Interest Rates May Change. The Reasons You Invest In Bonds Don’t.

I’ve been searching for an appropriate title for this quarterly edition of TABR’s newsletter for weeks. “Why Our Bond Strategies Are Different,” didn’t quite ring the bell, although it is a significant part of the message we’re trying to convey.

Then, last week I came across a full-page ad in the Wall Street Journal from Fidelity Investments (ironic since Fidelity is the custodian for our clients’ assets). The above title was the headline for the ad, which was touting one of their bond funds.

I had one of those ahh-ha moments. I thought, “That’s it!” So, below, we’ll be talking about the fact that interest rates will likely change, but the reasons you invest in bonds will not. We’ll also touch on what duration is, and how it relates to risk in bonds. There will be a real example of what just took place last year when bond yields surged rather quickly. And, yes, there will be commentary on why TABR’s bond strategies ARE different, and how that is.

In addition this quarter, there’s a long overdue piece on the Wells Fargo fraudulent account opening scandal, another story that conveys how our knowledge of the total picture allowed us to help a client save over $21,000 in annual expenses, an update on TABR’s Dividend Stock strategy, and finally, a quick review of 2016 performance. So, grab a cup of coffee and dig in.

Holding Bonds? Don’t Fret.

We get it. Stocks are sexy. Bonds are boring. In all likelihood, many of you have likely experienced at some point a holiday party conversation with a friend, where that person was extolling their good fortune. “I’ve doubled my money in Apple (or Facebook, or whatever).” Note—you’ll probably not hear about the disasters. But, chances are, you’ve never had anyone tell you how rich they’ve become over a glass of wine and some cheese and crackers because they’ve invested in the PIMCO Income Fund, or the Barclays Aggregate Bond Index or the Vanguard Total Bond Index.

Simply put, one has to understand the reason we invest in bonds, and the role they play in one’s portfolio. Many of you may be surprised to learn that at TABR, just over 50% of the capital we manage for clients is in our bond strategies. Hint—and that’s not because that is where the highest return may be over time. Rather, it’s to provide consistent income, stability and risk management.

Below, we’ve reproduced a table, courtesy of Morningstar and Research Affiliates, showing stock and bond returns for the past 100 years, broken down by decade.

| Decade | Stocks | Bonds |

| 1920s | 14.4% | 6.3% |

| 1930s | 1.8% | 4.6% |

| 1940s | 12.8% | 2.0% |

| 1950s | 16.3% | 2.1% |

| 1960s | 8.1% | 3.2% |

| 1970s | 8.4% | 4.0% |

| 1980s | 13.9% | 14.4% |

| 1990s | 17.6% | 9.4% |

| 2000s | 1.2% | 6.7% |

| 2010s | 8.9% | 3.2% |

| Average | 10.34% | 5.6% |

First, don’t get too caught up in the details of the data, such as what represented bonds and stocks? Many of the types of bonds we can invest in today (high yield, floating rate, mortgage-backed) didn’t even exist prior to about 1980, and there certainly weren’t mid-cap, small-cap and foreign stock indexes to buy back in the 1940s.

Just accept the notion that over a very long period of time, stocks have nearly doubled the return of bonds. If you go a step further and assume that over this same period, inflation has averaged about 3.5%, then the real return from stocks (after inflation) has been nearly 7%, while with bonds it has been about 2%.

Given this information, which is factual and can’t really be disputed, why would an investor choose to invest in bonds? Furthermore, why would a financial advisor recommend bonds if the goal was to maximize a client’s retirement portfolio over a 20 or 30-year time frame?

I’ll tell you why. It’s because of risk. To get the superior return of stocks, investors have had to endure maximum losses of over -50% a few times, and that excludes the anomaly of the -80% loss from 1929 to 1932. So, what is the risk in the bond market? A lot of people seem concerned about the end to the secular bull market in bonds which has been going on since about 1980. The consensus thought is that interest rates HAVE to go up, and bond investors are going to lose their shirt. We believe there is a lot of missing information in that narrative.

Much depends on the types of bonds one is invested in, what the strategy is (active management versus buy and hold until maturity), and what the duration of the bonds (or bond funds) is.

What Is Duration?

