Something’s Got To Give—-Will It Be S&P 500 3900?

Stocks staged a fairly impressive rally off of their mid-June lows, with the S&P 500 gaining over 17% in two months, and the NDX 100 (aka the QQQ) up nearly 23%.

This had given hope from the bulls that the worst was over, and perhaps inflation was peaking. But in mid-August, virtually all major indexes were turned away by their respective 200-day moving averages, and it appears that short-to-intermediate-term downtrends have reasserted themselves, with today’s inflation report suggesting that indeed, the worst is not likely over. From a technical perspective, the 3900 level on the S&P 500 is very important. Should stocks close below this key support level for more than a day or two, I would expect a full test of the June lows, with potentially much lower prices ahead.

In this monthly update, we’re going to start with markets, given their losses today of -3% plus, and go from there. There are a lot of similarities today to the 1973-74 period in markets, and we’ll touch on that, and current positioning, which is back to our Max Protect mode since September 5. I’ve also got segments on the best way to give, a sad reminder that an estate plan is essential in caring for your loved ones, and some talk on estimated taxes and what I consider to be the mirage of California’s budget surplus. Some of you may skip right to the humor section, as 2022 is a stark reminder that good times in markets don’t last forever, and why we believe risk management is essential for the vast majority of one’s investment capital. We’ll leave the Buy And Hold Forever theme to all the crypto and Game Stop enthusiasts. That’s not our game.

Portfolio Allocations—Back To Max Protect Mode

In late July and early August, some of our risk models improved, and BUY signals were generated from our high yield bond risk model, and two of our five stock market risk models. As a result, we increased exposure in those areas, with tactical stock exposure bumping up to 55%, an area we consider to be neutral. This improvement didn’t last long, as noted above. In the last two weeks, we received multiple SELL signals in both areas, and by last Monday, September 5, were back in our most defensive positioning, with the exception of a position in PIMCO Income, which may generate a SELL later this week. All of our high yield bond allocations are sitting in ultra-short bond funds, which is really important in a rising rate environment, and we currently have no tactical equity exposure. Our sector fund exposure which relies upon relative strength plus positions in two dividend-stock ETFs equals about 25%.

Since our Moderate Risk portfolios currently have a maximum equity exposure of 55%, and Conservative portfolios a max of 40%, in English, this means our net equity exposure is roughly 14% of the entire account in a Moderate portfolio, and about 10% in a Conservative portfolio.

This is a good time to once again emphasize that during periods such as these when our portfolios our heavily defensive, our portfolios are not going to behave like the markets at all. That will only happen with passive portfolios, which are fully invested at all times, and play no defense. We use those for a small portion of certain client accounts who are comfortable with this diversification, but the vast majority of the capital we manage is tactical. When there are bear market rallies such as in July when the S&P 500 gained 9% for the month, we will not keep pace with the balanced benchmark. Likewise, when markets are down such as in August with a -4% loss to the S&P 500, we will outperform significantly.

The whole key is to limit losses during significant declines, and thus far in 2022, that’s what’s happening. There will be extreme days like today, when stocks decline by -4% or more, and our portfolios will barely be down. Believe me, this allows one to think much more clearly than if you’re getting your head bashed in. At some point, stocks will bottom and head higher again, and then one feels like you’re being left out, but eventually, in a real bull market, our various models will turn bullish, and our portfolios will be aligned with the new trend. This process repeats itself over a period of years, and the key is simply following our disciplines. We can’t tell anyone how low prices are going to go, or how long this bear market is going to last. Nobody can. But when you have a process that works, you just follow it, and trust it. Down markets are not really fun for many people, except for a very small minority of traders who may make significant money shorting the market. In many ways, the key to getting through a bear market is getting comfortable with being uncomfortable. And in our view, the more one can minimize the drawdowns, the easier that is.

