Oil Price Spikes Not As Harmful As One Might Think

If I told you six weeks ago the price of oil would surge over 45% in a few weeks, you’d probably assume this would be bad for the stock market. It was, and then it wasn’t, as the market seems to have sensed the peak in oil was two weeks ago.

More on this inside, along with a more interesting look at the six-month seasonal pattern which is approaching, and my short take on AI. There’s also a quick note on QCDs (qualified charitable distributions), and of course, what’s a month without humor?

There’s More To Oil Price Spikes Than Meets The Eye

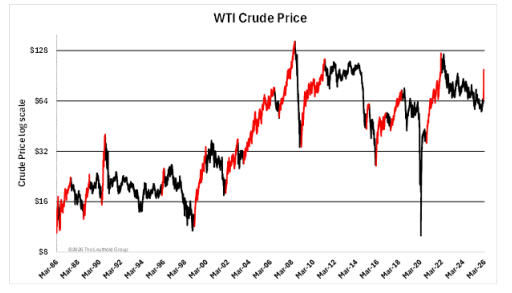

They say a picture is worth a thousand words, so look below at the chart of Crude Oil, which has spiked nearly 50% since February 27, the day before the United States attacked Iran.

As a result, the price of gasoline at the pump nationwide has surged over $1 per gallon, and even more in California, where extra taxes and regulations bump the cost of a gallon to the $5.80 to $6.50 range, depending on the location and the gas station (i.e., you’ll pay more at Chevron than at a 7-11 or an ARCO). This represents the sharpest monthly increase on record for gas prices.

Because of the jump in energy prices, inflation spiked in March, gaining 0.9%, with annual inflation now at 3.3% for the past 12 months, versus just 2.4% in February. Should oil prices remain elevated, it is easy to see inflation accelerating to over 4% year-over-year in the next two months.

This sounds pretty scary and ominous, and one would think that stocks would crater on such news. And initially, they did, with the S&P 500 falling from 6879 to 6343 from the day before the attack to March 30, a decline of -7.79%. Stocks, however, have a way of discounting the future, often way before the news becomes positive or negative. A two-week truce between the U.S. and Iran was announced early on April 8, but stocks bottomed on March 30 and as of the close on April 14, had risen 9.83% from that date, and are actually above the level BEFORE the war started, even with the price of oil still significantly elevated.

At least at present, most or all of the bad news was apparently already priced into the market, and now the market is looking to the future, and perhaps getting back to basics, such as corporate earnings, which started pouring in on Tuesday.

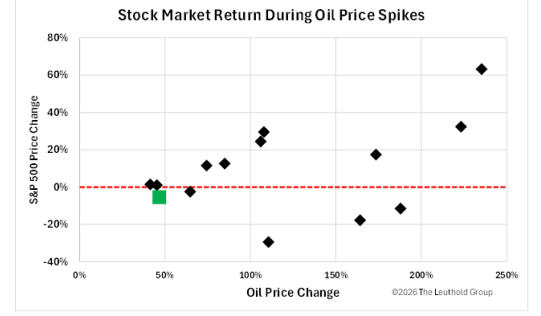

A more quantitative and objective look at the impact of a substantial jump in oil prices on the stock market was published earlier this month by friend Scott Opsal of the Leuthold Group. Opsal began his quest by looking for 30-day periods that recorded an increase in the price of oil greater than 20%. His process left him with 15 episodes going back to 1986 which fit the description of a major upward spike. For reference, see the chart below.

The oil price spikes are denoted by the red segments in the chart. Opsal found the average duration of a decisive oil price spike was nearly 11 months. Currently, we’re barely 7 weeks in this one. The burning question, though, is. . .what was the response of stock prices to a big jump in oil? Look at the chart below.

