The “F” Word, and What it Means for Investors

No, I’m not referring to the four-letter slang word that many a golfer utters after hitting their tee shot into the water hazard or the trees. Instead, this is about a term called a “fiduciary,” which may be getting as much attention these days in the investment industry as Donald Trump, Hillary Clinton or Bernie Sanders are getting from their Twitter accounts.

In April, the Department of Labor (DOL) passed a rule governing the investment advice in regards to retirement assets. The rule indicates that brokers can no longer earn commissions and other forms of conflicted compensation unless they agree to do so via a Best Interests Contract (BIC) agreement, essentially forcing them to use a fiduciary standard of advice.

First, since a number of surveys show that investors are nearly clueless as to what the word “fiduciary” means, let’s start with that.

According to the freedictionary.com, a fiduciary is “an individual in whom another has placed the utmost trust and confidence to manage and protect property or money. The relationship wherein one person has an obligation to act for another’s benefit.

It went on to say the following. “A fiduciary relationship encompasses the idea of faith and confidence and is generally established only when the confidence given by one person is actually accepted by the other person. Mere respect for another individual’s judgment or general trust in his or her character is ordinarily insufficient for the creation of a fiduciary relationship. The duties of a fiduciary include loyalty and reasonable care of the assets within custody. All of the fiduciary’s actions are performed for the advantage of the beneficiary.”

In English, being a fiduciary means putting your clients’ interests first. To a client who is entrusting their money to an advisor, that might seem obvious, but it’s not. Only in recent years has the financial press started to beat the drum and attempt to educate investors about the differences of working with a broker who is typically only held to a suitability standard (think Merrill Lynch, Wells Fargo, Morgan Stanley, LPL, Raymond James and other independent broker/dealers), versus those held to a fiduciary standard (fee-only advisors such as TABR and others).

Why Only Retirement Assets?

As it currently stands, the new DOL rule, which is not scheduled to go into effect until at least April of 2017, only governs retirement plan assets, such as IRA accounts, 401 (k) plans and other ERISA type entities.

Personally, I’m puzzled by this. As is typical of government regulation, this new rule is 1023 pages long. The lawyers are already having a field day. The House of Representatives has already passed a bill to kill the rule. The Senate is reportedly going to do the same, though President Obama has indicated he will veto such an effort. I just don’t understand the favored treatment of retirement plan assets, as if they are more important than after-tax savings?

Our industry already has a pretty large trust issue with the investing public. The cynic in me says that the DOL, under pressure from Wall Street lobbying, watered down the bill. It’s like the government is saying, “well, we want to do something that will save $billions of dollars in wasted fees in 401 (k) plans, but we’re still going to allow Wall Street and insurance companies to fleece you with high commission products in the way of variable annuities, non-traded REITS and other partnerships and heavily loaded life insurance products, and get away with it.”

To be sure, there is a lot more wrangling and guidance to come, both from the DOL and possibly from the Securities and Exchange Commission (SEC), who regulate investment advisers. The SEC has been working on their own version of the fiduciary rule for several years, and it’s possible they may emerge later this year with a mandate that would force all advisers to become fiduciaries for all assets. We just don’t know.

An Example of Fiduciary Behavior

To be sure, even advisers such as TABR and other fee-only firms can never be totally without a conflict of interest, or a bias. But below, I’ll describe a couple of common situations that might paint a picture of what it looks like to act as a fiduciary.

You’re our client, with $700,000 in a trust, $300,000 in an IRA, a $150,000 mortgage remaining on their house with a 4.2% interest rate, and two years from retirement, with a preference for having no debt in retirement.

Because of this, we recommend the client take $150,000 out of their trust and pay off the mortgage. If part of that trust was in a portfolio that we were managing, we would be losing assets, and therefore, revenue, but would be doing the right thing for the client. That’s an example of a fiduciary acting in the proper way. We’ve had several clients follow this type of advice.

Another recent example is that in comparing the costs/expenses of a small 401 (k) plan, as we did earlier this year. When we got involved, the plan being considered by the client was from an insurance company, where the overall expenses, not counting record keeping and administration, but including TABR’s compensation of 0.75% annually, was to be 2.42%. Granted, it was a brand new plan with virtually no assets, but still, I knew this was excessive.

