Will Hope Trump The Election? Pun Intended

Awful and empty. That’s how Wall Street Journal columnist Peggy Noonan recently described the two Presidential candidates. I thought that was spot on. You can read all the political commentary elsewhere. Here, though, we’re going to show you that the stock market just might be the most reliable forecaster of who wins the upcoming election.

In addition, we’ll have some interesting data on the aftermath of initial interest rate cuts, and how paying attention to detail in all likelihood saved one of our clients a loss of over $500,000. And appropriately, we’ll conclude with some election humor!

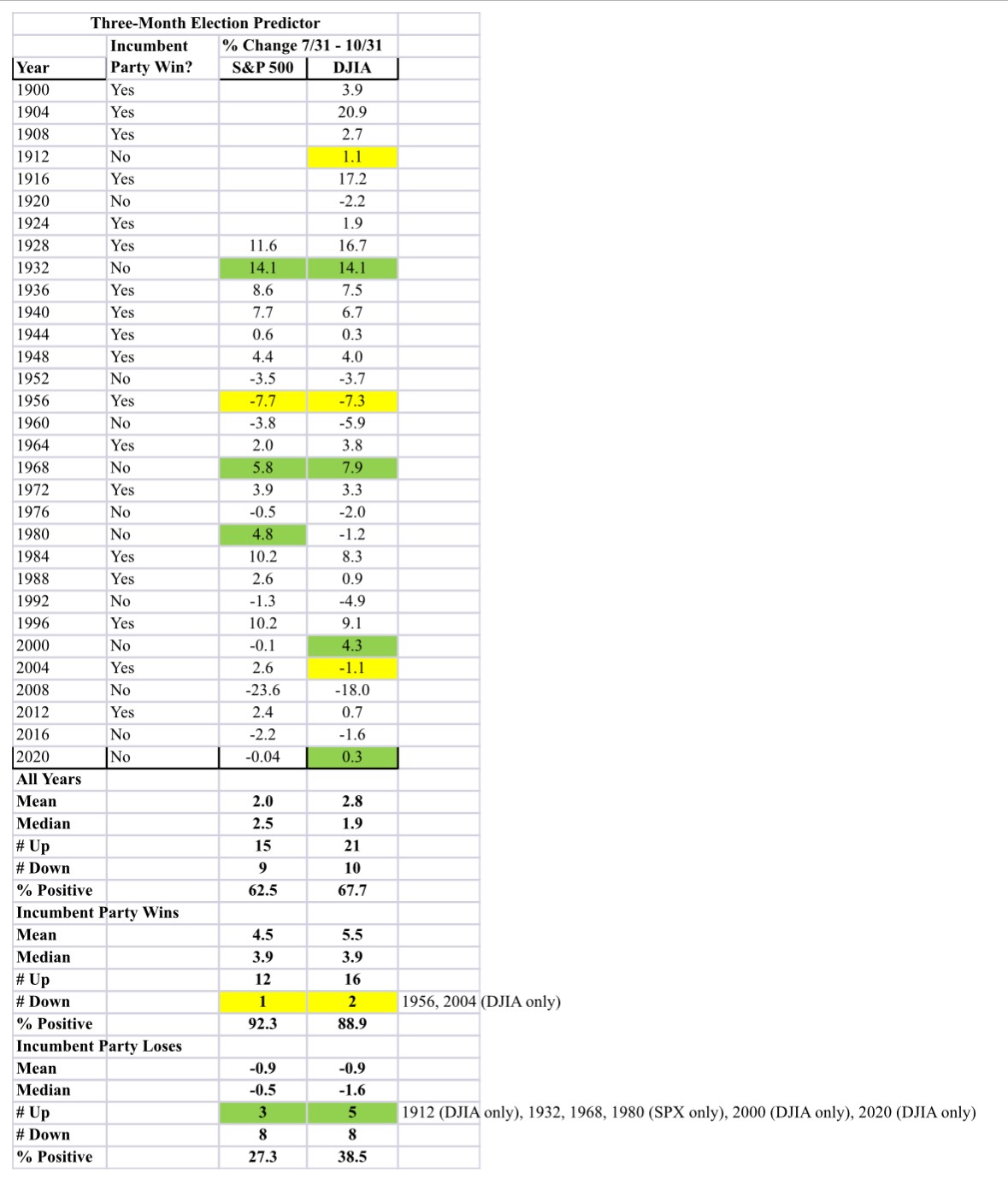

The 3-Month Election Predictor

Economists study all manners of data to predict the future course of the economy. Unemployment numbers, inflation, manufacturing indexes, retail sales, homes for sale, and the list goes on. Ultimately, the majority of economic forecasts miss the mark, just as do the majority of earnings estimates made by financial analysts when trying to forecast the quarterly earnings and sales of companies. What’s often overlooked in the complexity of economic forecasting is simply paying attention to what the stock market is doing. Though never perfect, a falling stock market (the key is how much?) has often been a harbinger of a coming recession. And a rising market has mostly foretold good times.