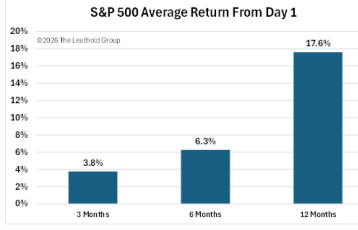

In the chart above, the x-axis plots the oil price change in percentage terms, while the y-axis plots the price movement of the S&P 500 Index. According to Opsal, the only time a bear market came about as a result of an oil price spike was in 2002. The average return across all periods was +10%. This is backed up by the chart below, which calculated the average S&P 500 price change over the 3-, 6- and 12-months measured from the first day of the oil price spike.

What’s notable is the average gain after 12 months of over 17%, which is about 70% greater than the norm. In fact, Opsal found that in seven of the 15 prior cases, the S&P 500 rose by more than 24% in the year following the initial jump in oil prices.

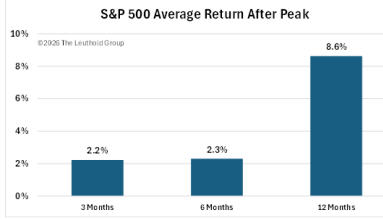

Finally, the chart below plots the average gain in the S&P 500 for the 3-, 6- and 12-month periods after the peak oil price is attained. This, of course, can only be known in hindsight.

Thus far, crude oil has peaked on April 3 at $112 per barrel, and has declined over -18% since then. Given the truce and perhaps an eventual negotiated settlement, it’s possible the oil market is already thinking the worst is over. But, we really don’t know, do we? Based on the data above, though, there is not likely to be much more left in the tank (pun intended here) from current levels for the next six months.

The bottom line is, oil price spikes aren’t as negative for stock prices as one might assume. This is just one reason why we trust our models to guide our exposure in and out of markets, and not faulty, worrisome assumptions. I will say this, though. From the reading I’ve been doing on the Strait of Hormuz, it’s my understanding that even with a possible settlement in the war soon, it will likely be many, many months before things return to normal with the shipping lanes.

If oil prices stay elevated for another two months, the likelihood of printing 4% or greater year-over-year inflation by June will be a high probability, and that will likely kill the stock market’s upward momentum. We’ll know a lot more by June 30. Meanwhile, we’re about to enter the worst six-month period of the year for stocks.

Maybe You Should SELL This May And Go Away?

In the late 1980s and 1990s, I was fascinated by the seasonality research from the likes of Yale Hirsch, Norm Fosback and Jay Kaeppel. I even authored a few articles on the topic of month-end and holiday seasonals for Stocks and Commodities Magazine in that time period. In reality, though, during that time period until around 2003, other than the six-month period we’re about to talk about, there was no practical way to implement the strategies of going in and out of the stock market with ease. Then, and even now, I began to question the WHY part of seasonals. In other words, I have a set of rules that tells me to invest (or not) in stocks simply based on the calendar, with no input as to how the stock market is actually behaving? Yep.

