Navigating the Loss of the Stretch IRA Under the SECURE Act

Last month, I attended an intensive Friday-Saturday IRA workshop that focused on the many changes to IRA regulations in recent years. Ed Slott hosted the workshop. He’s a CPA and IRA expert, and you may recognize his name from the Retirement Freedom specials on PBS. I initially met Ed in 2005, the first time I attended one of his workshops, and I’ve always been impressed with his expertise and knack for entertaining explanations of inherently complex topics.

The most recent workshop I attended was particularly noteworthy, as it has significant implications for all of our clients with an IRA account. These changes are due to the SECURE Act, or Setting Every Community Up for Retirement Enhancement Act, a law passed in 2019 attempting to improve retirement savings options for Americans. Despite the good intentions, you’ll see not all of the changes were an improvement.

In this month’s newsletter, I’ll discuss the implications of the SECURE Act on your retirement accounts, along with our recommendations. I’ll also share a handy tax checklist, a true client story about spousal support, a stealthy tax increase for California taxpayers, TABR’s 20th anniversary, and our current investment allocations. And make sure to watch the hilarious 2-minute video at the end.

Now, back to the SECURE Act. This new law has many implications for IRA accounts, and they fall into two main categories:

1) The SECURE Act’s first significant change was the impact on the “stretch IRA.”

Before the SECURE Act, beneficiaries of inherited IRAs could “stretch” withdrawals and tax payments over their lifetimes, allowing for compound tax-deferred growth of the inherited funds. In other words, IRA beneficiaries could take small annual Required Minimum Withdrawals (RMDs) over the remaining years of their life, maximizing the tax deferral benefits.

Let’s take the example of a 50-year-old beneficiary, Jen, who inherited a $1 million IRA from her mom in 2018, before the SECURE Act was enacted (all names and details in this newsletter’s client stories have been changed to protect privacy). Jen was in her peak earning years and making $150,000 per year, putting her in the 24% federal tax bracket. Her 75-year-old mom was living off Social Security and IRA withdrawals and was in the 12% federal tax bracket.

Prior to the SECURE Act, Jen could take RMDs based on her remaining 36.2-year life expectancy, which comes from an IRA table forming the basis for the RMD calculation.

At age 50, Jen would divide the $1 million IRA balance by 36.2, which results in a $27,624 RMD. That 36.2 number would be reduced by 1 each year for the rest of her life to determine her RMD. Therefore, at age 51, she would divide that year’s IRA balance (say, $980,000 in this example) by 35.2 (her initial 36.2 life expectancy minus 1). That would mean at age 51, she’d have to withdraw $27,840 ($980,000 divided by 35.2).

This would continue each year of her life, providing Jen with additional annual income, and allowing her to remain in the 24% federal tax bracket. Jen could withdraw more than the RMD amounts, but doing so could put her in a higher tax bracket and wipe out the benefits of a lifetime of tax-deferred IRA growth.

Again, the example above is before the SECURE Act was enacted. Unfortunately, the SECURE Act eliminates the stretch IRA strategy for most non-spouse beneficiaries.

Under the SECURE Act, non-spouse beneficiaries, such as children or grandchildren, generally must withdraw all funds from the inherited IRA within 10 years of the original account owner’s death. This means beneficiaries will likely face larger tax burdens in a shorter timeframe compared to the previous stretch IRA rules.

If Jen were to inherit the same $1 million IRA today under the new SECURE Act rules, she would be required to empty the IRA account by the end of the 10th year after the year of death – the 10-year rule. Because Jen’s mom was over age 73 and was taking RMDs when she passed away, Jen would also have to take RMDs for the 10 years that she is emptying the IRA account.

To simplify the example, let’s say Jen takes out 10% of the account each year for 10 years. That would mean an annual $100,000 withdrawal, pushing her from the 24% tax bracket to the 35% tax bracket each year. That’s $350,000 of taxes over 10 years, significantly higher than Jen would have paid under the rules prior to the SECURE Act.