With the Presidential election less than one month away, there is no shortage of polls predicting the outcome. I would think polls are a lot less reliable today versus many years ago. Fewer people have land lines, and most of us don’t pick up our cell phones for numbers we don’t recognize. But, as technology has evolved, especially in the last 15 years, there have been several sites that have taken the data to a new level. Nate Silver of FiveThirtyEight went from being a baseball stats guy to a political stats expert, and developed an election forecasting system which correctly predicted the outcomes of 49 of the 50 states in the 2008 U.S. presidential election.

Like any model, nothing is flawless. In 2016, right before the election, FiveThirtyEight had Hillary Clinton with a 71.4% chance to win. You all know what happened. More recently, a few betting sites have cropped up where anyone can put skin in the game by betting on real-world events. The Polymarket platform fits that bill, although I should note that currently they are not allowed to operate in the U.S. They can’t offer betting to U.S. citizens, but U.S. citizens can use the platform by way of work arounds. In any case, the theory is rooted in sports gambling lore. Supposedly, the more money bet on a football team to win, the greater the probability the team will win. There are always upsets, though. Just ask Northern Illinois and Notre Dame, or last weekend, Vanderbilt and Alabama, in college football.

Nevertheless, in 2020, prediction markets gave Donald Trump just a 33% probability of winning, and that panned out. At present, FiveThirtyEight has Harris leading Trump by a 48.5% to 45.9% margin, and Polymarket is showing Trump just recently taking the lead in their forecast, at 53.3% to 46.2%. With data, these figures are pretty much toss-ups, and it will be interesting to see if much changes between now and election day.

The catalyst for this piece was my reading of a Fortune article a few weeks ago saying that since 1984, the performance of the stock market for the 3 months prior to the election had successfully forecast whether the incumbent party would win or not. This was intriguing, but not sufficient. That’s only 10 data points. It’s meaningless. But I wanted to see more, so I reached out to our research provider, Ned Davis Research (www.ndr.com), and with the help of analyst Ed Clissold, came up with the data below, which goes back to 1900, and covers the last 31 elections.

A couple of notes. Data on the Dow Jones Industrial Average goes back to 1900, but the S&P 500 only goes back to 1926. Here is the premise of the “indicator.” If the stock market shows a positive performance for the months of August, September and October, the probabilities favor the incumbent party to win. If the stock market is negative, the incumbent party should lose. You’ll note in the data there are a few instances where the performance of the S&P 500 and the Dow are different. We’re ignoring those, and sticking only with the Dow, simply because that gives us 31 data points rather than 24 data points, and that is statistically significant when you can look at 30-some data points (as mentioned earlier, 10 is pretty useless).

I should note that I recently read that newsletter writer and analyst James Stack of Investech Research may be responsible for this idea, but Stack’s version calculates the gains until election day, which doesn’t give one any margin. In our version, the outcome of the election has had a 77% success rate, with 24 of 31 prior cases being accurate. That’s obviously pretty decent. And where do things stand right now, with about 4 weeks to go? On July 31, the S&P 500 closed at 5522 and the Dow Industrials at 40,842, and as I write this, the S&P 500 is trading at 5790 with the Dow at 42,526. They are up 4.8% and 4.1%, respectively, from the July 31 close, so unless the stock market craters in the next 3 weeks, the odds are heavily favoring a Harris victory.

Though without precedent, another interesting twist would be to keep an eye on the following stock, which is Trump Media & Technology (DJT). This is a media and technology company in Sarasota, Florida that runs the Truth Social social media platform and is primarily owned by former president Donald Trump.