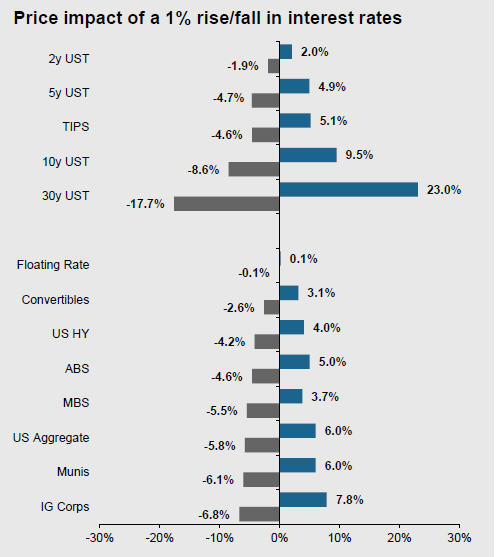

Unfortunately, our industry has a lot of complicated jargon. But, stay with me here. Duration is an approximate measure of a bond’s price sensitivity to changes in interest rates. If a bond (or bond fund) has a duration of 6 years, for example, its price will rise about 6% if its yield drops by a percentage point (100 basis points), and its price will fall by about 6% if its yield rises by that amount.

Below is a helpful table from J.P. Morgan Asset Management which illustrates the price impact of a 1% rise or fall in interest rates of various types of bonds.

As it turned out, we had a significant jump in bond yields last year, as the 10-year Treasury Note bottomed on July 8 at 1.36%, and jumped 123 basis points by December 16, when it closed at 2.59%. It closed the year at 2.44% and sits at 2.43% as of February 21.

So, what happened to various types of bonds and bond funds in this environment? Take a look at the table below, which includes many of the bond funds we use in client portfolios, along with several other broad examples. The returns shown in the far right column under drawdown include dividends and are for the period July 8, 2016 to December 16, 2016.

| Fund | Duration | Yield | Drawdown |

| TLT 20 yr Treasury Bond ETF | 17.77 yrs | 2.59% | -17.65% |

| Franklin Calif Tax Free Fund | 6.34 | 3.62 | -6.36% |

| Vanguard Total Bond Index Fund | 6.02 | 2.38 | -4.64% |

| Guggenheim Bullet Share 2024 Fund BSCO | 6.24 | 3.03 | -4.94% |

| Sierra Strategic Income Fund SSIRX | 5.26 | 3.00 | -0.54% |

| Blackrock High Yield BRHYX | 3.70 | 5.66 | +5.35% |

| PIMCO Income Fund PIMIX | 2.62 | 5.50 | +3.21% |

| Fidelity Short Term Bond FSHBX | 1.62 | 0.99 | -0.52% |

| PIMCO Short Term Bond PTSHX | 0 | 1.78 | +1.74% |

| TABR All Bond Account | n/a | n/a | +0.59% |

We’ve listed the examples by duration, with the longest at the top, being the 20-year Treasury Bond, and the lowest at the bottom, the PIMCO Short Term Bond. I know, you’re probably asking how does a fund have a duration of zero? First, the figures for duration and yield were taken from Morningstar, and they are current. The managers at PIMCO run bonds differently, using a lot of derivative strategies, and this is one of the reasons their funds went up even as interest rates increased. As for TABR’s all-bond account, we don’t necessarily have static positions, so duration and yield can change for our portfolio when allocation changes are made.

You can see from the table that in general, the longer the duration, the bigger the loss. There were some differences, though. The Sierra Strategic Income Fund with a duration of just over five years, lost only -0.54%. How did that happen? We own a small piece of this fund in almost all of our portfolios. It just so happens that Sierra is a tactical manager (much like TABR), and they take disciplined, protective action when prices deteriorate (not to mention having a plan to re-enter markets).

You’ll also note that Blackrock High Yield actually earned a 5% plus profit while interest rates were rising. This was not an anomaly. The other high yield corporate funds we use also were positive, at varying rates of return. This asset class represents 60-65% of our overall bond exposure, but it is coupled with our risk management models.

Finally, you’ll note that TABR’s all-bond account also earned a positive return during this period. This is because the only parts of our bond allocations that lost money were short duration funds, which lost very little (such as Fidelity Short Term Bond), Sierra, which was mentioned above, and the Bullet Share from Guggenheim (BSCO). I should note that this particular position is designed to be held until near maturity in 2024, so what happens to its price is mostly irrelevant.

All in all, we feel that proper active management in bond funds can be extremely beneficial to the bottom line and makes a potential secular bear market in bonds not nearly as scary as it may seem.

What To Expect—2.75% to 3% Appears To Be Key

Forecasting that interest rates would rise for the past several years has been an exercise in futility. Long time readers of our work know that we think forecasting is a waste of time. Dealing with the evidence as it takes place is our preferred process.

