find any resources that addressed this disconnect directly. Wasn’t there anything that explained how to build wealth and concurrently reach higher levels of contentment?

I studied the issue by talking with clients and reading literally hundreds of books, from the classics to contemporary bestsellers, with topics ranging from finance and psychology to personal growth. I wrote this book because it’s the one I wish I’d had earlier on my own journey, and in the hope that it can be a valuable guide for anyone who has grappled with these same issues.

Financial Security Is Achievable, but It’s Only the Beginning

Along the way, I discovered that financial security is only the starting point, and there are three higher levels of financial success. These include financial independence, financial freedom, and ultimately, financial serenity. I will discuss this in greater detail in Chapter 3, but financial serenity is essentially living in a state of financial abundance, gratitude, and tranquility.

Throughout decades as an investor and financial planner, I have only worked with a small number of individuals who live in financial serenity, a concept few have even heard of. That’s probably why it’s so rare. While it is possible to achieve and having wealth may help, wealth alone won’t get you there.

Over time, I observed a number of principles that, when followed, lead to financial serenity. Bookstore shelves are bulging with volumes that explain how to achieve wealth in dollar terms, but few, if any, explore the principles that lead to financial serenity.

Principles and Values

Billionaire investor Ray Dalio founded Bridgewater Associates and built it into the world’s largest hedge fund.

As he explains in his book, Principles:

Your values are what you consider important, literally what you “value.” Principles are what allow you to live a life consistent with those values. Principles connect your values to your actions; they are beacons that guide your actions, and help you successfully deal with the laws of reality. It is to your principles that you turn when you face hard choices.

