How Proposition 19 Is Still Saving Some Homeowners Thousands

A few clients have asked about Proposition 19 recently, so I thought it would be useful to revisit the topic and update what I wrote when I first covered it in 2023. Most people think of Prop 19 as an inheritance issue, and that is certainly part of it. But it can also be helpful for longtime California homeowners who want to move and carry their low property tax basis to a new home.

That second part is worth paying attention to. For some homeowners age 55 or older, as well as certain disabled homeowners and victims of wildfire or natural disaster, Prop 19 may make it easier to downsize, relocate, or move closer to family without giving up a low assessed value built over many years.

First, though, a quick update on the story that prompted my original article. My parents’ neighbors had inherited a Southern California home and were surprised to receive a notice saying the property tax bill was going up by about $14,000 per year. At first glance, it looked like a mistake. Unfortunately, it was not. Under Proposition 19, inherited property can be reassessed to current market value unless the new owner meets certain requirements and files the right paperwork.

The good news was that their situation was correctable.

They filed the required form, qualified for the parent-to-child exclusion, and reduced the new taxable value substantially. In round numbers, that saved them about $10,000 per year in property taxes.

That article was written almost three years ago. Since then, the savings have added up. Depending on the timing of the county’s reassessment and the tax years involved, they have now likely saved somewhere in the neighborhood of $25,000 to $30,000. More importantly, the savings will continue to build in future years. Their taxable value remains much lower than it would have been if the home had been fully reassessed to market value.

That is real money. It is the kind of planning issue that can affect retirement income, family cash flow, or the decision to keep or sell an inherited home.

A Quick Refresher on Proposition 19

California’s property tax system is unusual. Under Proposition 13, property taxes are generally based on the assessed value of the home when it was purchased, with annual increases limited to no more than 2%, plus local assessments and voter-approved bonds.

That’s why two neighbors with similar homes can have very different property tax bills. One family may have bought their home in 1980 and be paying taxes based on a relatively low assessed value. Another family may have bought the house next door last year and be paying taxes based on today’s market price.