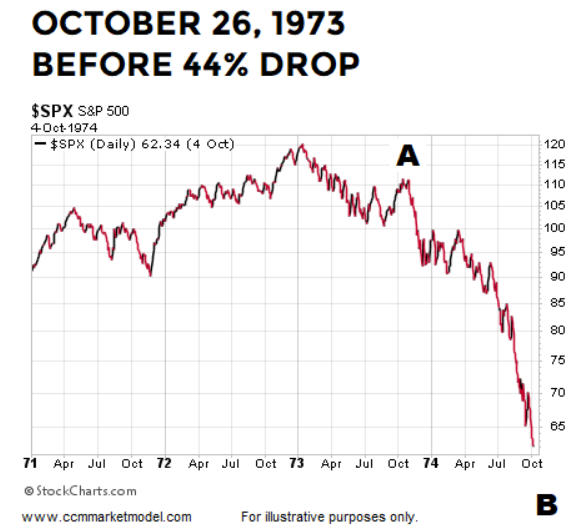

Memories of 1973-74

I will be turning 65 this November, and no worries, I’m not retiring. Remember, we have our 17-year-old daughter still at home, in her senior year at Orange Lutheran, then off to college and in all probability, graduate school to become a veterinarian. Back in 1973, I was a 16-year-old attending Tulare Union High School. I sure didn’t know what the stock market was doing then. And, I’m sure many of my age-related peers don’t remember much either, certainly not from an investment standpoint. In reality, the majority of today’s investors have never experienced a stock market that is dealing with very high inflation.

As Ned Davis Research’s Joe Kalish noted a month ago in one of the firm’s updates, this year’s bear market has many of the characteristics of the early 1970s which ultimately led the S&P 500 to decline -45% during a two-year span. Mainly, very high inflation, a doubling of oil prices (sound familiar?) due to the Arab-Israeli war in October of 1973 which also started the Arab oil embargo. In addition, monetary policy was quite similar, with an unfriendly Fed. Starting in the early part of 1973, the Fed raised the discount rate from 4.50% to its peak of 8% on April 25, 1974, where it stayed until December 9, 1974. In other words, the Fed was tightening financial conditions deep into a recession. Why? Because inflation was soaring. In June of 1972, the CPI bottomed at 2.7% and had increased to 3.7% when the Fed began their rate increases. Inflation would eventually top out at 12.3% in December of 1974, which is when the bear market ended.

–

In this cycle, inflation was basically at zero in May of 2020 thanks to Covid, but had shot up to 8.5% in March of this year when the Fed began their tightening cycle. So far, the Fed has increased the Fed Funds rate from 0-0.25% to its current level of 2.25-2.50%. With today’s median CPI coming in for August at 9.2%, the highest in the history of the database going back to 1983, it’s a virtual certainty that the Fed will bump rates next week by another 75 basis points, to the 3.00-3.25% level. As a result, the narrative is the Fed will need to raise rates higher than anticipated, and for longer. We could easily see Fed Funds at 4% by the November meeting.