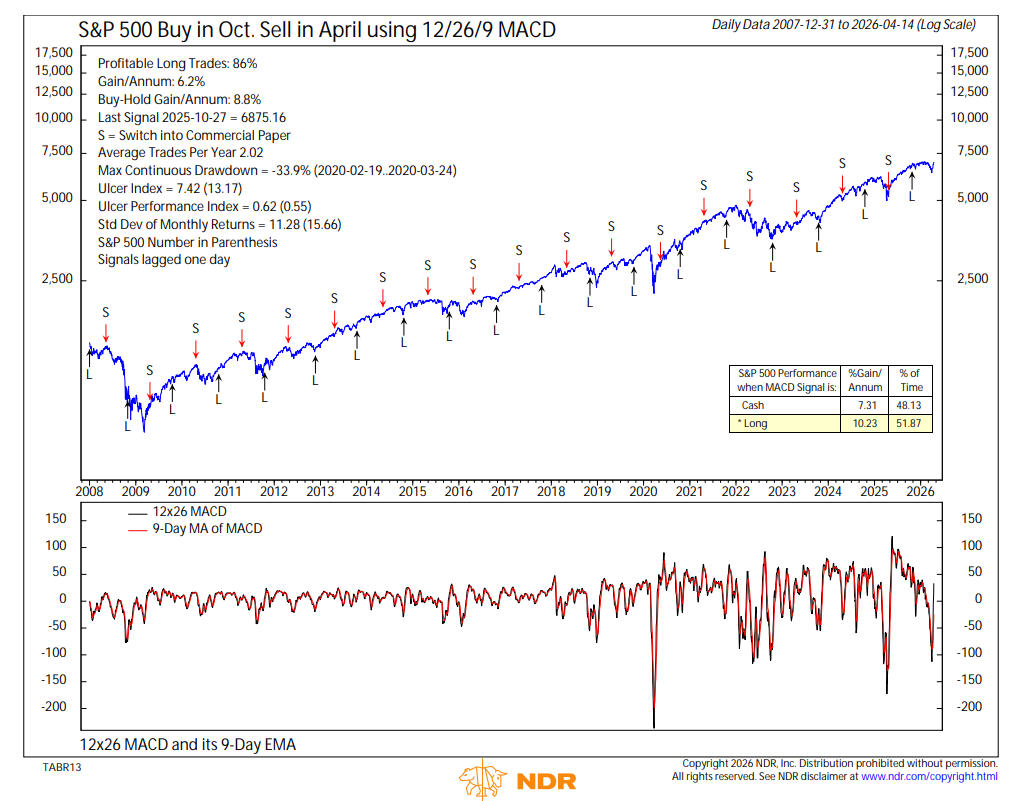

Much of the data was quite compelling. Roughly, from 1950 to about 2007, if you only invested in the S&P 500 from November 1 to April 30, and went to cash for the other six months, you would have actually beaten buying and holding the index for the entire year, and taken about 50% less risk by being in cash. For a risk manager, it doesn’t get much better than that. Like any good secret, though, if everybody knows it, it stops working. That seems to be the case with the “Best Six Months.” Though we adapted this with a twist on one of the indicators to better time entry and exits, the chart below courtesy of our work with Ned Davis Research (www.ndr.com), shows the results of this strategy going back to 2007.

With about two weeks to go as I write this on April 15, the S&P 500 Index is up less than 2% since the entry in late October 2025, yet had you exited the so-called unfavorable period from May through October last summer, you would have missed out on a gain of about 22%. So much for the “worst” six months. But it turns out there is more to the data. It turns out that only once in the four years of the Presidential Cycle does this pattern have any statistical significance, and that “once” is about to take place now, a mid-term election year. First, thanks to Mark Hulbert of MarketWatch and the Hulbert Financial Digest for publishing this research, since you’d have to be a finance aficionado to be reading finance journals to find this.