The stock went public last September at $16 and pretty much went nowhere until January, when it surged from around $16 to over $50 in one week, ultimately peaking in March at over $79. The stock then proceeded to decline, finally getting to $12 on September 23 before the recent run-up, supposedly fueled by comments from Elon Musk. Two weeks ago, as I planned to write this monthly piece, I would have said this chart is telling you that Trump has no chance to win. But, the performance of the stock in the next 3 weeks might be telling, if there happens to be a surge of so-called “smart” money betting on the stock. As mentioned earlier, at present the betting odds are a literal toss-up, but our 3-month predictor strongly favors Harris.

About the only thing that can be certain is what analyst Ed Clissold commented to me in an email—that on November 6 (which is the day after the election), half of America will think the world is ending. Ha!

Pay Attention To Cycles, Not Political Parties

I don’t want to spend too much time analyzing this area, because there is something for everyone, regardless of party favorites. Our main message is, and always will be, don’t worry about this stuff. Let the market do the talking. You’ll see below, in data provided by Ned Davis Research, that stocks have indeed done a bit better under Democratic Presidents. OK. But understand much of that difference was due to the 1930s when the stock market crashed from 1929 to 1932, under Republican leadership. Then, from 1992 to 2000, stocks soared under President Clinton, creating a major cycle top and the Internet Bubble, which President Bush inherited, where stocks went nowhere for 8 years. Then, President Obama took over for 8 years, coming into office at the bottom of the cycle. Did they all cause this? I don’t think so.

For those who want to peruse it, though, here is the data. What is shown are real returns, also known as inflation-adjusted returns, of the Dow Jones Industrial Average.

| When U.S. Government Has A: | % Gain Per Annum | % of Time |

| Democratic President | 3.80 | 48.15 |

| Republican President | 1.35 | 51.85 |

| Republican Congress | 6.52 | 32.42 |

| Split Congress | -0.77 | 15.86 |

| Democratic Congress | 1.10 | 51.72 |

| Democratic President, Republican Congress | 5.21 | 9.73 |

| Democratic President, Split Congress | 8.49 | 4.52 |

| Democratic President, Democratic Congress | 2.80 | 33.90 |

| Republican President, Republican Congress | 7.09 | 22.69 |

| Republican President, Split Congress | -4.23 | 11.34 |

| Republican President, Democratic Congress | -2.05 | 17.82 |

Sometimes, what is solid individually is not quite the same when put together. For instance, when you combine a Democratic President with a Republican Congress, you get respectable gains of 5.21% per annum, but that combination has only taken place less than 10% of the time. The best combination is a Democratic President with a Split Congress (as we have now), which shows gains of 8.49%, but has only happened less than 5% of the time. Right now, that outcome appears decently likely, since it is almost impossible for Democrats to gain control over Congress given the current data. A Republican sweep has been very good for markets, and has been in effect 22% of the time, but if history is any guide, and you’re voting your pocketbook, a Republican President with a Split Congress has been the worst combination. If Trump were to win, that outcome would be a likely reality.

By the way, median gains for post-election years going back to 1900 are 12.7%, but annual gains took place only 55% of the time, which is significantly below the norm of near 75%. All in all, with stock market valuations mostly in the 95th percentile historically, and stocks now finishing a string of strong returns since 2009 in the mid-double-digits annualized, I expect whoever wins the Presidency to reside over a very below average if not poor next four years. As they say, history may not always repeat, but it sure does rhyme.

