Solar—Yes or No, and Musings on Universal Life Insurance

Though my intentions have been to get our quarterly newsletter onto a more regular early February, May, August and November publishing schedule, I am still behind on that objective. Nevertheless, here is the first of four that we will get done this year.

As promised, we have an update on our personal experience with a home rooftop solar installation, along with some comments on universal life insurance policies, a product that many of our clients have and that we also have personal experience with. Plus, a brief note regarding online savings banks. And, there are the usual details on TABR’s various portfolios for the prior year, where we perhaps provide TOO much information, but with our usual candor along with shorter and longer term perspectives.

Please note that within the next week, you’ll be receiving an email from us with a link to take our short client survey. We’re always looking to improve upon what we do for clients in a variety of areas, so we’d appreciate your time and feedback.

Should You Install Solar? The Latest

It’s now been just over one year since we had solar panels installed on our home rooftop in Yorba Linda. Much has taken place in the last year from a regulatory standpoint in regards to electrical rates being charged by the various utilities, and what has been approved by the Public Utility Commission (PUC). This is not just for the state of California. The state of Nevada recently voted to sunset the state’s net metering program, which compensates customers who remit excess solar power generated from their rooftop panels at the retail rate of power.

This was a drastic cut for retail solar owners, and within weeks, Solar City, the largest installer in the nation, announced that it will cease operations in Nevada. Let me tell you my bottom line, based on all the facts which have changed since I began to investigate whether or not solar was a good deal. Then, I will provide details on the upcoming rate changes for those that want to pore over the rationale.

Though leasing a system, where no upfront funds are required, reportedly accounts for almost 75% of new solar installations, this method no longer makes sense, in my opinion. If your electrical bill does not average at least $400 a month, and you’re not buying the system outright, don’t even bother with solar. That’s not to mention you should be intending to stay in your home for a long time, because the typical contract is for 20 years, and you are on the hook for it, even if you want to move and sell your home. If you’ve signed a contract that has turned out to be a crappy deal, it is going to make it harder to sell your home, because a prospective buyer is not going to want your deal.

First, the entire industry would not exist without government tax credits. Those credits were narrowly approved by Congress in December for another five years, or the outlook would be even bleaker than I am suggesting. But, the sales premise from every company was that electricity rates were going to just continue to increase over time, and that by going solar, you could provide the electricity you need at lower rates, and even provide the environment with cleaner energy.

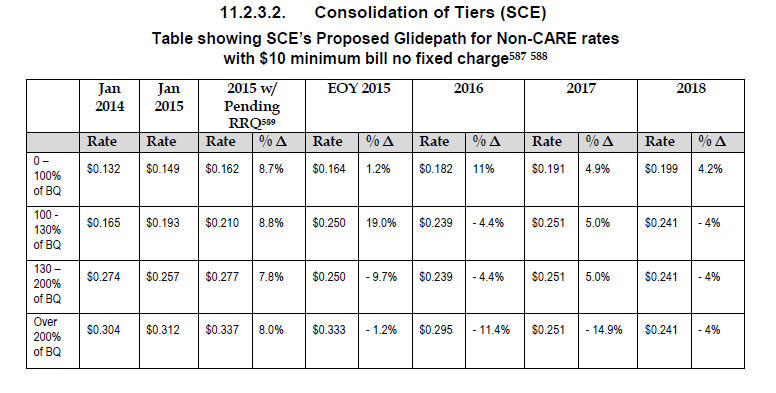

But, the utilities have thrown a wrench into the long term prospects of solar by getting the PUC to approve a rate structure that collapses the tiers from four tiers to two tiers. Importantly, as the table below shows, the lowest tier, which was at 0.149 cents/kwh in January 2015, will rise 33% by 2018, while the top tier will fall from 0.312 cents/kwh to 0.241, a decrease of almost 23%. So, the consumers who use the least amount of power (and don’t need solar) will be seeing an increase in their costs, while the consumers who use the most electricity will be seeing their rates go down, making solar less attractive (again–unless you buy your system, get the tax credits and stay long term).