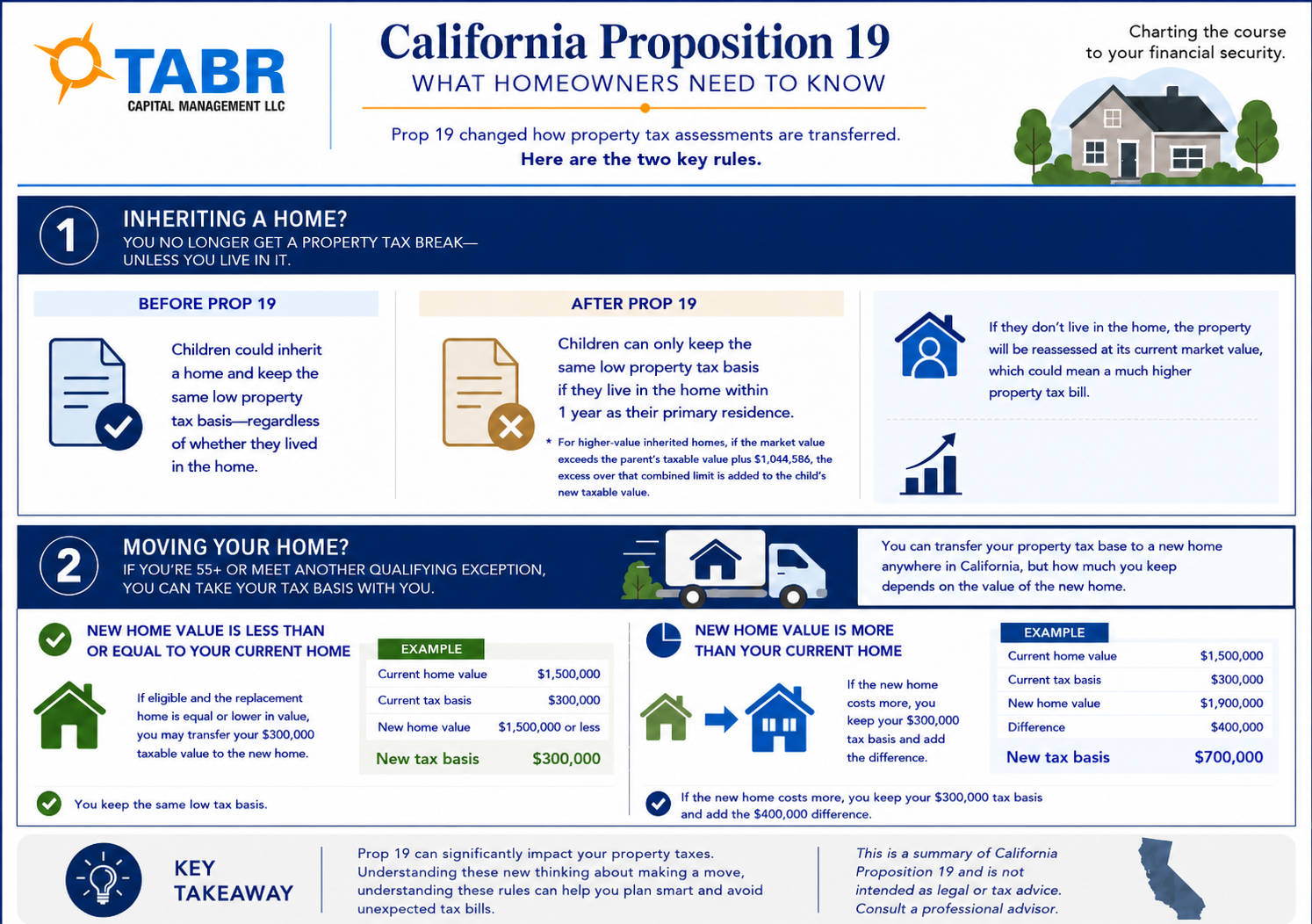

Proposition 19, approved by California voters in 2020, changed two major parts of this system.

First, it narrowed the old parent-child and grandparent-grandchild property tax exclusion. Before Prop 19, parents could often transfer a primary residence to their children without triggering a reassessment, whether or not the child moved into the home. Today, the inherited home generally must become the child’s primary residence to qualify for the exclusion.

Second, Prop 19 expanded property tax portability for certain homeowners. Homeowners who are age 55 or older, severely disabled, or victims of wildfire or natural disaster may be able to transfer the taxable value of their current primary residence to a replacement primary residence anywhere in California.

In short, Prop 19 took away some benefits for inherited property while expanding benefits for homeowners who move during their lifetime.

The Inheritance Rules Are Still Catching Families by Surprise

The biggest problem I see is that many people still assume the old rules apply.

They assume that if Mom and Dad bought the house decades ago, the children will inherit the low property tax basis automatically. That is no longer true in many cases.

Under current rules, the parent-child exclusion generally applies only to a family home or family farm. For a home, the child must use the property as a primary residence, and the exclusion is capped. Rental properties, vacation homes, and other investment properties generally do not receive the same treatment.

Even when a child does move into the inherited home, there are filing requirements. The child generally needs to file the proper reassessment exclusion claim with the county assessor and also file for the homeowners’ exemption or disabled veterans’ exemption within the required time period.

The timing also matters. Missing a deadline may not always destroy the benefit completely, but it can delay when the benefit begins and may cause unnecessary tax bills in the meantime.

That was the key issue for my parents’ neighbors. The law gave them a way to reduce the reassessment, but the county was not going to apply it automatically without the correct claim.

The Exclusion Amount Has Increased

One update since my 2023 article is that the exclusion amount has been adjusted upward.

When Prop 19 first became effective, the exclusion amount was $1 million above the property’s factored base year value. That amount increased to $1,022,600 for transfers from February 16, 2023 through February 15, 2025. For transfers from February 16, 2025, through February 15, 2027, the amount is now $1,044,586.