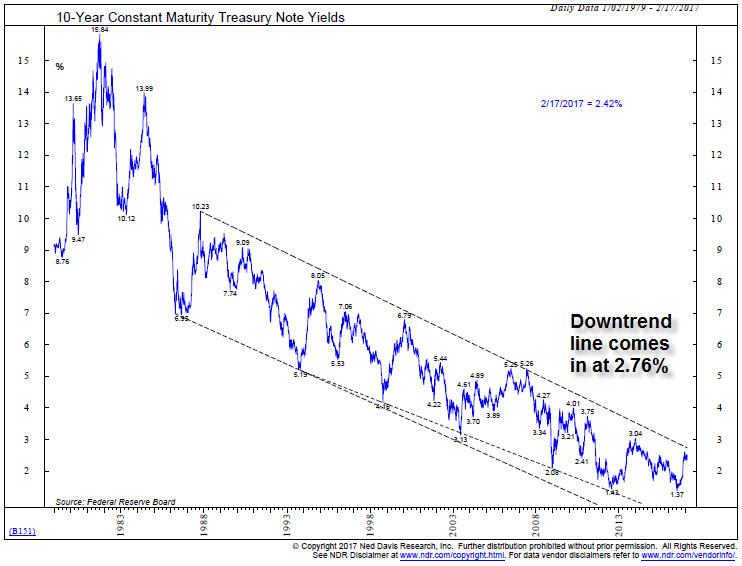

Entering 2017, the Federal Reserve Board has indicated they expect to increase short term interest rates (the Fed Funds rate) three times this year. Based on their past, investors would be wise to take this with a grain of salt. Entering 2016, they projected four hikes, and barely provided one, in December 2016. In our view, it is better to let the market tell you. Below is a chart courtesy of Ned Davis Research depicting the 10-year Treasury Yield back to 1979, with a price channel extending back to about 1987.

The downtrend line they’ve drawn comes in at 2.76%. The strategists at NDR feel that if this yield level is broached, “it would indicate significant technical and fundamental damage, and likely signal the end of the secular bull market for bonds.” Similarly, Jeff Gundlach of Doubleline Capital, and one of the best bond managers in the business, thinks the 3% level is the magic number.

No one really knows, though. Gundlach was one of the few in the business who predicted Donald Trump would win the Presidency, yet, he was dead wrong in suggesting that stocks in 2016 were going to do quite poorly. Our advice is to let the bond market tell the story. For what it’s worth, there is more global debt outstanding today than in 2007 before the mortgage meltdown, so I personally believe the Fed is going to be quite deliberate in raising interest rates. I expect them to err on the side of caution—slow and steady.

Conclusion For Bond Investors

If you’re concerned about fixed income and rising rates, you need to consider WHY you’re investing in bonds in the first place. Many investors are concerned about the potential damage that rising rates could cause to their bond allocations. We believe many of these fears are without merit, especially if one is using the strategies that TABR favors in their bond market allocations.

Why The Wells Fargo Scandal Is A BIG Deal

This is old news (September 2016), but it is not irrelevant news. I’ve just not had time or space to include some thoughts on it since it became everyday business news. To recap, federal regulators said Wells Fargo Bank employees secretly created over 1.5 million unauthorized bank and credit card accounts—without their customers knowing it—-since 2011. The accounts were allegedly opened so thousands of employees could meet sales targets and receive bonuses. Wells Fargo has confirmed that 5,300 employees have been fired over the last several years in relation to this behavior.

As they should have been, but one has to look at the culture of the firm, and how something like this could happen. It is especially timely because of the current focus of the Department of Labor trying to pass a new rule requiring advisors to act as fiduciaries on behalf of their clients (see a prior TABR Update on that subject). Were the employees looking out for the best interests of the clients, or the best interests of themselves and the bank? Everyone should know that answer.

Do you know what we at TABR would need to do in order to open an unauthorized account for a client at Fidelity? At a minimum, we’d need to forge a clients’ signature several times, on both Fidelity’s documents as well as TABR’s. Do you know where that would get us? I’m pretty sure we would be barred from the industry.

Needless to say, we take the issue of trust with clients quite seriously. Investors shouldn’t have to ask if their advisors have their best interests at heart, but in today’s world, they need to, because in today’s world, there are significant differences between advisors who work at Morgan Stanley, Merrill Lynch, an independent broker-dealer that can receive commissions, a life insurance person hawking annuities compared to a fee-only RIA who is an acknowledged fiduciary.