My Moment With A President

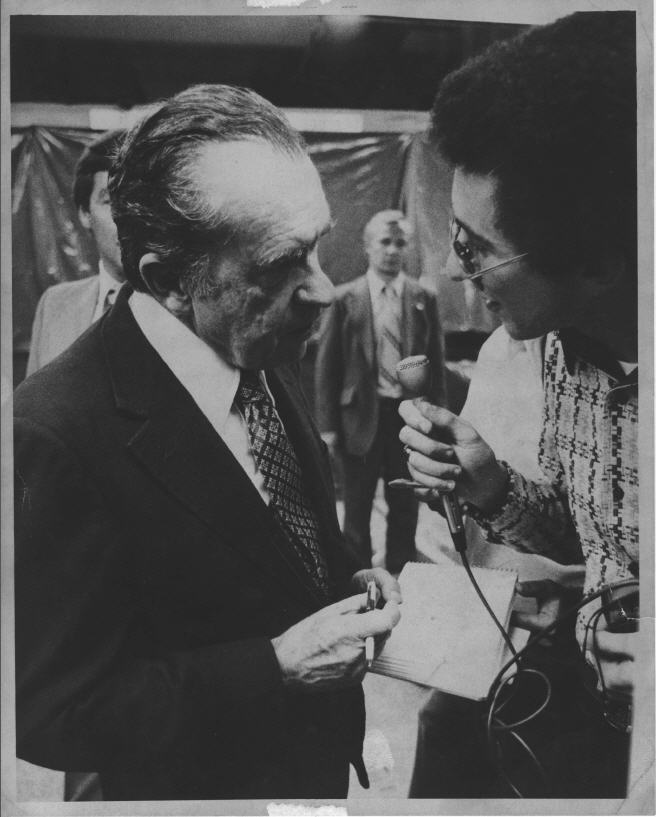

Since we’re talking Presidents and such, I thought I would regurgitate a photo from 45 years ago that I’ve published once before. It’s a fond memory that will always be with me.

The scene is September 1979. I was all of 21 years old, in the position of Assistant Director of Public Relations for the California Angels. My dream. The Angels had just clinched their first playoff spot, and post game, everyone was celebrating in the clubhouse, with beer and champagne. Former President Richard Nixon was at the game that day, as he and his wife Pat were good friends with Gene & Ina Autry, the Angels’ owner. Since the Nixon’s often stayed at their San Clemente vacation home, they attended Angels games from time to time and sat in the owner’s box. After the game, Nixon and Mr. Autry were in the clubhouse, congratulating the players and in my role in PR, I figured hey, I need some audio for our hotline, so I was able to get Nixon’s attention, which resulted in this photo below, taken by photographer David Hopley.

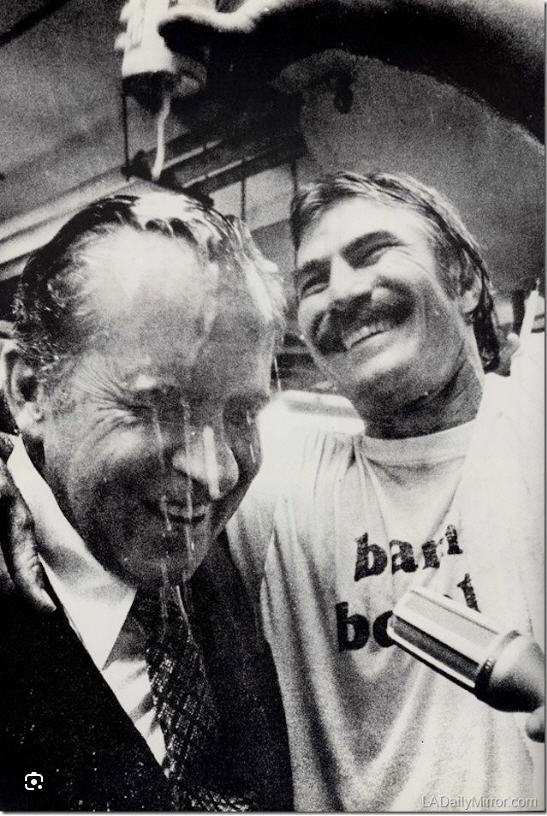

What’s so lasting though, and was just hilarious, was that while I had the President’s attention, unbeknownst to him, our All-Star second baseman, Bobby Grich, snuck up behind him and doused him with a Budweiser, declaring, “Mr. President, this Bud’s For You!” The resulting photo, which you see below, made it onto the front pages of nearly every major newspaper in the country. And no, Bobby and I did not plan this! It was a really cool moment, and Nixon was a great sport about it. I think it’s ironic that all these years later, since 2005-06, our family has resided in Yorba Linda, home and birthplace of Nixon and of course, the Nixon Library.