That helps, but it doesn’t fully solve the issue for many California families. Home values in many parts of the state have risen so much that even a $1 million-plus exclusion may still leave part of the property subject to reassessment.

Here is the basic idea.

Suppose a parent’s home has a taxable value of $300,000 and a market value of $1,600,000, and the child moves in as their primary residence after inheriting the home. Using the current exclusion amount, the protected amount would be approximately $1,344,586, which is the $300,000 taxable value plus the $1,044,586 exclusion amount. The excess value, roughly $255,414, would be added to the existing taxable value. The new taxable value would be about $555,414 instead of $1,600,000.

That is still a meaningful benefit. But it is not the same as keeping the old assessed value entirely.

The Portability Side May Be More Useful Than People Realize

The other side of Prop 19 deserves more attention.

For homeowners age 55 or older, Prop 19 can be helpful when selling a longtime primary residence and buying another California home. Before Prop 19, these transfers were more limited by county and, in many cases, could be used only once. Now, eligible homeowners may be able to transfer their taxable value to a replacement home anywhere in California, up to three times.

This can be especially useful for retirees who want to move but feel trapped by their current property tax bill.

For example, a couple may own a home worth $1.5 million with an assessed value of only $300,000. If they sell and buy another home for an equal or lower value, they may be able to transfer that $300,000 taxable value to the new home.

If they buy a more expensive home, part of the excess value may be added. So, if they sell the $1.5 million home and buy a replacement home for $1.9 million, the extra $400,000 would generally be added to their transferred assessed value. In that case, the new home might be taxed based on an assessed value of roughly $700,000 instead of $1.9 million.

There are important timing requirements. In general, the replacement home must be purchased or newly constructed within two years of the sale of the original home. The claim is filed with the assessor in the county where the replacement home is located. It is not handled casually through escrow and forgotten.

A Possible Ballot Fight Is Still Developing

Another development is that efforts to undo part of Prop 19 have continued.

A newer initiative was cleared for signature gathering in late 2025. Its goal is to reinstate broader property tax reassessment exclusions for certain transfers between family members, including by inheritance.

As of this writing, that does not change the current law. It is only a proposed initiative. The existing Prop 19 rules still apply unless and until voters approve a change.

That distinction is important. It is easy to read headlines or mailers about possible ballot measures and assume relief is coming. Maybe it is, and maybe it is not. Planning should be based on the law as it stands today, not on what might happen in a future election.

What Families Should Do Now

For families with California real estate, the practical takeaway is simple: do not wait until after a death or property transfer to understand the rules.

If parents intend for children to inherit a home, the family should discuss whether any child actually wants to live in the home as a primary residence. If not, the property may be reassessed. That may still be fine, but it should not come as a surprise.

If a child does intend to live in the home, the family should understand the filing requirements and deadlines. The paperwork can make the difference between a manageable property tax bill and a very unpleasant letter from the county assessor.

The lesson from my parents’ neighbors is not that everyone can avoid a property tax increase. The lesson is that a little knowledge can make a big difference.

They were fortunate. The problem was fixable, and the savings have now added up to tens of thousands of dollars. But it would have been much better to know the rules before the reassessment notice arrived.