One bright spot is that certain exceptions apply to the 10-year rule, such as for:

- Surviving spouses

- Minor children of the account owner (but not grandchildren)

- Disabled individuals

- Chronically ill individuals

- Those not more than 10 years younger than the IRA owner (or those older than the IRA owner)

The individuals above are still eligible for the stretch IRA, but most beneficiaries no longer have that option. The key point is that the SECURE Act significantly alters the landscape for inherited IRAs and requires IRA owners and beneficiaries to adjust their financial planning strategies accordingly.

2) The SECURE Act’s second significant change is that Traditional IRA accounts are no longer the preferred vehicle for retirement savings.

This stems from the SECURE Act, partly due to the loss of the stretch IRA discussed above and partly due to the fact that we’re at historically low top marginal tax rates (believe it or not). Please see the chart below, showing the top marginal tax bracket going back to 1913:

Copyright © 2024, Ed Slott and Company, LLC. Reprinted with permission. Ed Slott and Company, LLC takes no responsibility for the current accuracy of this information.

The chart shows that although most people feel like they’re paying too much in taxes, the rates are very low by historical standards. Just look at the top rate of 91% or more for the 17 years from 1946 to 1963. Ouch!

So what does this mean for IRA accounts today? Contributing to a Traditional IRA account or a Traditional 401(k) allows a taxpayer to save money on taxes now by reducing their taxable income, but they will eventually pay taxes when they withdraw funds from that account, usually in retirement.

If you’re currently in the top 37% tax bracket and making Traditional IRA contributions, you’re saving 37% in taxes due to the ability to deduct your contributions and reduce your taxable income. That sounds great, but what happens if you retire and tax rates increase to, say, 45%? If you pull those funds out in retirement and pay 45%, you would have been better off paying the 37% rate up front and putting that money in a Roth IRA instead of a Traditional IRA.

Roth IRAs and Roth 401(k) accounts are the opposite of Traditional IRAs. With Roth accounts, taxpayers don’t save any money on taxes when they put money into them, but the investments grow tax-free, and they don’t pay taxes when they withdraw funds from the account in retirement (as long as the funds have been in the account for 5 years and they are over 59 1/2 years old).

Let’s go back to the example of Jen, who inherited the Traditional IRA from her mom. Her mom was in the 12% tax bracket in retirement, so she’d have to pay $1,200 for every $10,000 she withdrew from the IRA account. She could have converted her Traditional IRA to a Roth IRA account year-by-year and paid 12% in taxes, and Jen would have inherited the Roth IRA account tax-free.

Unfortunately, her mom didn’t do any Roth IRA conversions. Due to the SECURE Act changes outlined above and the $100,000 annual withdrawals, Jen will be in the 35% tax bracket and have to pay $35,000 in federal tax each of the 10 years she withdraws $100,000 from the IRA. Again, that’s $350,000 in taxes over 10 years, significantly higher than her mom would have paid to do the Roth IRA conversions over time.

The above is a simplified example showing a daughter inheriting funds from her mom, but the SECURE Act makes things even more complicated if an IRA owner names their estate, a charity, or a Trust as their beneficiary. Some of these situations can result in the IRA having to be emptied by the end of the 5th year after the year of death (the 5-year rule), potentially pushing beneficiaries into an even higher tax bracket than would result from the 10-year rule.

Either way, given the current low tax rates and loss of the stretch IRA, Roth accounts are much more compelling retirement vehicles than Traditional IRAs.

Recommended Actions

First of all, review your IRA account beneficiaries. If you have named a Trust account or your estate as the beneficiary, you should consult with your estate planning attorney and strongly consider naming an individual or individuals instead. This one change could allow your beneficiaries to stretch the IRA distributions over 10 years or potentially over their entire lives instead of being forced to take distributions over 5 years and pay higher taxes as a result. The IRA Required Minimum Distribution rules are more complicated than they’ve ever been, so please call us if you’d like to review your specific situation.

Next, consider getting the funds out of your Traditional IRA by spending down those assets first in retirement. We helped a client with four children do this, and she is now living off withdrawals from her Trust account instead of her IRA. This helped her kids in two ways. First, their mom withdrew the IRA assets when she was retired and in a low tax bracket, minimizing the taxes they would have paid if they inherited her IRA instead of her Trust. Second, they won’t have to deal with the drawn-out process of inheriting her IRA account and the RMDs it would entail.