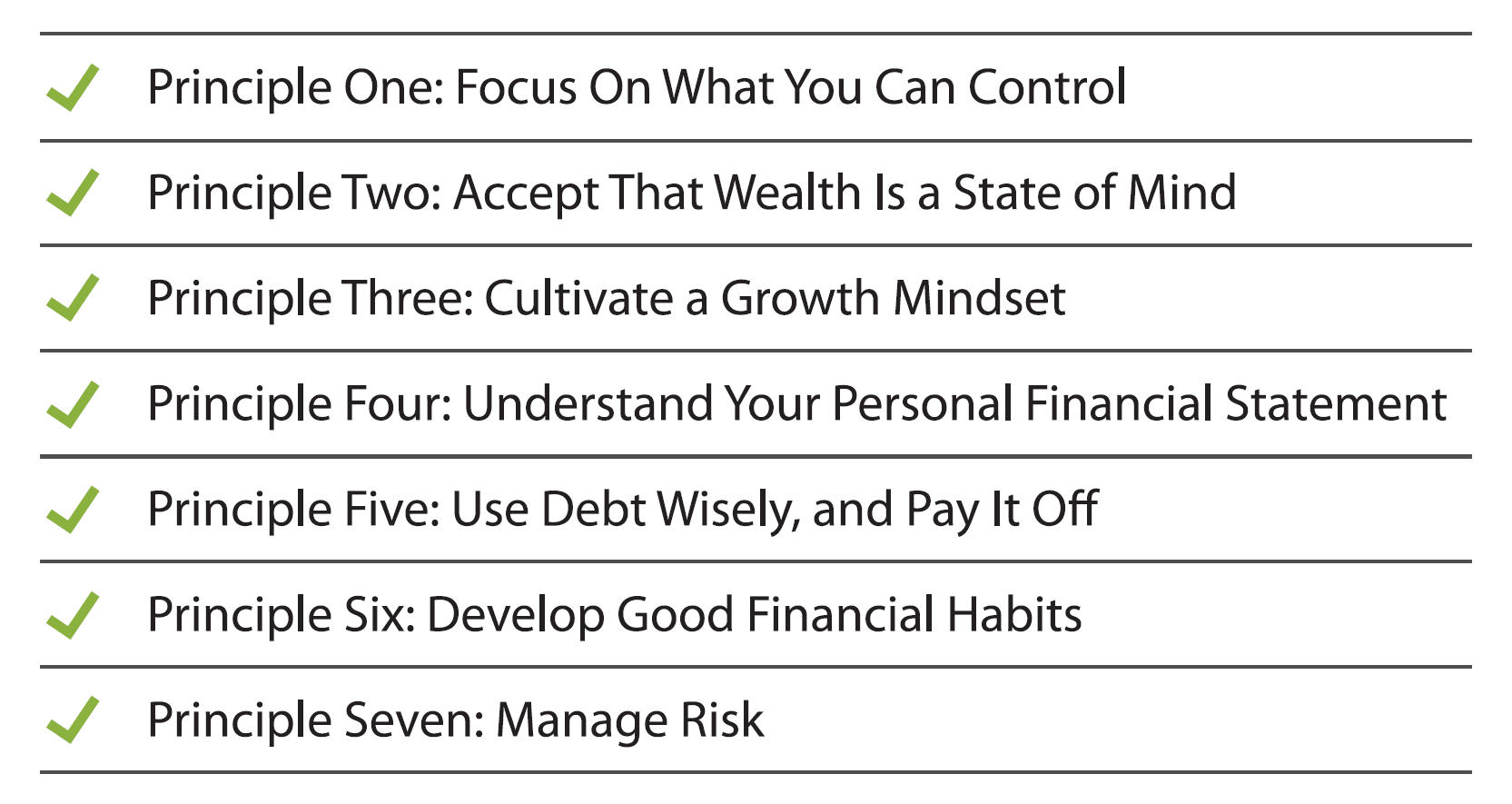

In short, principles are rules or codes of conduct that can help guide our actions in times of uncertainty. The seven principles of financial serenity that I have developed are in the graphic below.

The first three principles deal with our inner worlds or mindsets, and the last four deal with financial practices and strategies. Some of these principles have been around for millennia, and others are relatively new. In any case, I’ve seen firsthand that following each one in combination with the others is what leads to more desirable financial outcomes.

Spiraling Up to Financial Serenity

I have also seen that using these principles has a compounding effect. When we make good financial decisions, big or small, it leads to improved circumstances. Those improved circumstances lead to better opportunities, and those better opportunities open the door to even more beneficial financial decisions. This results in the virtuous cycle I call spiraling up.

This book is for those who value financial serenity and are willing to cultivate the above process to achieve it.

The first three chapters discuss the challenges we all face, followed by chapters on each of the seven principles illustrated by true client stories. I changed the names and details in each client story to protect the privacy of those involved. In most cases, I changed dollar amounts, used round numbers, and ignored taxes to make the examples easier to follow.

The final chapter is a remarkable, multigenerational true story of a family spiraling up by using each one of the principles. My ardent hope is that you also use them to achieve financial security, move to and beyond financial independence and freedom, and spiral up into financial serenity yourself.

Back to the 1987 Crash

So, what does the 1987 stock market crash have to do with spiraling up? The Los Angeles Times copy I mentioned above is displayed on my home office bookshelf today, serving as a reminder of my own long financial journey.

The blaring headline reads, “Stocks Plunge 508 Amid Panic: Record One-Day Decline Eclipses 1929 Market Drop.” This is an excellent example of why we should be cautious about the advice we get from the media. Hearing that the crash was even worse than the 1929 drop undoubtedly scared people out of the markets.

However, after the Dow Jones Industrial Average dropped 508 points and closed at 1,739 on October 19, 1987, it recovered and ended up closing above 35,000 for the first time 34 years later in 2021. While it was not possible to invest directly in the Dow Jones Industrial Average over that entire period because there was no index fund, Ned Davis Research estimates that during those 34 years, a $100,000 initial investment in the Dow would have grown to more than $4 million.

Someone who had the right plan, the discipline to follow it, and enough time could have done very well during this long period of economic growth and innovation, despite the many turbulent events along the way.

Anyone who invested right after the 1987 crash and didn’t look at their account again for 34 years until 2021 would be ecstatic with their account balance. However, that belies all of the challenges and ups and downs they would have faced during the interim period. That leads us to why financial success is so elusive, which is the subject of Chapter 1.

My publisher has agreed to discount the eBook version of Spiraling Up to $0.99 for launch week. Anyone who is interested in picking up a copy at the discounted rate can do so by clicking here.