Instead, I tailored a proposal from American Funds, one of the largest and lowest cost active fund managers in the industry, and got the expenses down to 1.18%. In this case, the comparison was so wide it was pretty easy to make the right choice. I can tell you that in the opaque world of 401 (k) plans that include third party administrators, there is not always a lot of transparency or full disclosure. Sometimes, it is really hard to determine exactly what a plan is paying. And, it’s not that a client is obligated under a fiduciary standard to always select the lowest cost option. But, if a client doesn’t know all the facts, or the adviser doesn’t give them full disclosure, that is an entirely different story.

In the past year, we have been examining a few different 401 (k) plans that some small business owner clients either have, or are considering. What we’ve observed in a very limited sample is that many clients either don’t really know what they are paying in the way of expenses, or what they are being told and what they’re actually paying is substantially higher, with very poor and misleading disclosure. For instance, if you were told your plan expenses would be 1% annually, but in the fine print and language, it was revealed you’re really paying 1.25%, wouldn’t you feel betrayed, or misled? Apparently, the new DOL rule aims to eliminate these types of practices.

Having Skin in the Game

It is not clear at present what policies and procedures we may have to put in place to be in compliance with the new regulations. As mentioned above, they’re not final and are likely to be challenged in court. Since TABR and other fee-only advisers are already fiduciaries, the impact on how we run our business with clients is likely to be much less than the broker/dealers in the business who still operate under a commission/fee model. As we get into early 2017, there is likely to be more clarity to this whole area.

Though it is not required of a fiduciary, I do feel strongly about this area, which is what I call eating your own cooking. Even before we formed TABR, we have been investing our own funds in exactly the same investments that we place clients in. Simply put, we do not invest in things we are unwilling to put our own money in (with rare exceptions, such as an immediate annuity that doesn’t fit our particular needs). Research has shown that mutual fund managers who have a significant stake in the funds they run typically do better than fund managers who have no money in their own funds.

When you have your own money on the line, I believe you have a more vested interest in the outcome, and are going to be a lot more diligent than an adviser who does not. It’s certainly one of the things that makes us different. I hope it conveys what is intended—we believe in what we’re doing. We’re not the only ones who feel that way.

In a recent Wall Street Journal article, Tesla founder and CEO Elon Musk was asked about his personal borrowings and funding of his companies Solar City, SpaceX and Tesla. He responded, “if I ask investors to put money in, then I feel morally I should put money in as well. I should not ask people to eat from the fruit bowl if I have not myself been willing to eat from the fruit bowl.”

And finally, in a recent column discussing investor rights, Wall Street Journal columnist Jason Zweig said, “If an investment manager wouldn’t want his or her mother to buy a new portfolio, then it has no business being sold to the investing public either.”

If our industry adhered to these practices, there would be a lot less of the crap that is created and sold, and a lot more trust from the investing public. Ultimately, our business is built on relationships, trust and competence. Regardless of what the rest of the industry does, that is how we’re always going to act—with skin in the game and putting our clients ahead of us.