The table above is excerpted from the California PUC Decision on Residential Rate Reform, and the Proposed Decision dated July 3, 2015, which affects customers of Southern California Edison, San Diego Gas & Electric and Pacific Gas & Electric. The table shown is relevant only to SCE customers. Many thanks to our client who sent the whole document to us, along with excellent insight.

In my own case, we’ve now had monthly bills for 12 months, and entered into a contract where we have locked in a constant rate of 0.19 cents/kwh for 20 years. Going in, our average bill was running $500 per month, and our monthly lease payment is $297, so we were expecting to save $200 per month. Supposedly, if our system did not produce a minimum amount of power during the year, in the range of 17,000 to 19,000 kwh, we are supposed to get reimbursed by the company for the difference (this is in the contract).

But, remember, there is the net metering rule, and when all was said and done, we still had to pay SCE about $480 in net metering charges for the 12 months. So, our savings were reduced to about $1920, and I’m still in the process of interacting with the company we hired, Sun Power, to see if they are going to send us a refund. Their monitoring system shows that they produced 17,672 kwh during the 12 months, yet my bill from SCE shows net generation of 10,948 kwh.

The California PUC narrowly rejected a request to change the net metering rules (unlike Nevada), but that doesn’t mean the utilities won’t keep trying. The utility companies feel that non-solar utility customers are subsidizing solar companies. The solar companies are complaining that the government encourages consumers to go solar by providing incentives, and is now retroactively taking those away.

I’m not sure where it all will end, but this is for sure. For more and more people, solar is not going to be beneficial, which may make the marginal players in the industry eventually fail. Stick with a company like Solar City, who appears they will be around. And, negotiate. If you can lock in rates that are low enough, given a future top tier at 0.241 cents, maybe it can be worth it in certain cases. Just make sure to do your math.

Stung by ‘Universal Life’

That was the headline in a Wall Street Journal report inside the August 10, 2015 edition. The gist of the article was that in the 1980s, over 25% of individual life insurance sales were of this type of policy known as universal life. Unlike term insurance, both universal life and whole life policies are permanent, and build up cash value over time, as a result of on-going premium payments.

Without getting into too much detail, the main difference between universal life and whole life is that the former offers flexible premium payments, which can be increased or decreased over time. When interest rates are higher, universal life policy holders can pay lower premiums, but if rates are lower, they will pay higher premiums. In contrast, whole life policies offer fixed level premiums that will not change.

If you recall, in the 1980’s interest rates were in the low teens, so when many of these policies were sold, the agents selling them illustrated the future as if 12% interest rates were going to go on forever. This led policy holders to believe that they could get away with paying low premiums and still keep their policies. But that is not what has happened. As you know, interest rates have been declining for nearly 30 years, and are at some of the lowest levels in U.S. history. As a result, many of these policies are in danger of perishing, and if our experience with several clients is any indication, it is likely that many of the policy owners are not aware this is happening.

By the way, this problem is not just with policies issued in the 1980s. Below, we’re going to show some detail of an in-force policy illustration for a policy that was issued in November of 1999. This real example happens to be of a variable universal life policy (which has its own issues, and an area we’ve had personal experience with). The premise, however, is the same. If the policy owner (that is normally you or me) doesn’t put enough money into the policy in the way of premiums, and/or the policy itself does not earn enough from investment returns, especially in regards to the projections that the policy was purchased on in the first place, then the policy is going to terminate much sooner than one realizes, unless something is changed.

An insurance company has to spread its risk over time, and over many thousands (or millions) of policyholders. With permanent insurance, even where one is paying level premiums, you end up paying more than the cost of insurance when younger, so that you can accumulate enough cash value to pay for the much greater cost of insurance when we are older. Initially, how much one pays in premiums is determined by the health ratings on the insured (for instance, common jargon is super-preferred, preferred, standard, and so on), one’s age, and the projections for what the insurance company is crediting on their policies (whole life) or what one thinks is reasonable to earn in the way of returns over time (variable life).

