Listen To The Music (aka The Fed)

In their final meeting of 2021 last week, Fed Chairman Jerome Powell announced that the asset purchases the Fed has been making for about 18 months now at the clip of $140 billion per month, would not only be “tapered” further, but will now end in March of 2022.

At that point, the Fed will be removing on an annualized basis nearly $1.7 trillion of support to financial markets. We can’t know for certain what impact this will have, but I’m definitely in the camp of “this can’t be a positive.”

In recent years, Fed policy and interventions has become more important than ever before, so when the Fed sends a message that they will be tightening financial conditions, I’d suggest we take a lesson from The Doobie Brothers (1972), and Listen To The Music.

This will definitely be this year’s shortest monthly update, as we’ve just had a lot going on. Read on.

In This Case, The Music Is The Fed

As I write this just before Christmas Eve, the S&P 500 has closed at an all-time high. What’s not to like? It has been a solid year for most stock indexes, no doubt, but cracks are beginning to show up within the internal health of the market (participation, new highs diverging), and virtually no other index confirmed this recent high. It is hard to make a bearish case, as I think the index has tested its 50-day moving average 10 times this year, and every time, stocks mount a rally, often making new highs. Just 22 days ago, the S&P 500 closed at 4513, and looked to be teetering. Since then, it has rallied 4.7% in about 3 weeks.

One could argue that the Fed really isn’t going to be tightening credit conditions until they actually start raising rates. They’re just removing support. However, $1.7 trillion is a lot of money, and the question becomes, who (or what) replaces that? The Fed is not likely going to raise interest rates until sometime in the spring at a minimum, and current forecasts suggest only 3 increases next year in the Fed Funds rate to a level of 0.75%. For all we know, stocks may keep climbing next year, but to me, this is like removing the stilts from a building. How long will it hold up, especially with inflation figures continuing to roll in at rates of 6% and higher.

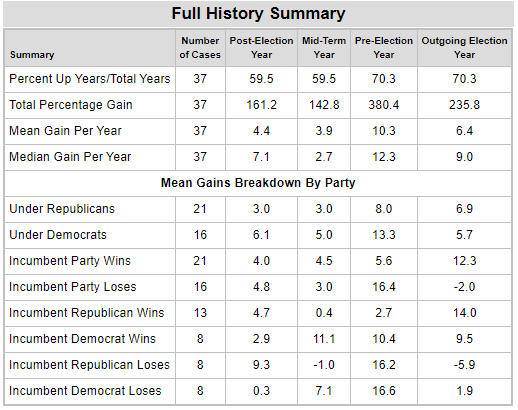

Next year has another headwind as well. Within the Presidential Cycle, it will be a Mid-Term Election Year. As the table below from Ned Davis Research shows, this portion of the cycle shows the lowest gain historically of any of the four years.

This data goes back to 1872, and you can see that the median gain per year in mid-term years is only 2.7%, by far the worst of the four years. Coupled with a Fed who is messaging that things will not be as supportive as the past 18 months, I think investors should indeed heed the Doobie Brothers hit song, and Listen To The Music. At best, we’re Living On The Fault Line (1977), and we could be in for Nothin’ But A Heartache. Yes, those are also songs from the Doobie Brothers, who also have a new album out, Liberte’. And, no, we’re not on their publicity team!

Current Portfolio Allocations

From a technical standpoint, I can say that stocks look weaker from a breadth perspective more so than at any time in the past 18 months. But, our models are still 3 of 5 positive for stocks, and likely to switch back to 4 of 5 this weekend, which will have us increase our tactical equity portion from 60% to 80% invested. Candidly, every “sell” from one of our models this year has been met with higher prices. This is the price of risk management. The deterioration that took place in November has once again been met by a decent rally, but as noted above, nothing is confirming the S&P’s new high. At some point, this will matter. But, not now, and not likely the last week of the calendar year, which usually has a strong upward bias. In bonds, our high yield bond risk model generated a SELL on November 29, the first such change in 13 months. We’re now using two variations of our model, so this shift caused us to move 50% of our high yield bond positions into short term bond funds. Like stocks, our SELL has been met by rising prices, but not yet enough for our model to reverse. This portion of our fixed income exposure is now 50% in high yield, and 50% in short duration bond funds.