Instead of spending down the assets in a Traditional IRA, another option is converting it to a Roth IRA, which can be done a little bit each year to minimize taxes. Many CPAs have a three-word mantra when it comes to tax planning: “Defer, defer, defer.” However, the tax landscape has changed. If taxes will be higher in the future than they are today, it’s better to pay taxes earlier when the rates are lower than to defer taxes and face potentially higher rates.

Of course, these recommendations depend heavily on your specific situation. Please call or email us anytime to discuss your IRA beneficiaries, accelerating IRA withdrawals, or whether a Roth IRA conversion makes sense for you.

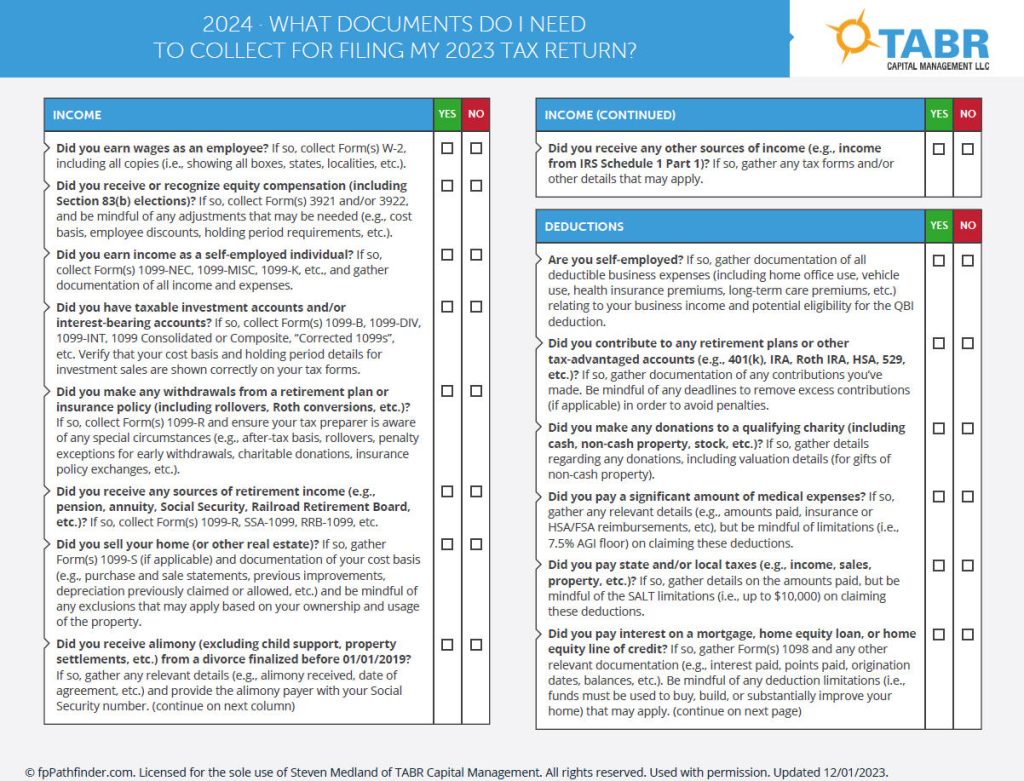

A Handy Checklist for Your Taxes

Tax Day is Monday, April 15, 2024, barely a month away. We thought the checklist below might be helpful as you gather your tax documents for your accountant. You can download a PDF version by clicking on the image below.

Remember that you can make 2023 Roth and Traditional IRA contributions up until April 15 of this year, and the 2023 contribution deadline for SEP IRAs is the employer’s 2024 tax filing deadline. The Roth and Traditional IRA contribution limits for 2023 are $6,500 for those under 50 and $7,500 for those 50 and above. For 2024, the limits are $7,000 for those under 50 and $8,000 for those 50 and above.

If you’d like to review the IRA contribution limits, tax rates, or other important financial numbers for 2024, you can click below to download our 2-page guide.