Just last week as we were initiating the paperwork with a new client, one of the spouses stopped in the middle of the process and looked at me and said, “please assure me you’re not another Bernie Madoff.”

Madoff, of course, is in jail for the remainder of his life for misleading his clients for over 20 years by producing fake statements that purportedly showed they were making money all the time. His clients trusted him, but there were no safeguards between Madoff and the clients’ money.

Ultimately, as financial advisor and blogger Carl Richards wrote in an October 2016 piece, “trust is the single most valuable asset that any real financial advisor has.” He goes on to say this. “Here’s why I think it’s the most valuable asset, and here’s why I think I can argue that. Just for a minute, I want you to take that asset away. Let’s say you did something tomorrow, and it’s not hard to imagine what you could do to have this result, but let’s say you did something tomorrow to lose the trust of your current clients, your future clients, and your community, and collectively the world, right?

“Let’s say you did that. What would you have left? If you lost that asset, I don’t think we have to argue that you would have nothing, right? Sure, you can rebuild, of course, but at that moment, you would have nothing.”

I think Richards is right on. Wells Fargo, of course, is a lot bigger than TABR, so they’re not likely to go out of business, but they have taken a massive PR hit and lost a lot of credibility. By the way, some full disclosure. I have a couple of accounts there with our son, and formerly had one with my mother prior to her passing last year. In addition, we actually bought and sold Wells Fargo stock in TABR’s Dividend Stock accounts last year. This was entirely due to our quantitative screening process.

The buy took place on October 3 at about 43.61 per share, and we exited the position on January 3 at 55.73 for a gain of over 27%. We don’t personally know of anyone who has been harmed by what took place at Wells Fargo, but I think the message should be clear. Two-way, honest communication, trust and transparency is the only way to go. It’s not a one-way street, by the way. Importantly, advisors also need to be able to trust their clients.

What We Do When No One’s Looking (another installment)

In our July 2016 newsletter, you may recall we introduced this section in response to our daughter, Caroline, asking us, “Daddy, what do you do at work?”

In this particular story, one might think that the refinancing of a mortgage is not particularly earth shattering. However, not all refinance situations are simple or alike, and the key is that we had the entire picture of our client in our grasp, which allowed us to come up with the solution we recommended.

In this case, our clients owned their own home, and had a small first mortgage on it of $117,000 along with a small home equity line of $122,000. These amounts were quite small relative to the value of their primary residence. In addition, they owned two vacation properties, one of which was fully paid off, and worth about $500,000, while the other property was worth about $750,000, but had a $475,000 mortgage at 4.375%.

All told, combined mortgage payments for principal and interest were running about $4500 a month, so I was thinking of ways to simplify things and reduce payments (and the interest rate). In this process, we discovered one other fact which we were unaware of, mostly because it had occurred in the past year between our annual meeting where we review everything.

They’d inadvertently taken on about $64,000 of credit card debt related to various home projects. Never mind that they could have taken those funds from their taxable accounts with us. They just hadn’t got around to dealing with that. So, they were also paying this down at about $800 per month.

With the help of the mortgage broker who has helped a number of our clients, some with some pretty complex situations, we were able to accomplish a cash-out refinance. This allowed them to pay off the second vacation property, pay off the first and second mortgage on their primary home, pay off the credit card debt and roll it all into one first mortgage at 4% for 30 years, with monthly payments of $3580. This is saving them $1759 a month, or over $21,000 annually.

At some point, they’re planning on selling the smaller vacation property, at which point they will have several flexible options. They may pay down the new loan using a recast, which would result in additional savings without a refinance. They might add to their taxable investment account and begin taking an income for certain goals, or they might choose to help their kids and grandchildren with certain things. Or, they might do all three.

Without a regular review process that looks at everything, I don’t think we would have been able to be nearly as helpful. As it turned out, the timing was good as we were able to lock in their rate right before yields jumped after the Election. And, we learned some things about mortgages that we really didn’t know. There can be some big differences between a simple refinance of one’s primary residence, as opposed to a cash-out refinance, or the refinance of a rental property.

It’s nice to collaborate with other professionals in our field who really know their stuff, and ultimately, this helps our clients.

The TABR Dividend Stock Strategy—An Update

In August 2014, we unveiled research on a new strategy we were about to roll out which focused on S&P 500 companies with a combination of high dividend yields and high earnings yields. We were able to take the study back to the beginning of 1973. In our backtest, we discovered the strategy had an edge of over 400 basis points annually, net of fees, in comparison to buying and holding the S&P 500 Index. However, the biggest drawback was the maximum loss of nearly -60%, which wasn’t any better than buying and holding the index.