Market Update: Geopolitical Events and Long-Term Perspective

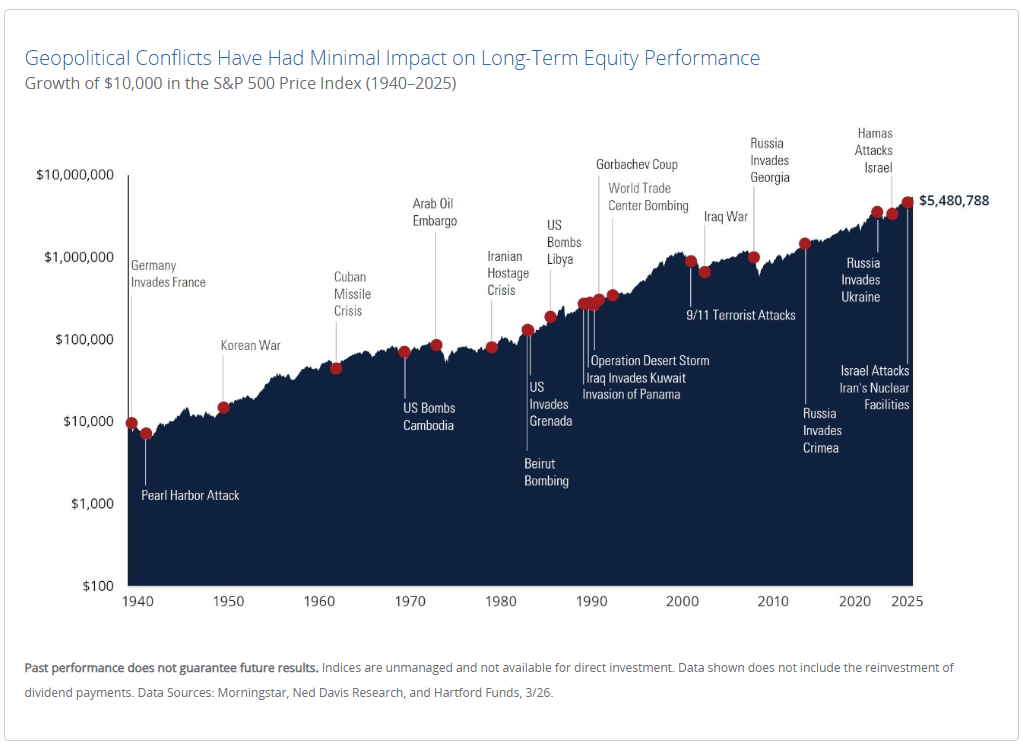

Since the Iran war began and concerns grew about disruption in the Strait of Hormuz, I have shared the Hartford Funds chart above with several clients who were understandably uneasy about what the conflict could mean for oil prices, the markets, and their portfolios.

That concern is reasonable. When military conflict appears in the headlines, markets often react quickly. The first response is usually uncertainty, and uncertainty is uncomfortable. We saw that when the U.S.-Iran conflict began on February 28. Oil prices jumped, stocks declined, and it was easy to imagine the situation getting worse before it got better.

The S&P 500 closed at 6,878.88 on February 27, the last trading day before the conflict began. By March 30, the index had declined to 6,343.72, a drop of about 7.8%. Reuters reported that the S&P 500 fell as much as 9% during the selloff, just short of the 10% decline generally considered a correction. By April 15, the index had recovered those losses and closed at 7,022.95, a new record high. More recently, the S&P 500 has been trading around 7,400, meaning it has moved meaningfully above where it stood before the fighting started.

What I appreciate about the Hartford Funds chart is that it doesn’t dismiss those concerns. It simply provides a wider lens.

The chart shows many difficult geopolitical events over the past 85 years, including Pearl Harbor, the Korean War, the Cuban Missile Crisis, the Gulf War, 9/11, Russia’s invasion of Ukraine, and the Hamas attacks in Israel. None of those events were trivial. Many were deeply painful and historically significant.

And yet, over long periods, the stock market has been driven more by earnings, productivity, innovation, inflation, interest rates, and the resilience of the broader economy than by any single geopolitical event.

That does not mean markets always recover quickly. It does not mean future conflicts will be harmless. It simply reminds us that making major portfolio decisions in the middle of frightening headlines has historically been very difficult to do well.

The recent market rebound doesn’t make the conflict any less serious, and it doesn’t mean the risks have disappeared. But it does show how quickly markets can move from fear to recovery, sometimes before the headlines feel resolved. For long-term investors, that is an important reminder: emotional reactions are understandable, but they are not always a reliable guide for portfolio decisions.

Coming Soon: A New Client Portal Through Advyzon

We are in the process of rolling out Advyzon, a state-of-the-art technology platform that will improve the client portal experience and help us streamline several parts of our internal workflows.