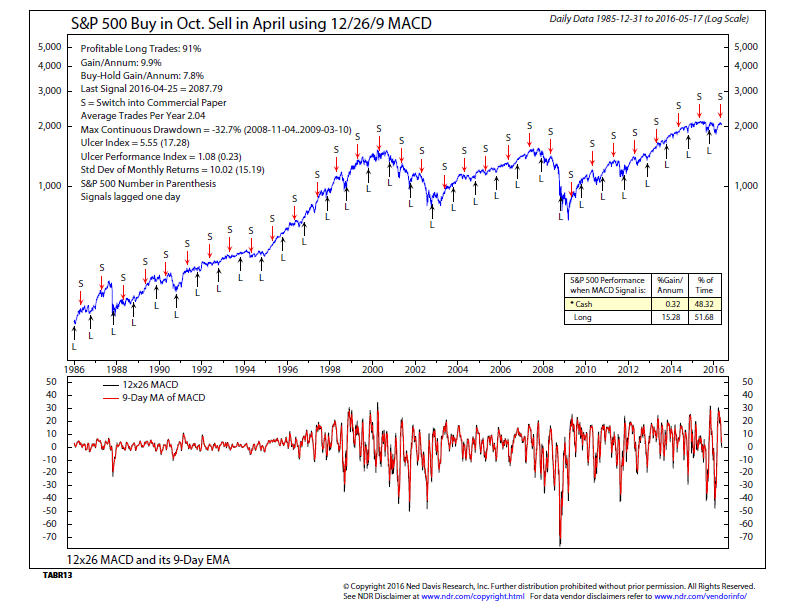

Say Hey, Sell in May?

We and others have written extensively about the strong and weak seasonal patterns of the stock market since 1950, which show the best six months to be invested being November to April, and the worst from May to October. This has been popularized by the Stock Trader’s Almanac, published by Yale Hirsch.

According to the numbers, if you owned the Dow Jones Industrials from October 31 to April 30, you would have earned an average of 7.44% annually since 1950, but only an average of 0.39% annually from April 30 to October 31. Please note those figures do not include dividends, which would make both numbers higher.

We’ve improved upon this strategy, thanks to the idea of Sy Harding, and used a momentum indicator called MACD (moving average convergence divergence, created by my dear friend and mentor, Gerry Appel) to exit and enter trades at slightly different dates.

The chart below is thanks to our friends at Ned Davis Research. It covers the period from December 1985 to present, and validates the research going back to 1950. Mainly, that on average, the stock market goes nowhere during the unfavorable time period, which we are now in.

It doesn’t mean that one should use it as a 100% guide and buy or sell everything in one’s stock portfolio. But, the edge is really significant to be part of an overall risk management process, which is how we use it. In 2015, using the exit and entry dates from our formula, the S&P 500 as represented by the Vanguard S&P 500 Index Fund dropped -2.63% including dividends, during the unfavorable period, and had a drawdown of nearly -11%. This year, we exited on April 25, so the fund gained 3.77% during the favorable period, and is already down nearly 2% from that date.

It’s only one model, and it does not work every year, but on average has worked quite well over time. We can’t know the outcome this year, either, but given the context of all the indicators we follow, I suspect the odds are high that stock prices will be lower in late October than they are currently. We’ll see.

Where We Stand with Investment Allocations

Very little has changed since our last monthly update. We cited then the evidence was mixed, and that tended to coincide with our positions. Our real estate model is still on a BUY. Our high yield corporate bond model is still on a BUY, in fact with very little deterioration. As mentioned last month, stock market breadth statistics were very strong off the February 11 low, and this normally bodes well for many months. High yield bond prices typically deteriorate BEFORE stocks begin to head down, as they did last summer. Normally, these would be bullish portents, but with the Fed in a sort of tightening mode and weekly charts beginning to look toppy, this is not a “normal” market.

Thus far, the majority of our tactical stock market risk models have failed to turn bullish, so right now exposure is about 40%. That we consider a notch below neutral. The S&P 500 and larger stocks continue to be the strongest segment, peaking a month ago, and down less than 3% from their peak, while small stocks and foreign stocks have fallen further. The S&P 500 will eventually either break above 2100 or drop below 2030, and only the market knows which. A mixed bag it still is.

Quick Note on Settlement of Trades

Last November, we replaced our core equity positions, where we had been using no transaction fee actively managed funds, with broad-based exchange-traded funds (ETFs). We’ve been meaning to remind clients that funds settle in one day, but ETFs take three days to settle. So, for those of you who don’t always think ahead when you need to withdraw funds which are above and beyond your normal income plan, please remember that it is going to take longer to raise capital than it has in the past.

Material of a Less Serious Nature

An Irishman, full of St. Patrick’s Day spirit, staggers into a Catholic church. He enters a confessional booth, sits down, but says nothing.

On the other side of the partition, the Priest coughs a few times to get the penitent’s attention. Getting no response, the Priest finally pounds on the partition three times.

The Irishman mumbles, “Ain’t no use knockin’, there’s no paper on this side either.”

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov.).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.