True Client Story – A Win/Win for Spousal Support

We recently met with one of our clients, James, for our annual review, and we had a line item showing $48,000 per year in spousal support for his ex-wife, Susan. We asked how old Susan was now, and she turned 66 last year. Ages ranging from 66 to 67 are a magic number for Social Security, known as the Full Retirement Age (FRA). The FRA varies based on birth year and ranges from age 66 for those born before 1955 to age 67 for those born in 1960 or later.

The FRA is the age at which Social Security recipients can receive 100% of their benefits, as opposed to a reduced benefit at an earlier age. In our client’s case, he was the higher earner, so his ex-wife could receive a higher benefit by taking her spousal benefit, which is 50% of his FRA benefit.

That meant that Susan was eligible to start receiving $2,000 per month in Social Security benefits. Per their divorce agreement, James was able to reduce his spousal support payments by the corresponding amount when Susan started Social Security benefits. Saving $2,000 per month was clearly a win for James, but how did it also benefit Susan?

Because they were divorced before 2019, Susan’s spousal support payments were fully taxable to her as income. The $2,000 she is still receiving in spousal support continues to be taxed as income, but the $2,000 of her new Social Security income is not taxed at all on her California tax return, and only 85% of that is taxable on her federal return.

Neither of them would have realized these benefits without our financial planning process, and this is just one example of the advantages of doing regular annual reviews.

A Stealthy California Tax Increase

Bob Kargenian recently pointed out a new change to California’s State Disability Insurance (SDI) program that has flown mostly under the radar. The change, originating from Senate Bill 951 (SB 951), increased taxes for Californians starting on January 1, 2024. The bill introduced several changes to California’s Unemployment Insurance Code and State Disability payments with the intention of increasing benefits for residents in need.

The new law has two tax components. The first change is increasing the California SDI rate from 0.9% last year to 1.1% this year. The more significant change is eliminating the taxable wage limit. Last year, only income up to the $153,164 taxable wage limit was subject to California SDI tax withholding, but now all income is.

This applies to all wages, including base pay, bonuses, equity incentives, and deferred compensation. Employees will pay these higher California SDI taxes through automatic deductions from their paychecks.

TABR’s 20th Anniversary

It’s hard to believe that TABR celebrated its 20th anniversary last month. How time flies. It’s been an incredible journey, and we owe it all to you, our wonderful clients.

We established TABR on February 6, 2004, and for two decades, we’ve had the privilege of guiding you toward your financial goals, helping you plan for the future, and navigating the ever-changing investment and financial planning landscape. Your trust and loyalty have been the cornerstone of our success, and we are deeply grateful for the opportunity to serve you.

As we reflect on this milestone, we want to extend our heartfelt thanks to you. Your support, feedback, and collaboration have been invaluable to us, and we look forward to continuing to serve you for many years to come.

Thank you for entrusting us with your financial future. Here’s to 20 years of partnership, growth, and success!

Our Current Investment Allocations

Since Bob Kargenian wrote our last monthly newsletter on February 9, there have been minimal changes to our investment stance. We reduced our stock exposure yesterday from 83% to 66%, as now 4 of our 6 stock market risk models are on BUY signals. Our high yield bond fund risk model is still on its November 3 BUY signal.

Our most aggressive strategy is our OEX/S&P 500 Relative Strength Stock process. It’s an all-stock account, and we don’t play defense like we do in tactical accounts. That means it will likely perform the worst of all TABR strategies in down years and the best when the market is going up. It currently owns stocks like Meta, Broadcom and Nvidia that have garnered more of their share of news headlines in recent years. But, we won’t own them forever. When they lose momentum, and fall in our ranking process, they are automatically sold and replaced with other leading stocks. This is a repeatable, disciplined process we employ monthly.

These stocks remind me of the regret investors may feel when they don’t own them, which made me think of the 2-minute video below. It’s originally from Conan O’Brien and has a humorous look at hindsight bias. Enjoy!

All of us here at TABR Capital Management hope you enjoy the coming of spring, and we thank you again for 20 years of your continued trust and confidence.

Best regards,

Steven W. Medland, MBA, CFP®

Partner

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.