For clients, the most visible improvement will be a cleaner and more useful online portal. Advyzon will allow you to view account information, performance reports, allocation details, and shared documents in one place.

Behind the scenes, Advyzon also gives us better tools for reporting, document sharing, client service tracking, billing, and portfolio management. That may not sound exciting, but it matters. Good technology helps reduce duplicate work, keeps information organized, and allows us to spend more time on planning and client conversations rather than administrative follow-up.

There’s no action required on your part for now. We will provide more details before the portal goes live later this year, including instructions on how to log in and what you can expect to see.

As with any technology change, we expect there may be a few questions along the way. Our goal is to make the transition as smooth as possible and give you a better experience once everything is in place.

Welcome Aracely Enriquez, Our New Office Manager

We are happy to introduce Aracely Enriquez as TABR’s new Office Manager.

Many of you will begin hearing from Aracely as she helps coordinate scheduling, paperwork, client service requests, and the many small details that keep TABR running smoothly. A lot of good client service happens behind the scenes, and this role is an important part of that.

Aracely brings more than a decade of experience in customer service, operations, and team leadership. She began her career in customer service in 2010 and later moved into operations management, where she developed a strong foundation in process improvement, collaboration, and client-focused service. Her experience spans logistics and financial planning, giving her a practical understanding of how effective systems and clear communication support better client service.

Aracely earned her B.S. in Business Management from California State University, Long Beach. After graduating, she joined a Registered Investment Advisor (RIA) firm in Ontario, California, where she advanced to Team Lead in the Operations Specialist department. After that, she joined an RIA firm in Brea, California, and served as a Senior Client Services Specialist.

Outside of work, Aracely enjoys spending time with family, trying new restaurants, attending church, and making lasting memories.

Please join us in welcoming Aracely to TABR. We are grateful to have her on the team.

Portfolio Allocations

Since Bob Kargenian’s update on April 15, our stock allocation has changed several times as the models have adjusted to changing market conditions. We increased equity exposure from 40% to 80% on April 20, after additional stock market risk models turned positive. On May 11, one of our models moved back to a sell signal, and we reduced equity exposure from 80% to 60%. Earlier this week, we reduced our equity exposure from 60% to 40% based on another investment model going negative over the weekend.

Our high yield bond model also moved back to a buy signal on April 20, so we once again own high yield bonds in portfolios where appropriate. In all Tactical Accounts, we also established a partial position in gold on May 6 through IAU, the iShares Gold Trust.

This is a good example of how our process works in real time. We are not making allocation changes based on headlines, predictions, or opinions about where markets “should” go next. Instead, we follow our quantitative models and adjust exposure as the weight of the evidence changes.

No model is perfect, and there will always be times when markets move faster than any system can adjust. But having a defined process helps us avoid the bigger mistake of reacting emotionally to short-term news. The goal is not to capture every move perfectly. It is to participate when conditions are favorable, reduce risk when conditions deteriorate, and provide a smoother ride over time.

A Few Closing Thoughts

Taken together, these topics are a good reminder of what financial planning often looks like in real life. Sometimes it’s understanding a California property tax rule before it creates an expensive surprise. Sometimes it’s staying disciplined when unsettling headlines make the markets feel less predictable than usual. Other times, it’s improving the tools we use, adding the right people to the team, and continuing to follow a portfolio process that keeps decisions grounded rather than reactive.

In different ways, each of these areas matters because they affect how families make decisions, respond to change, and stay on track over time. Good planning does not remove uncertainty, but it can make the next decision a little clearer. As always, we are grateful for the trust you place in us and for the opportunity to help you think through these decisions along the way.

Best regards,

Steven W. Medland, MBA, CFP®

Partner

TABR Capital Management, LLC (“TABR”) is an SEC-registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure website (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs, and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore, the performance shown is net of TABR’s investment management fees, and also reflects the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes, and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services, and it is not known whether the clients referenced approve of TABR or its services.