We initiated a real-time account in September 2014 with $102,000 and now have two years and three months of history. This is a brief recap on how things are progressing.

| S&P 500 (VFINX) | TABR Dividend | Income | |

| 2015 | 1.25% | -9.09% | $3,688 |

| 2016 | 11.82% | 13.34% | $3,478 |

| 27 months | 7.9% compounded | 5.01% compounded |

As you can see, the strategy had a rough 2015, but rebounded nicely last year, though the full year data does not tell the whole story. On June 30, the account was down just over -2%, but then gained 15% in the last six months, much of that concentrated in the fourth quarter. This is a great reminder that all factor-based strategies go through regular periods of underperformance, and sometimes this underperformance is significant.

There are two other areas to consider with this strategy—one is the drawdown and the other is the regular income. Unlike the backtested research, we are not fully invested at all times. In 2016, the accounts began the year 50% invested, but by March 16 were up to 80% and then became fully invested on April 25. At present, accounts are about 82% invested, with the rest in a short term bond fund.

Thus far, the strategy’s worst drawdown has been -16%, while the worst for the S&P 500 has been -14.2%. So, we haven’t been thrilled with that, but we’ve not completed a full market cycle so the jury is far from done.

One of the most important statistics is how much income is being provided, and not necessarily what the account is worth at any given moment. Thus far, income has averaged about 3.5% on original capital, and the current portfolio is projected to earn $4108 this year, but that will be a moving target, since we re-balance each quarter and we also cannot know if our risk models will reduce exposure later in the year.

We’re currently managing 30 accounts and some of the names in the current portfolio include Ford Motor, Best Buy, Dow Chemical, H&R Block, IBM, Target, Valero Energy and Verizon. We’ve been cautious about stock valuations, and certainly felt that way going into 2016, and yet the strategy earned 13%. One never knows. But, we are looking to add capital and expand to a number of interested clients when significant weakness takes place.

TABR Strategies for 2016

We’ve always found it useful to look backwards and contemplate what we’ve done. This can be helpful even when things seem to be going right, but even more so when they’re not. It’s how one can make course corrections, and fix things.

Transparency has been a fixture at TABR since we were founded in 2004. The vast majority of RIAs in our business do not publish a track record. They may cite compliance issues, or the work necessary to comply with regulations, or that all their clients have “customized” portfolios. Simply put, we do publish one, because we believe in our process, and our staff backs that up by investing the vast majority of their personal savings in the exact same strategies we use for clients.

Sometimes, the numbers aren’t pretty. That is part of being in investment management. Even the best money managers in the business go through years of underperformance. We are no different. The key is, in our view, sticking with your discipline, but also having the courage to fix things when something may be amiss.

And though below you will see comparisons to industry benchmarks, ultimately we are judged by helping our clients achieve their goals, with substantially less risk than passive, buy and hold strategies. Besides our combined 47 years of financial planning and investment management wisdom, that is probably the one big difference and edge we have over competitors.

In the past, we devoted a substantial amount of detail to the performance of each of the funds we use. We’re going to attempt more simplicity this year. It’s like when I was looking for a big screen TV and the guy started to tell me about how many pixels were in the TV. My eyes started to glaze over. If you want more detail than we’re providing here, just ask. We have it. But as I continue to grow and gain even more experience, we realize that most clients just want to know everything is OK.

In the last few months, we’ve all witnessed in sports the cliche, “it’s not how you start, but how you finish.” That was true of the stock market last year. On November 4, just four days prior to Election Day, the S&P 500 Index was up about 3.6% for the year. By December 13, it had gained an additional 9%, while mid-cap and small-cap indexes surged 14% and 18%, respectively in the same time span.

Stock Allocations

This was the first full year of using ETFs as our core equity exposure, which represents 50% of the pie. Only two trades were made the whole year for the core, selling QQQ (Nasdaq 100) and IJK (mid cap growth), and replacing them with IJJ (mid cap value) and IJH (mid cap). The other two holdings remained constant, RSP (equal weight S&P 500) and the IJT (small cap growth). This part of the pie gained 16.13% for the year, versus the equity benchmark which gained 10.55% (75% Vanguard Total Stock and 25% Vanguard Total International Stock).

