Offense Sells Tickets, Defense Wins Championships

A few weeks ago, the Carolina Panthers played the Denver Broncos in the 2016 Super Bowl. Carolina entered the game with the top-ranked offense in the league, scoring 500 points, more than any other team. Meanwhile, the Broncos had the top-ranked defense, based on several categories, and only 3 other teams had allowed fewer points than Denver.

During the telecast, I remember the announcers saying that in the past, when one of the two teams participating had the #1 defense in the league, they had won 9 of the 11 games. Guess what? Despite having a 39-year old Peyton Manning at QB, who is currently a shell of his former All-Pro years, the Broncos won, because of their defense.

This gives me concern, in that my favorite hockey team, the Dallas Stars, are currently the top scoring team in the NHL, and have the second best record as I write this, but their defense and goaltending are mediocre at best. As much as I may wish otherwise, this leads me to believe that unless they improve defensively, out-scoring the opposition in the playoffs is probably not going to work, and they are not going to win the Stanley Cup.

You may be asking—what the heck does this have to do with investing and portfolio management, and the achievement of your financial goals? Well, actually, quite a lot. You see, it does one little good to earn high returns in a bull market, only to give most of them back in the ensuing bear market. It reminds me of a commercial that used to run in the 1980’s by what I remember was a major savings and loan, and the slogan they used in one of the ad campaigns was “It’s Not What You Earn, It’s What You Keep.”

There are a lot of areas I could use that analogy with investments, but for now, we’ll keep it within the context of what has been happening with financial markets worldwide since last May—mainly, that stock prices are in major downtrends.

Near Term Positive and Critical Support

On February 11, stock indexes closed at new lows for the year, and from the peaks last year. At that point, the S&P 500 Index was down over -14% on a closing basis from its high, the S&P Mid Cap Index was down -20%, the Vanguard Total International Stock Index was down -26%, and the Russell 2000 Index of small companies was also down over -26%.

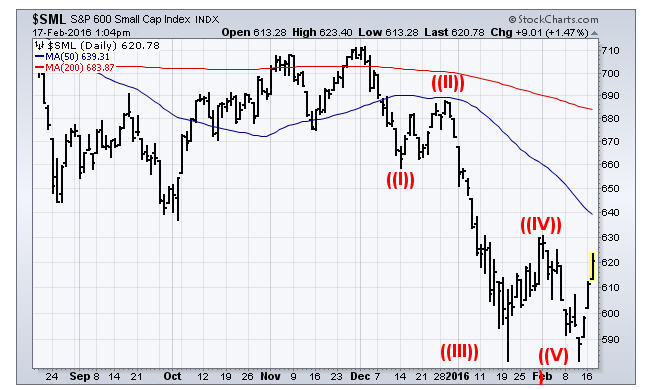

It’s a fair question to ask—is it possible the worst is over? The chart below is that of the S&P 600 Small Cap Index, courtesy of www.stockcharts.com.

It shows a clear five-wave decline from its November peak. Internal data showed several positive divergences, with fewer stocks making new lows, and a lessening of downside momentum in a number of areas. We used this decline to cover some of our hedges, expecting a rally, and that is exactly what has transpired the last two weeks, with prices rebounding nearly 7% thus far. In addition, our high yield bond models have improved significantly, generating BUY signals, and lending support to possible further rally.

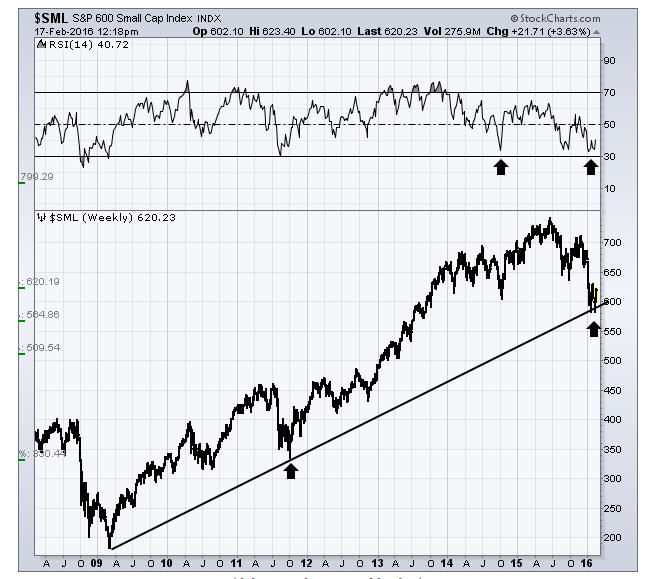

For additional context, below is a longer term chart of the same index. The decline stopped at the 600 level, on the long term uptrend support line which goes back to the 2009 lows. A similar support zone is at the 1800 level on the S&P 500 Index. Thus far, the bear market in stocks has had two legs down.

There is no way to know how many it will have before the bear market is complete, but based on valuations and the overall technical evidence, the probabilities highly favor a break of this major support in coming weeks and months, with likely targets for the S&P 500 in the 1550-1700 zone, as conveyed in last month’s update. I have no particular crystal ball in regards to a recession in the U.S., nor is there any way to know how long this malaise in world stock markets may last. It might be over in 4 months, or it could last another two years.

Where We Currently Stand

Our real estate model went negative in January, and our high yield bond risk models just turned positive, so we’ll be adding exposure to that area for the first time since November. The last BUY signal for this area was a failure, taking place within the downtrend in stocks, and there is a real possibility that the new signal may meet the same feat. But one never knows, and that is why we have the discipline to follow our process, because that is how you achieve results over time.

We began the year with portfolios positioned fairly conservatively, and more defense was added pretty quickly, as several of our models deteriorated. As a result, our tactical portfolios are experiencing a much smoother ride than others, which is one of our main objectives for clients. There will be a time to make rain—just not yet.

Within the stock market, at present only 2 of the 10 primary risk models we use are in a positive mode, so our tactical equity allocations are running at about 25%. Our best guess is this rally will eventually terminate with no more than another 3-4% of upside, whereas we think the downside has at least 15% from current levels.

Material of A Less Serious Nature

A mafia Godfather is convinced that his bookkeeper, Guido, has embezzled $1 million from the family. Guido is deaf—a big reason he got the job. If it ever came to it, he would have a very hard time testifying in court. The Godfather confronts Guido about his missing money and brings along his lawyer who knows sign language.

The Godfather tells the lawyer, “Ask him where the money is!”

The lawyer, using sign language, asks Guido, “Where’s his money?”

Guido signs back, “I don’t know what you’re talking about. I didn’t steal anything.”

The lawyer tells the Don, “Guido says he doesn’t know anything about the missing money.”

The Godfather pulls out his pistol and puts it to Guido’s head and says to the lawyer, “Tell him he has ten seconds to spill his guts.”

The lawyer signs to a nervous Guido, “He’ll kill you if you don’t tell him what you did with the money.”

Guido, now trembling with fear, signs, “OK, you win. The money is in a brown duffle bag buried behind the shed at my cousin Bruno’s house.”

The Godfather asks the lawyer, “What did he say.”

The lawyer replies, “He says you don’t have the balls to pull the trigger.”

Please know that when our models suggest a more positive risk environment, we’ll be happy to pull the trigger. And remember, baseball season has started, so things can’t be all bad.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.