Ultimately, one would want to pay the least in premium for the most amount of insurance. But that is not easy to get to, because in this product area, many of the policies can be incredibly complex and opaque, and are not always sold with the best interests of the client in mind, but rather the best interests of the insurance agent. I should point out, especially in light of last week’s Department of Labor ruling on retirement plan advice, that most insurance professionals are paid by commissions, and are typically not subject to a fiduciary standard, as we and other RIAs (registered investment advisers) are. A fiduciary is to put the interest of the clients first.

| Age | Premium Outlay | Admin Charges | Cost of Insurance | Total Charges | Cash Surrender Value |

| 76 | $1200 | -66 | -1019 | -1248 | 7774 |

| 77 | $1200 | -66 | -1111 | -1342 | 7959 |

| 78 | $1200 | -66 | -1213 | -1446 | 8047 |

| 79 | $1200 | -66 | -1320 | -1553 | 8028 |

| 80 | $1200 | -66 | -1454 | -1687 | 7871 |

| 81 | 0 | -66 | -1624 | -1764 | 6402 |

| 82 | 0 | -66 | -1830 | -1954 | 4676 |

| 83 | 0 | -66 | -2069 | -2173 | 2652 |

| 84 | 0 | -66 | -2688 | -2742 | 277 |

To illustrate the problem I’m referring to above, I’ve shown partial data above on an illustration we recently received (I’ve had to exclude some data due to space limitations). This policy has a $70,000 death benefit, and was taken out by a 53-year-old female, who today is 69 years old. Since this is a variable life policy, I asked that future investment returns be assumed at a 4% net rate (net of expenses). At present, the policy owner is only making premium payments of $888 annually. That, of course, is the first problem.

That’s not nearly enough to cover the expenses of the policy, if one lives until around age 90. So, I first asked the insurance company, Pacific Life in this case, to assume premium payments of $1200 annually, until age 80. That initially gave us enough information, as you can see in the above table, that the policy would lapse at age 85.

Though not shown, I also asked for an illustration where we increased the annual premiums to $3000, and also stopped them at age 80. This showed the policy lasting until age 97.

Now we have enough information to discuss with the client how important this policy is in their overall planning work, which also will include the affordability of the increased premium on their budget, and an objective discussion about their health, and their likely longevity. In this case, $1200 premiums are not likely enough, since most people have a good chance of living beyond age 84, yet $3000 may be too much.

Another option that can be suggested, depending on the goals of the client, is reducing the amount of the death benefit, which will in turn reduce the premiums necessary to maintain the contract for the desired amount of time.

In our experience in evaluating dozens of these types of policies, this type of analysis is rarely done by the insurance agent who sold the policy. Not all ignore this analysis, but certainly many do. I can tell you there are many people who have similar issues as the above, and some of them are our clients. This is just another example of the types of things we discover when we are looking at every aspect of a client’s financial life.

We realize that life insurance is a distasteful topic for many. But, its an important element for many individuals and families. If you were not aware that we could help in this area, please use this as a reminder that we can. In addition, I’ve had personal experience with term, universal life and variable universal life, and please know that in our role as an RIA and fiduciary, we receive no commissions from anyone to implement recommendations. The management fee we charge on assets under management isn’t just for investments. It covers a whole host of areas that we provide advice and guidance on. We’re simply looking for the best fit for clients in their situations.

Online Savings Banks

The Federal Reserve Board has been pursuing a zero interest rate policy for the better part of 8 years now. And though the Fed raised interest rates in December by 0.25%, there is no guarantee that rates are going to rise significantly any time soon. As a result, yields on savings accounts at the major banks such as Bank of America, Wells Fargo and Chase, along with most money market funds from brokerage firms, whether they be Schwab, Fidelity or TD Ameritrade, have been at 0.10% or less for quite some time. CD rates, of course, have not been much better, though yields at certain credit unions that clients work with have been more competitive.