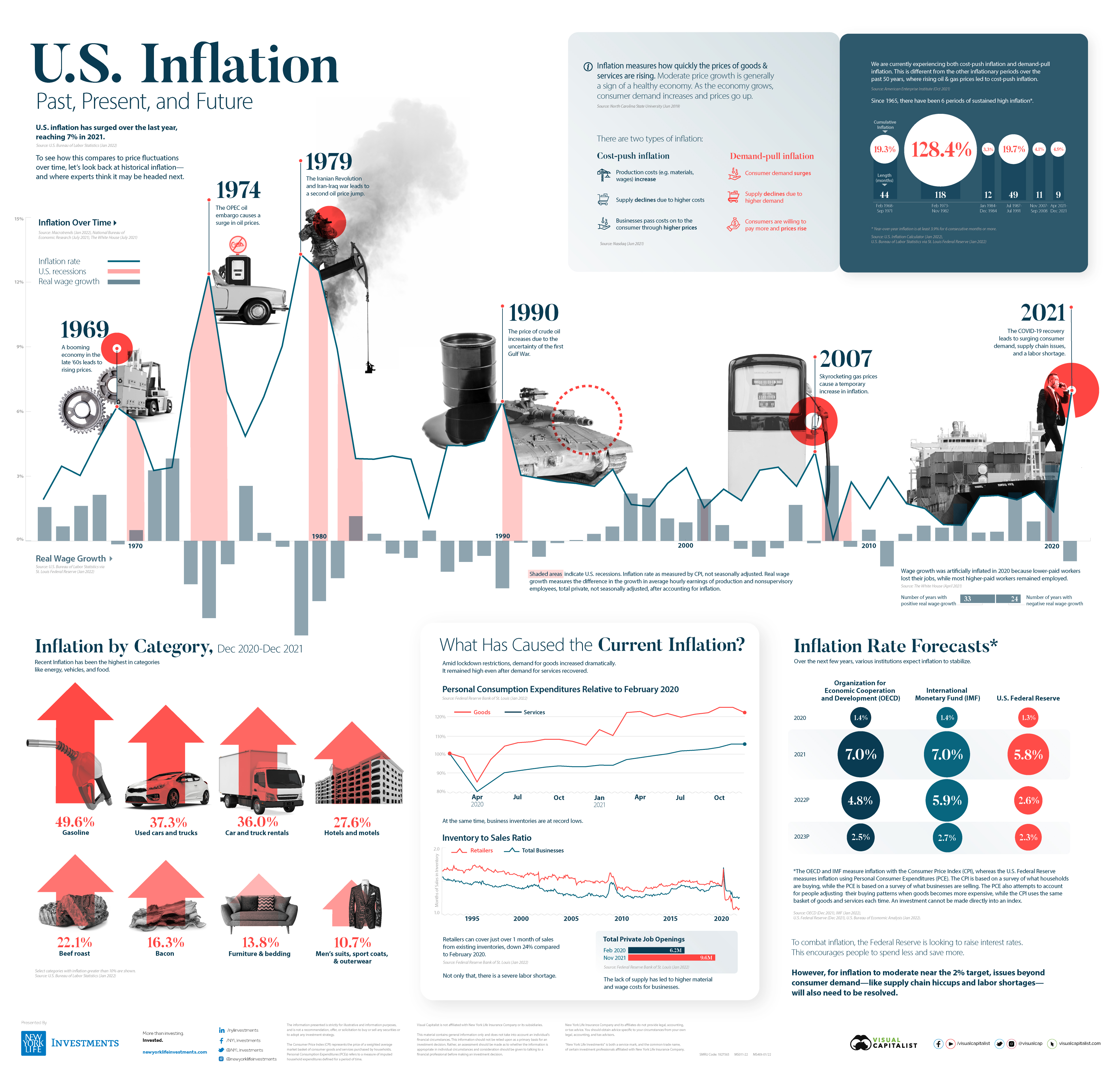

Rising Inflation

At the end of my book’s introduction, above, I give the example of $100,000 growing to over $4,000,000 when invested in the stock market for 34 years. A couple of things I don’t talk about until later in the book are 1) we’d never recommend someone investing 100% of their money in stocks, and 2) even as investments grow over time, the purchasing power of that money would drop significantly over those 34 years due to inflation.

After I dropped off my daughter at her high school this morning, I drove past a nearby gas station that was selling premium gasoline for $6.39 per gallon. Yikes! According to energy.gov, 34 years ago the average cost of a gallon of gas was $0.90 (gas prices in California tend to be higher than average for the country, but we’ll ignore that difference for the purposes of this discussion). The point is that inflation is something we all need to deal with as it’s not going away. It’s one of the primary reasons we need to take at least some level of investment risk; that’s the only way we can offset the erosion of our purchasing power over time.

I came across the interesting infographic below that has a big-picture view of US inflation going back decades, courtesy of Visual Capitalist. You can click on the graphic to view the high-resolution version.

As you can see, the last time inflation was this high was in the 1970s and early 1980s. The Federal Reserve is calling the current inflation “transitory” and predicting that the inflation rate will be closer to 2% later in 2022 and in 2023. That remains to be seen. For inflation to drop that much, consumer demand will need to drop, supply chain issues will have to be fixed, or labor shortages will have to be solved (or some combination of the three).

The Federal Reserve can raise interest rates to combat inflation because higher interest rates motivate consumers to save more and spend less. However, higher interest rates have a negative effect on stock prices, so the Fed is walking a tightrope. If their interest rate increases cause stocks to crash, they may have to delay further increases even though they want to reduce inflation.

TABR Investment Models

How will we navigate the markets as the Fed raises interest rates? We will continue to follow our investment models, which are currently all negative. As Bob Kargenian has written, we have been in a maximum defensive position since January 31.

Moderate accounts have about 12% in stocks and 4% in gold, with Conservative accounts having slightly less. We have no high yield bond exposure but are heavily invested in short-duration bond funds. When our models change, we’ll change. Bob and I will keep you informed in future updates, but feel free to reach out to us at any time with questions.

Thank you, as always, for your trust and confidence in all of us here at TABR.

Best regards,

Steven W. Medland, MBA, CFP®

Partner

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.