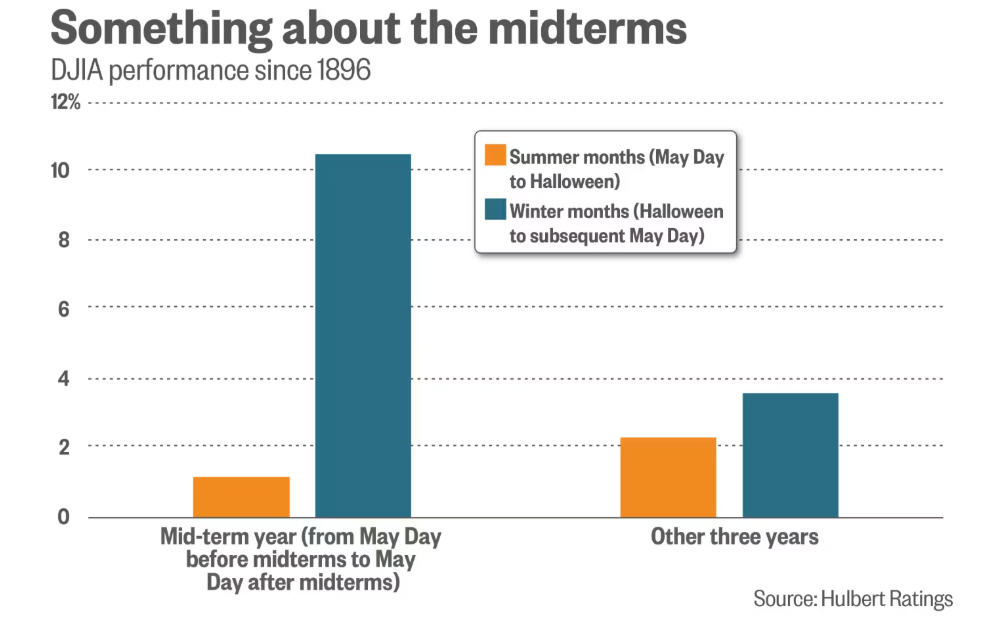

As Hulbert noted in his recent post, credit for discovering this anomaly of the Best Six Month’s Indicator dependence on the U.S. midterm elections goes to Terry Marsh, an emeritus finance professor at UC Berkeley, and Kam Fong Chan, a professor of finance at the University of Western Australia. See the table below that Hulbert produced.

What the finance professors found is that pretty much the entire edge of the best six months strategy was only statistically relevant during mid-term election years. The stock market performs on average more than 9% better in the six months after the November midterms than in the six months before. In the other three years of the cycle, though, this edge is only 1.3%, which is pretty meaningless.

We do not employ seasonal factors into any of our trading models (although we did many years ago), but if there is a year to GO AWAY IN MAY, this appears to be the year, and the time, especially with the recent straight up rally of the last few weeks, with stocks seemingly anticipating good news on the war front. My best guess from here is that most of that good news is now in the market.

A Quick Note On QCDs (Qualified Charitable Distributions)

Many of you are aware that if you are 70 1/2 or older, you’re eligible to transfer directly to charities of your choice up to $111,000 in 2026, satisfying Required Minimum Distribution (RMD) rules without increasing taxable income. This can be confusing, because today, you do not need to start taking RMD payouts until you’re 73, but when the wonderful IRS (ha) updated the laws, they failed to change the age for QCD payouts. Meaning, if you’re 70 1/2 today but not 73, you can make QCD payouts even though you’re not required to take money out of an IRA yet.

Just bear in mind that you don’t get to eat your cake and keep it too here. Meaning, if you process QCDs for example for $40,000, it will be entered on your tax return as a distribution from your IRA, but the distribution is not counted as taxable income. Importantly, you DO NOT get a deduction for making a charitable contribution. That would be double dipping. If your CPA is reporting the IRA payouts as withdrawals and then separately deducts the charitable gift, you are risking increasing your AGI (adjusted gross income) and causing all kinds of problems. That should not be happening. Thanks to MH, our former office manager, for pointing this out.

Some Brief Thoughts On AI

I’ve heard an axiom for employers who are adding staff that goes like this—hire slow, and fire fast. For me, I’m going to adapt that to the adoption of AI to any and everything—proceed cautiously, and be open-minded, but cynical. There’s a ton being written on the subject, but the article that resonated the most for me was authored by Sophie Bakalar, titled “Losing Your Mind Is Worse Than Falling Behind.” I really encourage you to read it, and absorb it.

A couple of points Bakalar makes are as follows. “In the frenzy to hack your way to success before the ‘social singularity,’ you might be destroying the skills that will actually matter in a post-AGI world; judgment, strategy, and the ability to recognize when something is off.” Microsoft surveyed 319 knowledge workers and came back with the following. “A key irony of automation is that by mechanizing routine tasks. . .you deprive the user of the routine opportunities to practice their judgment and strengthen the cognitive musculature, leaving them atrophied.”