Bottom line, I can give you all the conjecture you want about headwinds, Fed tightening, cycles and so on, but please remember this is not a forecast that next year will be down, or terrible. It very well may be. So far, though, our models are not necessarily that negative.

Welcome, Tracy Curtis

Today marks the ninth day for Tracy at TABR, who is in the midst of assuming the role of Mary Hernandez as our Office Manager and Senior Client Services Specialist. Mary will be officially retiring in mid-January, and is sharing as much wisdom as possible in the next month with Tracy of her 18 years at TABR.

Tracy comes to us after a recent stint at DST Wealth Management in Indian Wells, where she handled a variety of roles. She has just finished her B.S. in Management at Pepperdine University, and moved to Orange County from La Quinta, CA with her beloved Chihauhau, Wilson. All of us at TABR are excited to have Tracy join our team, much as we are saddened to see Mary leave. More on Mary next month. Make sure to introduce yourself to Tracy the next time you call, and many of you will also get to meet her during your next office visit.

Family Time With The Medlands

Some of you have been with me for over 35 years. And a large number certainly over 20. As a result, from afar and sometimes within conversations, you’ve watched our kids grow up (Bob’s and Steve’s). In that vein, below are recent photos of Steve’s no longer little ones, Audrey (14) and Conrad (12).

Audrey, above, loves the snow when it is available (!), is a freshman at Dana Hills High School, and also loves the beach and spending time with her friends.

Conrad, below, is halfway through middle school. He ran cross country this year, and plans to return to that next school year.

Team LaRoi

A year ago, our son, Adam (below), was unemployed for the better part of 9 months. Covid pretty much shut down the entire live music industry, and his focus has been fashion and music in his role as a freelance photographer after graduating from NYU with a major in photo.

Earlier this year, though, he was recommended for a job shooting photo, video and a documentary for the Kid LaRoi, a young pop/rap singer from Australia (see LaRoi below).

Adam has been with LaRoi and his team since May, and they are preparing for a world tour which begins in Los Angeles in early February. In July, LaRoi cut a single with Justin Bieber called Stay, which had been the Number One pop song in America for nearly 7 months until Adele had the audacity to release her new album. Another hugely popular song of his is Without You, with Miley Cyrus. LaRoi and his team work extremely hard, and Adam is enjoying his time with them, doing what he loves.

Material Of A Less Serious Nature

Fifty-one years ago, Herman James, a North Carolina mountain man, was drafted by the Army. On his first day in basic training, the Army issued him a comb. That afternoon, the Army barber shaved off all his hair. On his second day, the Army issued him a toothbrush. That afternoon the Army dentist yanked seven of his teeth. On the third day, the Army issued him a jockstrap. The Army has been looking for Herman for 51 years.

No doubt, that is the best sentiment we can share with you. Thanks for the trust and confidence you place in all of us at TABR. May you celebrate a Happy Hanukkah, Merry Christmas, and a Happy New Year with friends, family and all of your loved ones.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

Inverse ETFs

An investment in an Inverse ETF involves risk, including loss of investment. Inverse ETFs or “short funds” track an index or benchmark and seek to deliver returns that are the opposite of the returns of the index or benchmark. If an index goes up, then the inverse ETF goes down, and vice versa. Inverse ETFs are a means to profit from and hedge exposure to a downward moving market.

Inverse ETF shareholders are subject to the risks stemming from an upward market, as inverse ETFs are designed to benefit from a downward market. Most inverse ETFs reset daily and are designed to achieve their stated objectives on a daily basis. The performance over longer periods of time, including weeks or months, can differ significantly from the underlying benchmark or index. Therefore, inverse ETFs may pose a risk of loss for buy-and-hold investors with intermediate or long-term horizons and significant losses are possible even if the long-term performance of an index or benchmark shows a loss or gain. Inverse ETFs may be less tax-efficient than traditional ETFs because daily resets can cause the inverse ETF to realize significant short-term capital gains that may not be offset by a loss.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.