For those of you who have significant cash (that could be $20,000, or $1 million) sitting in a bank earning very little, there is an alternative, as long as one is comfortable being totally online with this portion of your money. The first virtual bank was created in 1995, but they really haven’t caught on to be more widely used until the last few years. And, they’re not for everyone. If you have a lot of complex transactions, or need to talk with someone frequently, forget it. But, if you simply want to earn on your cash instead of 0.10%, and still have it liquid and FDIC insured, where you can link it to your main bank and make up to six withdrawals in a month, you may want to take a look.

In our experience with clients, the four banks that most are using include Ally Bank (the former General Motors Acceptance Corp), Capital One 360, Synchrony Bank and American Express Personal Savings. Below, I’ve summarized their current rates on savings and short term CDs.

| Online Bank | Yield on Savings | 1 yr CD | 2 yr CD |

| Ally Bank | 1.00% | 1.05% | 1.30% |

| Capital One 360 | 1.00% | 0.75% | 1.10% |

| Synchrony Bank | 1.05% | 1.25% | 1.45% |

| American Express | 0.90% | 0.55% | 1.00% |

It is very possible that interest rates may remain low for an extended time (think Japan). I sincerely hope not, as I believe the unintended consequences may cripple the U.S. pension system, which are relying on significantly higher returns to meet their liabilities. So, it makes sense to maximize things where we can, especially when there is no risk. If you’ve had a good or bad experience with any of the above, or if there is option in this area that we’ve missed, please let us know so we can compile feedback.

2015 Performance—All of it

None of us can control investment outcomes, but we can control our process, so that what is what we are always focusing on (and of course, trying to make it better, where possible). We’re not looking to maximize returns per se, but rather to meet client goals with the lowest amount of risk. In investing, there are tradeoffs, so comparing oneself to a benchmark isn’t always the end all, unless the comparisons are apples to apples. Nevertheless, we do use benchmarks to give some overall context.

The rest of the section is filled with a myriad of details. We find it useful to look back and contemplate what we’re doing. For those of you who only care about the bottom line, here is the brief summary. Neither tactical nor passive strategies produced gains last year, and the more you were diversified, it’s likely the worse you did. Large company stocks were about the only area that held up in 2015, as they are typically the last segment of the stock market to turn down. Exposure to mid-caps, small stocks and international/foreign was a substantial drag, and the high yield corporate bond market had its worst calendar year in some time. Stocks peaked in May, and spent the remainder of the year on the defensive. For those of you into the details, read on. We break things down into four categories—real estate, bonds, alternative and stocks.

Real Estate

| Dow Jones Real Estate Index (IYR) | 1.61% |

| Cohen & Steers Real Estate Fund | 7.35 |

Our trend following model for this sector entered the year on a BUY signal that went back to February of 2014. A sell finally came in June, followed by two buys in November, one of which lasted all of two weeks, and that we ended up hedging with an inverse short position in the Pro Shares Short Real Estate Fund, since we had taken a position in the Cohen & Steers fund noted above. As you can see, buying and holding the index (IYR), resulted in a small gain from the year, including reinvested dividends, while we estimate the trades with our model resulted in a -5.13% loss. Allocations within portfolios range from about 3% in Conservative accounts to 7% in Aggressive accounts.