I worry that we’ll be raising millions of young men and women who have little ability to think for themselves, because AI will just provide the answers, even though they don’t have the knowledge to understand if those answers are even accurate. Just a week ago, a dear client sent over an AI-generated financial planning document for us to review and give thoughts. I’ve glanced at it, but because of a very crammed schedule currently, haven’t had time to dive into it. At first glance, it appears quite impressive, with pages and pages of analysis. I might call this maximum data. And what is going on in some respects is what has transpired in baseball the past 10 years or so, as statistical analysis of game management decisions, the probability of scoring more runs by hitting home runs rather than singles and the effectiveness of starting pitchers as they begin to go through a lineup for the third time has overshadowed the actual judgment of scouts and managers as to what is actually happening with a player.

Bottom line, the following will always be the case, and is so spot on, from Pastor Charles Swindoll. “Machines can’t hug you when you’re grieving. Machines don’t care when you need a sounding board. Machines never affirm you when you are low or confront you when you are wrong. When you need reassurance and hope and strength to go on, you cannot replace the essential presence of another human being.” And just to reassure you, this update/newsletter is being written by me, Bob Kargenian, with my own thoughts, and has not been created by Claude, Chat GPT, Anthropic or Grok. And it never will be. You have to know what AI is good for, and importantly, you have to know enough about the subject matter to catch errors. That’s my two cents, even if the government is about to stop producing pennies.

TABR Portfolio Update

At this writing, two of our five stock market risk models are positive, so we’ve had 40% tactical stock exposure since April 1. Unless there’s a decline of about 2% in the next two trading days, another of our models will almost certainly flip back to positive next Monday, at which exposure would be increased to 60%. This is the nature of risk management. It’s been quite comforting to be defensively positioned in March, just following our process, but it’s not as much fun when the market goes straight up right back to where it was, and one is under-invested. It is all part of providing a smoother ride, and making sure there is not a significant loss of capital.

The decline into March 30 was less than -10% in the S&P 500 Index. There may be another one, or worse, later in the year. Also, our high yield bond risk model went negative on March 16, but it too is very close to going back to a positive mode, and that may be the case next Monday. This can be frustrating, but is part of the process of being mostly a trend follower. The discipline we use allows us to think clearly rather than be forced by circumstances into a decision. The following is only a guess, so take this for what it’s worth. Given the inflationary forces of rising energy prices and the combination of a mid-term election year, I think the next six months will continue to be quite choppy, with very little upside from current levels. Let’s revisit that thought in November.

Material Of A Less Serious Nature

An American tourist in London is in desperate need of a toilet. After five minutes of unsuccessful searching, he enters a dark alley. Just as he is unzipping his pants, he feels a tap on his shoulder. The American turns around to face a London policeman. “Sir, it’s forbidden to urinate in public places,” says the cop. The tourist apologizes, explaining his futile search for a toilet.

“I’ll help you,” says the policeman. “Follow me.” He heads the tourist farther down the dark alley. After a few twists and turns, the policeman unlatches and opens a small door in the wall. The American enters to find a beautiful garden, fountains, bushes and trees.

“Have at it lad,” says the officer.

As the tourist relieves himself he asks, “Is this what they call English courtesy?”

“No,” replies the policeman. “We call this the French Embassy.”

If you’re burned out on gas prices, the war, U.S. politics or any other polarizing subjects, do what I do. Embrace the NHL playoffs coming up, and maybe even the NBA playoffs. The local Anaheim Ducks will have their first home playoff games in 8 years next week and even my Portland Trail Blazers got me excited last night with a thrilling comeback to earn the # 7 seed. But if you really want to know my schedule the next 3 weeks, or possibly as long as two months, just see if my Dallas Stars are playing. This time of year, I adopt their old theme song. Nothing Else Matters. Trust me, it beats doing or paying taxes!

As always, thank you for the trust and confidence you place in all of us at TABR.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflects the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.