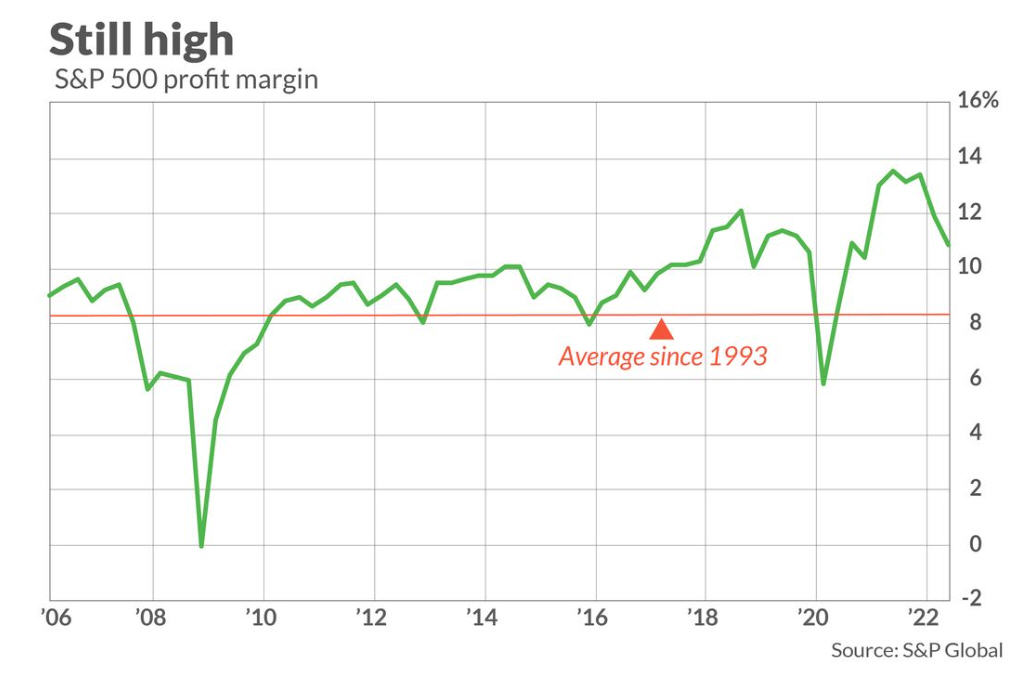

With today’s huge jump in short-term yields (over 20 basis points across the board), 6-month Treasury Bills are now priced at 3.78% and 1-year Treasuries at 3.92%. We expect the Fed Funds rate to follow to these levels, at a minimum. The higher yields go, the more pressure on stocks, and especially on growth stocks. Rising interest rates and high inflation is one of the worst combinations for the stock market, and that’s the hand we’re dealt with at the moment. All of this points to lower profit margins. Profit margins have been running at 10% or higher for a large majority of the time the past 6 years, save for the Covid interruption. A great visual is below, courtesy of S&P Global and Mark Hulbert’s Marketwatch column.

As shown above, margins have averaged just over 8% since 1993, and are currently 32% above this average. Thus far, many companies have been able to maintain revenue thanks to robust demand, but inflation is beginning to eat into profit margins. This eventually will affect net earnings, and we’re likely going to see a contraction in price/earnings multiples, coupled with a deceleration in earnings. That’s not a good combination for stocks.

Git R Done Estate Planning

Remember Larry The Cable Guy? I thought of his slogan when reading about the sad tale of actress Anne Heche, who recently was killed, as a result of injuries suffered during a car crash. Heche, 53, left behind a 20-year-old son, Homer, and his 13-year-old younger brother, Atlas. That’s terrible, but so was the news that apparently, Heche died without a will or estate plan, leaving her kids with a mess. A guardian needs to be appointed for the youngest son, as well as an appropriate person to sort out all the financial affairs. Unfortunately, it’s not uncommon to see high profile people neglect this area. But, lacking an estate plan is not uncommon amongst “everyday” people either. It’s estimated that 40% of the adult population has no estate plan in place.

One of the most important things that parents with children and single persons can do is to leave an organized legacy behind. And unless one has a direct connection to God, I’m pretty comfortable saying you probably don’t know when you’re going to die. If you’re part of the 40% noted above, don’t procrastinate any longer. You know who you are. Git R Done.

The Best Way To Give

Many of our clients give generously to institutions they care about, and are passionate about. My wife and I are so grateful to do what we are able to do in this area. Common causes that people love to support include colleges and universities, theatre and arts, churches and ministries, and honestly, the list is really up to your imagination. Many of you may be aware of the tax law that permits one to donate all or a portion of their IRA required minimum distributions once they reach the age of 72. This is a very effective process.

For instance, one of our clients has a required distribution of about $30,000 annually. Normally, that income would be taxable to them. Instead of donating out of their after-tax assets, though, they have had us cut checks to various charities of their choice to fulfill their annual requirement. One can contribute up to $100,000 annually in this manner and not pay tax on the distribution. This is known as a qualified charitable distribution (QCD).