Bond Funds

| PIMCO Income Fund | 2.64% | Sierra Strategic Income Fund | -0.76% |

| PIMCO Short Term Fund | 1.37 | Mainstay High Yield | -1.68 |

| PIMCO GNMA Fund | 1.33 | PIMCO High Yield | -1.85 |

| Prudential Short TermCorpBond | 1.07 | Lord Abbett High Yield | -2.02 |

| Blackrock Low Duration | 0.92 | Prudential High Yield | -2.59 |

| Lord Abbett Short Duration | 0.86 | Principal High Yield | -2.92 |

| Hartford Short Duration | 0.76 | MFS High Income | -3.82 |

| PIMCO Total Return | 0.73 | Blackrock High Yield | -3.96 |

| Fidelity Short Term Bond | 0.67 | Alliance Bernstein High Yield | -3.97 |

| JP Morgan Short Duration | 0.52 | Hartford High Yield | -4.34 |

| Loomis Sayles Limited Term | 0.47 | JP Morgan High Yield | -4.54 |

| MFS Limited Maturity | 0.28 | Putnam High Yield | -5.05 |

| Guggenheim 2024 CorpBond ETF | -0.15 | Loomis Sayles Bond | -6.86 |

As a refresher, let me outline our bond strategies, and how they are broken down. We allocate about 65% of the bond allocation to our high yield corporate bond risk model, where when on a BUY signal about 90% of this capital is devoted to a fund in this sector, with the remainder staying in a shorter duration bond fund. This is reversed when our model moves to a SELL signal. Presently, we are using about 11 different high yield funds in client portfolios.

You can see from the above that this sector of the bond market, which has the most risk on a buy and hold basis, had a very difficult year. The above numbers represent the full year return of each fund, not the results of our trading. Our risk model generated two trades during the year—a buy in February and a sell in July, then a buy in late October and a quick sell just 3 weeks later. Based on the Lipper High Yield Fund Index, we estimate a gain of 0.75% on the first trade and a loss of -1.93% on the second. So, we did much better than the Index, which was down nearly -5% for the year.

Until the third quarter, in the past, we have devoted about 50% of the high yield bond money to the Loomis Sayles Bond Fund, an excellent multi-sector fund with a very good long term record. It was the worst fund on the list last year. We became uncomfortable with the fund during the second quarter when we learned they were making fairly large bets on foreign currencies and foreign bonds. We wanted to make sure that we were owning a fairly pure sample of corporate high yield U.S. taxable bonds, so we made the decision to eliminate the fund from our portfolios. This is why you are seeing that we are now using many more high yield funds, to replace the position in Loomis Sayles.

The other 35% of our bond allocation is in more conservative areas, which now include about 14% positions in PIMCO Income Fund and the 2024 Guggenheim Defined Maturity Corporate Bond Fund along with a 7% position in Sierra Strategic Income. The latter two positions stay put. Sierra has its own risk models which we are pretty familiar with, and we know they will go heavily in cash or short term bond funds, should there be a significant rise in interest rates. We added the Guggenheim fund late in the year. It is of investment grade quality and all the bonds mature in 2024, and at our purchase price, we were able to lock in a yield to worst of about 3.65%, net of the funds expenses, which we view as excellent in this environment.

Finally, we’ve used a risk model for nearly 8 years now on the PIMCO GNMA Fund, one of the safest and more consistent funds in its category. We may use this fund again in the future, but late in the year, we replaced it with the PIMCO Income Fund, also very strong in its category. We have a similar risk model for this fund. Our motive is that in this environment, during the next five years, we think we will be able to earn a slightly higher total return with PIMCO Income, without any commensurate increase in risk.

Overall, TABR’s Bond account lost -3.07% for the year, while the Vanguard Total Bond Index Fund gained 0.30%. This reflects the more aggressive stance we take in bonds in the high yield area, which has rewarded us in the past with greater overall returns, and which we expect will continue to reward us in the future.

Alternative Funds

| Leuthold Core Investment Fund | -0.98% |

| PIMCO All Asset All Authority | -12.06* |

I’m not sure what to call this area anymore, because we’ve eliminated all of these types of funds going back to late 2014. Those included Hussman Strategic Growth and Marketfield, which continued their poor performance in 2015, thankfully without us as shareholders. *We entered the year with a small position of about 2% of portfolios in the PIMCO Fund noted above, but sold it all by early July, where we realized a small loss of -1.84% for the six plus months. We’re quite thankful, as the fund went on to lose another 10% during the second half of the year.