Initial Interest Rate Cuts

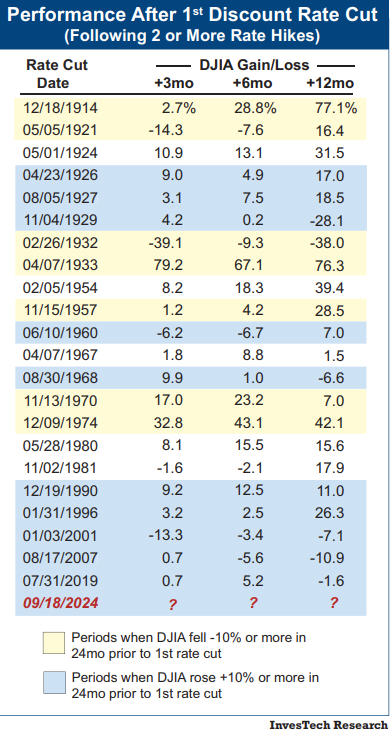

Two weeks ago, the Federal Reserve Board cut the Fed Funds rate for the first time since embarking on a run of 11 consecutive increases, which had increased the rate from 0-0.25% to 5.25-5.50% starting in early 2022 and ending July 2023. The Fed maintained that level until last week, and the rate is now at 4.75-5.00%. In general, cycles of declining interest rates have normally been positive for stocks, but not always. Most recently, those exceptions were in 2001 and 2007, both of which led to large bear markets culminating in losses of -45% and -56%. Plus, the first study I came across took the data only back to 1929.

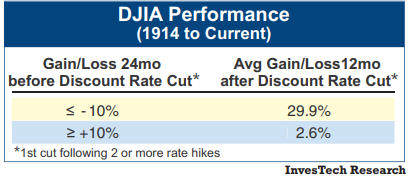

As I read further though, I found that context really matters. James Stack of InvesTech Research penned an excellent piece in his latest newsletter dated September 20, 2024 (www.investech.com). First of all, most of the time when the Fed is cutting, they are trying to get the economy going because the economy is bad and/or going into or is in a recession. That is not the case today, with the stock market basically making new all-time highs and no objective evidence even closely resembling a recession. Stack took the data back to 1914, and focused on the performance of the Dow Jones Industrial Average after the first cut in interest rates, that had followed at least 2 or more interest rate hikes. That table is below.

The key, though, was the performance of the stock market in the 24 months prior to the first cut. As the table below shows, when the performance was less than or equal to a loss of -10%, the average gain/loss in the subsequent 12 months was a gain of 29.9%. That makes sense. Things are depressed, the market goes up. But, when the prior 24 months performance was a gain equal or greater than +10%, the subsequent gain was a mere +2.6%.

Given that the S&P 500 gained 44% for the two years prior to the September 18 reduction, the future 12 months don’t look so hot given this past data.

Some’ll Win, Some Will Lose, Some Are Born To Sing The Blues

Those are part of the lyrics to Journey’s “Don’t Stop Believin.” And many of us are in the latter case, as the expected COLA (cost of living adjustment) for Social Security payees is expected to be 2.5% in 2025. That’s in line with the consumer price index during the last 12 months or so. And I’m not implying I am receiving Social Security, which I’m not (until age 70), but rather that I’m singing the blues, since our health insurance renewal at TABR just came in from Anthem Blue Cross, and our annual premiums for our policy covering myself, my wife and daughter increased by 13.66%. I guess you can’t win. You get older, your health insurance goes up. If you’re young, like our daughter at not quite 20, they get you on auto insurance for not being experienced. That’s life.

Be Careful With Bank Wires, And Pay Attention To Details

There will always be evil and good in the world. Part of our responsibility is to minimize the evil where possible. As I’m sure you know, financial crimes are happening all the time, and phishing and scams are all over the place, making it imperative to protect one’s data, and follow processes. One of those processes likely saved one of our treasured clients over $500,000 recently. Here’s the story.

Our clients were in the process of purchasing a new home, and were going to pay cash for it, take funds from their joint account at Fidelity, and then take their time in selling their existing home and eventually replace the funds at Fidelity with the proceeds from the sale of their home. Nothing out of the ordinary. They were working with an escrow company, and our client had sent an email to us, which was from the escrow company, with the bank wire instructions. An escrow officer was involved, along with the clients’ realtor, on an email chain where the realtor had provided the escrow company with our clients’ birthdates and email addresses.

When we got closer to funding the escrow, our client had forwarded an email they had received from the escrow officer, again with the wiring instructions, and indicated that they would be on vacation for a bit. Those instructions were also forwarded to us, and our administrative assistant, Sylvia. Especially on escrows, our process is to call the escrow company and verify the instructions over the phone. Why? Because there are evil people out there who somehow infiltrate these processes, take over accounts, and change the wiring instructions so that the funds go to a different bank, undoubtedly in the control of the crooks, and once that money gets wired to the wrong bank account, it will be gone in an instant, before any of it can be traced typically.