Giving away IRA assets is a better planning decision than giving away after-tax assets. Why? Because your heirs will pay tax on inherited IRA accounts. But, they don’t pay tax on inherited after-tax assets. A few years ago, my wife and I decided to add several programs that we support to our estate plan. The payouts would become effective when we each die. Recently, though, due to some reading I was doing, it dawned on me. This was a really ineffective manner to give (actually, it’s stupid!). We were going to have this money come out of our Trust. This is not good. This would cost our children a significant amount of money in taxes. How? Because they would inherit our IRA accounts, and pay taxes upon taking money out of our IRA’s after we’re both gone. What’s the smarter way to accomplish this? Simply name the various entities as beneficiaries on our IRA accounts, and stipulate percentages that go to them.

In that manner, the entities still get the donation, and they don’t pay taxes on the money coming out of an IRA, because they are non-profit. Our children will inherit assets from our Trust, and they will not pay taxes on that money (unless my Power Ball ticket comes in and all of a sudden, we have more than $25 million in the estate!). Yes, there is a certain weakness in this plan, in that one cannot designate a dollar amount when specifying a beneficiary of an IRA. Plus, the value of the IRA changes annually, depending on markets and withdrawals. But, it is manageable. All we have to do is compute the amount we want to give to each entity, divide that into the value of the IRA, and put that approximate percentage down on the beneficiary form from Fidelity. Perhaps every few years, we update it. A few pieces of paper updated every couple of years is absolutely worth it to our kids, to save tens of thousands of dollars in tax.

As we speak, we are in the process of having our estate attorney eliminate the provisions we had in place in our Trust to give to various entities. Once that amendment to our Trust is signed and notarized, we’ll then file updated beneficiary forms to reflect our wishes within our respective IRA accounts. If you have plans in your estate plan to donate money after your death, and currently those plans involve taking the funds from your non-retirement funds (after tax), I strongly encourage you to re-think that strategy if you also have large IRA accounts that could accomplish the same thing. There’s no use in giving the government money that instead could go to your loved ones, all with a little proper planning.

The California Tax Budget Surplus Mirage

Several clients have called in recent weeks in advance of this week’s quarterly estimated tax payment deadline. They all wanted to get a handle on their numbers. My payment is going to the IRS tomorrow. As I’ve been answering these various queries, I thought it would be of interest to share what I see, and what we’re likely going to be hearing in the early part of 2023.

First, almost all of us with decent-sized portfolios paid a lot of extra tax on their 2021 returns because most people had strong years in their accounts. Capital gains. This can cause one to then have to pay estimates the following year, because the IRS assumes if you earned X last year, you’re probably going to earn X this year. Except that’s not the case. Nobody knows how markets will do. Well, with 3 months to go, I can tell you how markets are doing. Almost everyone is losing money, and some people are losing a lot of money. Oh, you had a $75,000 capital gain last year. Good. This year, you’ll be claiming a ($3000) loss, and carrying forward the rest. As a result, taxable income all over the nation, no matter the state one lives in, is likely going to go down, and in all probability, in a big way.

It was reported several months ago that California has a record $97 billion surplus. If you know California’s politicians, they’ll find a way to spend most of that. I’ve not yet found any credible reports that the State intends to pay down debt, or set aside say $25 billion in reserve. Something prudent. Why is this relevant? Because in California, from a 2019 study, there are 96,000 households who earned over $1 million that year, and they accounted for $35 billion of the $90 billion in taxes paid, or 39% of all taxes paid. They are the top 1/2 of 1% of earners. My guess is with markets down, they will have almost no gains to report.

So, here’s my bet. Sometime in the first quarter of 2023, we’re going to be reading about California’s record budget DEFICIT, and there will be calls to raise taxes so they can pay for education and a bullet train to nowhere that nobody needs or asked for. You read it here first.

Welcome Jamie Klein!

Today marks the eighth day for Jamie at TABR, who is in the midst of assuming the role of our Office Administrator and Senior Client Services Specialist, taking over for Mary Hernandez. Mary has been pinch-hitting on a remote basis since late May, and along with Sylvia, is helping to get Jamie acclimated in a number of areas.