Leuthold continues to be a small core holding of between 2% and 4%, but we don’t consider it an alternative fund at all. It is a tactical fund that can own as much as 70% equities, but as little as 30%, based on the readings of their Major Trend Model. They have a very transparent process with a good long term record, but we’ll never again commit significant money to others. We’re going to live with our own work, for better or worse. We cannot erase the mistake of holding too much of our portfolios in this area in 2012, 2013 and 2014. We can only learn from it and never make it again.

Stock Funds—-Core Tactical Holdings

| Hotchkis & Wiley Value Opportunity | -0.02% | PIMCO Fundamental Index Plus AR | -7.07% |

| Touchstone Sands Capital Growth | -3.58 | Hodges Small Cap | -8.75 |

| Ariel Fund | -4.10 | Hotchkis & Wiley Mid Cap Value | -12.75 |

We’ve been using a relative strength methodology to select five core equity funds since 2008, with slightly above average results when compared to a benchmark we use, which is composed of a 75% weight in the Vanguard Total Stock Index Fund and a 25% weight in Vanguard Total International Stock Index. This blended benchmark lost -0.87% last year, but the average of the five funds (Ariel was a sixth, but was owned in a small minority of accounts) was down -6.43%. So, yes, “active” management even with our methodology had a rough year.

As noted in our last newsletter in mid-December, we’ve eliminated the active funds and replaced them with broad-based index exchange traded funds (ETFs), where we use a similar technical relative strength score to rank them against each other on a monthly basis. So, the core positions we own are passive in the regard that they are indexes, but we are dynamic in terms of what we own. For instance, no international indexes are near the top of our rankings at all. At present, the four ETFs we own are the NASDAQ 100 (QQQ), the Equal Weight S&P 500 (RSP), Small Cap Growth (IJT) and Mid Cap Value (IJJ).

TABR Fully Invested Passive Account

| PIMCO Real Estate Real Return | 3.85% | Alliance Bernstein Discovery Value | -5.89% |

| PIMCO Stocks Plus Int’l US$Hedged | 0.71 | PIMCO Fundamental Index Plus AR | -7.07 |

| Fidelity Capital & Income | -0.92 | PIMCO Stocks Plus Small Cap | -7.08 |

| Loomis Sayles Core Plus Bond | -4.20 | Aston Fairpointe Midcap Fund | -10.37 |

| John Hancock Disciplined Value | -5.20 |

Though we’ve been running a version of a passive mostly indexed based portfolio since 2007, we didn’t roll this strategy out to clients until late 2013. It’s designed for those who may want to be more aggressive with a portion of their assets, and follows the more traditional buy and hold, fully invested approach which has become quite common in our industry. A full research report on this, including research dating back to 1972 is available in the September 2013 TABR quarterly newsletter.

Our initial twist on this concept was to take the common allocation of 60% stocks and 40% bonds and use actively managed funds, rather than index funds. Given the purpose of this approach, we’ve come to the conclusion it’s better to stick with the index funds, so in early January 2016, we re-balanced nearly all of these accounts to that process. There are a handful of accounts remaining using actively managed funds as we are evaluating the costs of rebalancing in smaller portfolios under $100,000. For the full year, the fully invested Passive Account was down -4.99%.

TABR Dividend Stock Account

Having initiated this strategy in the fall of 2014, this was the first full calendar year we’ve completed with this equity process, which owns high yielding stocks in the S&P 500, combined with a fundamental value screen. Overlayed with the stock selection are a few of our stock market risk models, where we can reduce exposure to no less than 50% invested.