In this case, Sylvia noticed that the email address of the escrow officer had been subtly changed and was different, that the letterhead of the escrow company was slightly off, and that the bank and account number of the receiving bank were different than the first email we had received. These were all warning signs that something was off. When Sylvia called the escrow officer, we confirmed that in fact, none of the new information was correct and it was a fraud. The escrow company had no connection to the new receiving bank.

Had this information not been discovered, we would have likely wired over $500,000 to the other bank, and that money would likely have disappeared. We still cannot be certain where the breach took place. We called the escrow company with our client, and literally were talking with their top person in management, and after their investigation, they claim they could not find any breach on their side. We still don’t know if our clients’ email accounts were compromised, or that of their realtor, because emails were going back and forth between all three of them.

By the way, we filed an investigative complaint with the federal government and the financial crimes unit, and we attempted to contact the bank that was listed on the second “fake” email. It was a real bank located in Florida. I had an account number, but no account name, and I asked to speak to the top person in the bank. And despite my efforts to report what I knew was a fraudulent account, I got nowhere. The person wouldn’t give me the time of day, saying they couldn’t do anything unless they were contacted by the government. It was quite frustrating, feeling like the criminals have more rights than the people.

Taking care of your money goes beyond protecting against declines in stock and bond markets. Cyber theft is real, and scams are prevalent everywhere. Just yesterday, I got a text from an unknown number saying, “Hey, I’m visiting Disneyland in December. Do you still live near there?” I’m thinking, “who the f is this?” My practice is simply to delete these texts and mark them as spam, and block them. But this time, I replied, and said, “I don’t recognize your number.” And of course, I got a reply. It said, “Don’t you remember–we played golf when I last visited.” Haha. I just laughed, and deleted the number, and blocked it and reported it as spam. Maybe they know I live near Disneyland, but they sure as hell don’t know that I don’t play golf! Be careful with your email, your phone, everything.

TABR Portfolio Allocations

Our tactical accounts haven’t had a change in exposure in nearly 3 months, with equity exposure remaining at about 83%, and our high yield bond risk model still on its November 2023 buy signal, getting close to being almost one year long. Breadth statistics continue to confirm new highs, which is bullish for the intermediate term, and even negative seasonality of September and October so far have not mattered. It makes you wonder if the positive seasonality of November and December will work in reverse this year? Who knows? We don’t guess. When the evidence changes, we’ll change, but higher prices seem likely.

Material Of A Less Serious Nature

While stitching a cut on the hand of a 75-year-old farmer, whose hand was caught in the squeeze gate while working cattle, the doctor struck up a conversation with the old man.

Eventually the topic got around to politicians and their role as our leaders.

The old farmer said, “Well, as I see it, most politicians are ‘Post Turtles’.”

Not being familiar with the term, the doctor asked him what a ‘post turtle’ was.

The old rancher said, “When you’re driving down a country road and you come across a fence post with a turtle balanced on top, that’s a post turtle.”

The old farmer saw the puzzled look on the doctor’s face, so he continued to explain. “You know he didn’t get up there by himself, he doesn’t belong up there, he doesn’t know what to do while he’s up there, he’s elevated beyond his ability to function, and you just wonder what kind of dumb ass put him up there to begin with.”

Here’s my two cents. We have two Post Turtles running. And I’m voting for George Kittle. Again.

Finally, I found this on social media, and just cracked up. Here’s to President Reagan.

https://www.instagram.com/reel/C-YQAH0RrFn/?igsh=MTc4MmM1YmI2Ng%3D%3D

As I conclude this, the baseball playoffs are in full gear. My teams are on the sidelines (again), so I root against the Dodgers, and for my personal connections to Tanner Bibee of the Cleveland Guardians and Michael Lorenzen of the Kansas City Royals. Both are former Cal State Fullerton Titans. Meanwhile, school is in full throttle, with daughter Caroline just beginning her sophomore year at Cal Poly SLO, and my treasured 49ers are on the verge of a horrendous beginning (please don’t lose Thursday night to the hated Seahawks!). Meanwhile, son Adam and Kid Laroi and the team just got back from Sydney where Laroi performed a 15-minute set at the National Rugby Finals in front of 80,000 fans. That’s big league stuff!

As always, thank you for your trust and confidence in all of us, and for allowing us to serve you. Happy Halloween! And here’s also wishing a sweet and prosperous New Year to all of our Jewish friends and clients who are celebrating Rosh Hashanah this month.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.