That’s outstanding, but our allocation percentage to equities, which averaged 51%, offset much of this advantage. Overall, our stock market risk models turned out to be a bit too conservative. In real estate, the Dow Jones Real Estate Index (IYR) gained 7.01% for the year, but our slice allocated to this area lost -4.94%, as our trend model for this area got whipsawed twice. Not so hot. Finally, the position in the Leuthold Core Allocation Fund gained 4.51%, but this was behind its category.

Bond Allocations

The benchmark Vanguard Total Bond Fund was up over 6% at mid-year, but ended the year up just 2.50%. Each of our bond strategies Trumped this (OK, I couldn’t resist), and TABR’s all-bond account gained 6.99%. About 60-65% of our bond money is devoted to corporate high yield, in combination with short term bond funds, and our risk model for high yield.

Full-year returns for high yield funds we use ranged from 12.70% for PIMCO High Yield to 16.04% for Lord Abbett High Yield. The Morningstar High Yield category averaged 13.3%. For short term bond funds, returns ranged from 0.95% for JP Morgan Short Duration to 3.97% for Lord Abbett Short Duration. The Morningstar category averaged 2.08%.

Our other holdings included PIMCO Income, up 8.72%, Sierra Strategic Income, up 6.23% and the Guggenheim 2024 Investment Grade Bullet Share, up 6.15%.

Below is the performance, net of management fees, of TABR’s five different portfolios at present. These represent a majority of the strategies we are using in client accounts, but not all. The differences are mainly attributed to risk (example—moderate allocation versus conservative allocation or aggressive) and account size. The numbers are for the one year ending December 31, 2016.

| Type of Account/Strategy | 2016 Return | Benchmark |

| TABR Tactical Moderate | 5.56% | 6.83* |

| TABR Tactical Conservative | 5.34% | 5.72** |

| TABR Bond Account | 6.99% | 2.50%*** |

| TABR Dividend Stock | 13.34% | 11.82**** |

| TABR Passive Index Mix | 7.75% | 7.33%***** |

| Vanguard Total Stock Market Index | 12.53% | n/a |

| Vanguard Total International Stock Index | 4.65% | n/a |

| Vanguard Total Bond Market Index | 2.50% | n/a |

| Vanguard S&P 500 Index Fund | 11.82% | n/a |

*consists of 40% Vanguard Total Stock Index, 15% Vanguard Total International Stock Index and 45% Vanguard Total Bond Index

**consists of 30% Vanguard Total Stock Index, 10% Vanguard Total International Stock Index and 60% Vanguard Total Bond Index

***Vanguard Total Bond Index

****Vanguard S&P 500 Index Fund

******consists of 45% Vanguard Total Stock Index, 15% Vanguard Total International Stock Index and 40% Vanguard Total Bond Index

Returns shown are net of management fees, and include reinvested dividends

In Closing

Our regular monthly commentary will be published near the end of February. At present, most major stock indexes are at all-time highs, and this is being confirmed by breadth indicators. There are no divergences warning of an important top, so we’re expecting prices to be higher in three to six months. The second half of 2017 is likely to be more problematic than the first half with respect to financial markets, and we continue to believe the actions of Federal Reserve policy will be quite important.

Stock market valuations are excessive in relation to history, and sentiment is excessively bullish, but the trend is up, and this demands a moderately bullish stance, which is what we have. At some point, all of this will change, as will our indicators. Until then, we’re trying to enjoy the ride, and celebrating the beginning of another college baseball season for my # 8 ranked Cal State Fullerton Titans. We’ll see if we can get back to Omaha in June.

All of us at TABR are grateful for the trust and confidence you express in us daily.

Sincerely,

Bob Kargenian, CMT

President

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund and the Vanguard Total Bond Index Fund is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The TABR Dividend Strategy presented herein represents back-tested performance results. TABR did not offer the Dividend Strategy as an investment strategy for actual client accounts until September/October 2014. Back-tested performance results are provided solely for informational purposes and are not to be considered investment advice. These figures are hypothetical, prepared with the benefit of hindsight, and have inherent limitations as to their use and relevance. For example, they ignore certain factors such as trade timing, security liquidity, and the fact that economic and market conditions in the future may differ significantly from those in the past. Back-tested performance results reflect prices that are fully adjusted for dividends and other such distributions. The strategy may involve above average portfolio turnover which could negatively impact upon the net after-tax gain experienced by an individual client. Past performance is no indication or guarantee of future results and there can be no assurance the strategy will achieve results similar to those depicted herein.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.