Jamie comes to us after spending the last 13 years serving as Operations Manager for Klein Financial Advisors in Irvine, working with her mother, Lauren. And no, Jamie did not have a falling out with her mom! Rather, Lauren sold her practice to a larger firm and is in the transitional phase of retiring, so Jamie thought, “it’s time for me to change too.” The irony of the situation is that Steve Medland has known Jamie’s Mom for about 15 years, through a financial planning study group, but Jamie found us (and vice versa) through traditional means.

We are all excited to have Jamie join our team. In her prior role, she has used many of the software programs we use, so it’s a matter of getting her familiar with Fidelity’s operations and the different ways we use some of the software, such as for billing and portfolio management. Make sure to introduce yourself to Jamie the next time you call, or make a point of simply calling her to say hi, and welcome. Many of you will get to meet her during your next office visit.

The End Of The World (Tour)

Many of you may know our son, Adam, has been working as the chief photographer and videographer for the past 16 months with the team of Kid Laroi. They began a world tour (literally) in May, shortly after Mother’s Day, starting with three weeks in Australia, where Laroi and his family are originally from. During June and July, they played shows in Copenhagen, Munich, Zurich, Paris, Amsterdam, Berlin, Birmingham, London and Manchester. After a five-day break in late July, they resumed touring in North America, starting in Toronto and Montreal, doing 27 shows in 40 days, including Minneapolis, Milwaukee, Detroit, Boston, New York, Philadelphia, Miami, Orlando, Dallas, Houston, Austin, Seattle, Phoenix, San Francisco and finished this past Saturday and Sunday at the Novo Theatre in Los Angeles.

Our family got to attend the final show in Los Angeles Sunday night, and meet Laroi and several members of his team before the show. Adam purposely had us be the last ones in line with the Meet & Greet, and didn’t tell Laroi who we were or what was going on. After our daughter Caroline said hi to him, and then my wife Michelle said hello, he responded “Wow, you have cool parents!” I then introduced myself only as

Bob, and asked him, “So Laroi, do you know how we’re connected to you?” He was truly stumped until one of his team, affectionately known as ‘Bird” told him to look to his right, as Adam was filming the whole thing. That’s all of us with Laroi above, with Adam on the left.

Above, that’s Adam with Laroi and Bird. They, and many others, are part of Laroi’s team that make everything happen, from travel, to wardrobe, security, food, set design and much more. When you are together as much as they are, both on the road and at home, you become family. We’re grateful that Adam is getting to experience his dream job, with such great people who care about him. Much love to Laroi and the whole team for continued growth and success.

Material Of A Less Serious Nature

I think the following photo needs no explanation. Yes?

Yes, it’s that time of year. NFL Football. If your spouse or significant other is involved in a Fantasy Football league, you too can count on them wasting countless hours wondering if Russell Wilson threw for any touchdowns, or Nick Bosa had any sacks, or whether or not they can elevate Devonte Adams to the starting lineup. Many women play too, you know. Me. Not. All I care about is my 49ers trying to win the Super Bowl. Not such a good start in Chicago. Fantasies? Mine are much more sordid. 🙂

A Jewish Rabbi and a Catholic Priest met at the town’s annual 4th of July picnic. Old friends, they began their usual banter. “This baked ham is really delicious,” the priest teased the rabbi. “You really ought to try it. I know it’s against your religion, but I can’t understand why such a wonderful food should be forbidden! You don’t know what you’re missing. You just haven’t lived until you’ve tried Mrs. Hall’s prized Virginia Baked Ham. Tell me, Rabbi, are you ever going to break down and try it?”

The rabbi looked at the priest with a big grin, and said, “Of course I will, just serve it at your wedding.”

If you didn’t realize it from our above comments, the forces of Supply and Demand are not aligned with a bullish view. Bear markets are a part of investing. In our view, the winners are the ones who lose the least, and stick with the plan, so they’re positioned to make gains when the markets reverse. And that is what our process is designed to do. You cannot avoid losing in a bear market. But, you can minimize the damage. Thanks for all your trust and confidence in us at TABR.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.