As it turned out, this took place in June and July, so the portfolio was about 50% invested from early July to the end of the year. During that time period (from July 9 to year-end), the stocks in the portfolio fell -7.40% while the Vanguard S&P 500 Index Fund (VFINX) gained 0.57%. For the year, overall total returns were -9.10% versus a 1.25% gain for VFINX. The portfolio during the year had decent exposure to utilities and energy stocks, both sectors which sport decent yields, but also were among the worst performers for the year.

This doesn’t invalidate the strategy. It’s one year. Readers may recall our original research going back to 1973. There have been a couple of periods in history where there have been back-to-back double-digit losses, yet, over time, the process has proven in the past to add considerable value along with above average income.

Speaking of income, the account produced a 3.68% yield on our original capital, and started 2016 with a yield of 4.14% on the stock portfolio. We’ve noted to a number of clients who have asked—we don’t have any particular conviction about any one of the stocks, since we are following a formula, but we do have high conviction in the process. Our plan is to add capital when there is significant weakness in stocks, which still has not taken place. At some point in the next 12 to 24 months, there should be a better opportunity than what took place in February of this year. The key is having the discipline to act when things look bleak. Most investors would rather add money when things look good, such as now, but the price data will show that stocks in general are more expensive now than they were just 8 weeks ago.

TABR Strategies for 2015

Though our stock market risk models handled the third quarter decline quite well, equity fund selection detracted from the comparison versus indexes (see above). Going forward, we believe this will be less of an issue, with our move to broad-based ETFs, coupled with our relative strength work. And for the first time in a long time, our overall bond strategies were a drag.

Below is the performance, net of management fees, of TABR’s five different portfolios at present. These represent a majority of the strategies we are using in client accounts, but not all. The differences are mainly attributed to risk (example—moderate allocation versus conservative allocation or aggressive) and account size. The numbers are for the one year ending December 31, 2015 as well as the cycle from September 2007 to December 31, 2015.

| Type of Account/Strategy | YTD | Benchmark | 09/07 to 12/15^ | MaxDD |

| TABR Tactical Moderate | -3.56% | -0.40%* | + 0.33% | -25.06% |

| TABR Tactical Conservative | -3.81 | -0.17** | n/a | |

| TABR Tactical Bond | -3.07 | +0.30*** | +4.83 | -19.73 |

| TABR Dividend Stock | -9.10 | +1.25**** | n/a | |

| TABR Fully Invested PBA | -4.99 | – 0.19 | n/a | |

| Vanguard Total Stock | 0.29 | +6.0 | -55.38 | |

| Vanguard Total IntlStock | –4.37 | – 1.40 | -60.60 | |

| Vanguard Total Bond | +0.30 | +4.30 | -5.36 |

*consists of 40% Vanguard Total Stock Index, 15% Vanguard Total International Stock Index and 45% Vanguard Total Bond Index

**consists of 30% Vanguard Total Stock Index, 10% Vanguard Total International Stock Index and 60% Vanguard Total Bond Index

***Vanguard Total Bond Index

****Vanguard S&P 500 Index Fund from 12/31/14 to 12/31/2015

^ denotes annualized returns and actual period is 9/30/2007 to 12/31/2015

MaxDD stands for maximum drawdown, the worst loss from peak to trough in the period noted

Returns shown are net of management fees, and include reinvested dividends

In Closing

Next letter, we intend to delve into the topic of Target Date Retirement Funds, also known as LifeCycle Funds, which are common investment options today in many 401 (k) and related retirement plans. Depending on the depth of that treatise, we’ll look to include some other areas, including a section we’ll call What Daddy Does, inspired by a question from our 11-year-old daughter Caroline.

Meanwhile, since peaking in early December, stock indexes (and bonds for that matter) have been on a roller coaster, with sharp declines into mid-February, followed by an equally sharp recovery thus far. Time will tell if the improvement has longer-term legs, or if this turns out to be what is called a “sucker’s rally.” Overall, at present our work is more positive than negative, but with a wary eye on valuations, which are historically expensive.

All of us at TABR are grateful for the trust and confidence you express in us daily.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov.).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services