How Safe Are Your Fidelity Accounts?

With the First Republic Bank, Silicon Valley Bank, and Signature Bank failures in the last two months, you may understandably be concerned about the safety of your money, including your bank accounts and Fidelity investment accounts.

To start, a little background may help. Fidelity Investments is one of the world’s largest and most well-respected investment companies with an over 75-year history of providing secure and reliable financial services. We can break up the security of investment accounts into two main categories. The first is safeguarding your personal and financial information from fraud and unauthorized access. The second is protecting your account balances if the firm itself was to fail, as in the cases of First Republic, Silicon Valley, and Signature Banks.

When it comes to protecting your personal and financial information from fraud and unauthorized access, Fidelity uses a number of security measures. This includes using strong website encryption to protect data and employing stringent security protocols. As I discussed in last December’s newsletter, you can also enable Fidelity’s 2-factor authentication and security text alerts for added protection.

But the above only serves to protect you from fraud and unauthorized access. What happens when a financial institution fails?

Fidelity Investments has over $10 trillion in assets under administration and serves over 40 million customers worldwide. Whether this makes Fidelity “too big to fail” or not is up for debate, as that term usually applies to banks instead of brokerage firms. However, it seems very unlikely that the US government would allow such a large and systemically important firm to fail in a worst-case scenario. In any case, I wouldn’t personally rely on a government bailout for any of my investments, so let’s look at some other factors.

While Fidelity is privately held and doesn’t release financial statements, it’s widely regarded as financially solid and stable, with $8 billion of operating income in 2022. Although a failure at Fidelity Investments seems extremely unlikely, your accounts would still be protected in that event for the following reasons.

First, the Securities and Exchange Commission (SEC) regulates Fidelity, and the SEC Customer Protection Rule (15c3-3) requires Fidelity to protect fully paid client securities by segregating them and ensuring they can’t be used for anything else, like corporate investments, loans, or spending. Remember the cryptocurrency exchange FTX failure last November? According to the Wall Street Journal, FTX tapped into customer accounts to fund risky bets, leading to its downfall. This couldn’t happen with Fidelity’s practice of segregating client securities.

Second, the Securities Investor Protection Corporation (SIPC) protects all Fidelity brokerage accounts. If a brokerage firm like Fidelity is closed due to bankruptcy or other financial issues and customer assets are missing from accounts, the SIPC covers a maximum of $500,000 in securities and up to $250,000 in cash that hasn’t yet been invested (the money market funds in brokerage accounts are considered securities by the SIPC).

What happens if your accounts exceed the $500,000 and $250,000 limits? Fidelity provides additional coverage in excess of SIPC limits through Lloyd’s of London and other insurers. Like SIPC coverage, excess SIPC protection doesn’t cover investment losses due to market fluctuation or other claims for losses incurred while broker-dealers are still in business. The total aggregate excess of SIPC coverage available through Fidelity’s policy is $1 billion.

Fidelity’s excess of SIPC coverage has no per-customer dollar limit for securities, but there is a per-customer limit of $1.9 million for cash awaiting investment. This coverage represents the maximum excess of SIPC protection currently available in the brokerage industry.

Finally, the Federal Deposit Insurance Corporation (FDIC) protects brokered CDs issued by an FDIC-insured institution and held in Fidelity brokerage accounts. This coverage for IRAs and brokerage accounts is $250,000 maximum per bank.

One of the reasons that Silicon Valley Bank customers had to be bailed out by the US government is that an estimated 85% of the bank’s deposits were greater than the $250,000 FDIC limit and, therefore, uninsured. That’s why whenever we meet with clients and see deposits over FDIC limits, we recommend changes to protect them.

Please note that the $250,000 coverage limit is per depositor and trust beneficiary, so your bank accounts may be covered for more than $250,000 in some cases. For example, if a couple has a joint bank account, FDIC insurance will cover up to $500,000. If a couple has a living trust bank account with two beneficiaries (i.e., two trustees and two beneficiaries), it will be covered by FDIC insurance of up to $1 million. The maximum coverage would be $1.25 million regardless of the number of beneficiaries. This gets complicated fast, but you can enter your bank account information using the FDIC’s online calculator, a great resource that prints out a report showing any of your accounts balances that aren’t covered by insurance.

With other banks currently at risk of failure, this would be an opportune time to confirm that all of your deposits are fully covered by FDIC insurance. As long as you have under $250,000 in an FDIC-insured bank, you don’t have anything to worry about. If you have any questions about the above or how to use the FDIC’s online calculator, please call our office.

Focusing On What We Can Control

All the angst caused by the banking crisis makes this a great time to talk about focusing on what we can control. None of us can control whether our bank fails, but we can all take the above steps to ensure our money is covered by FDIC insurance. This also applies to every other area of our personal finances.

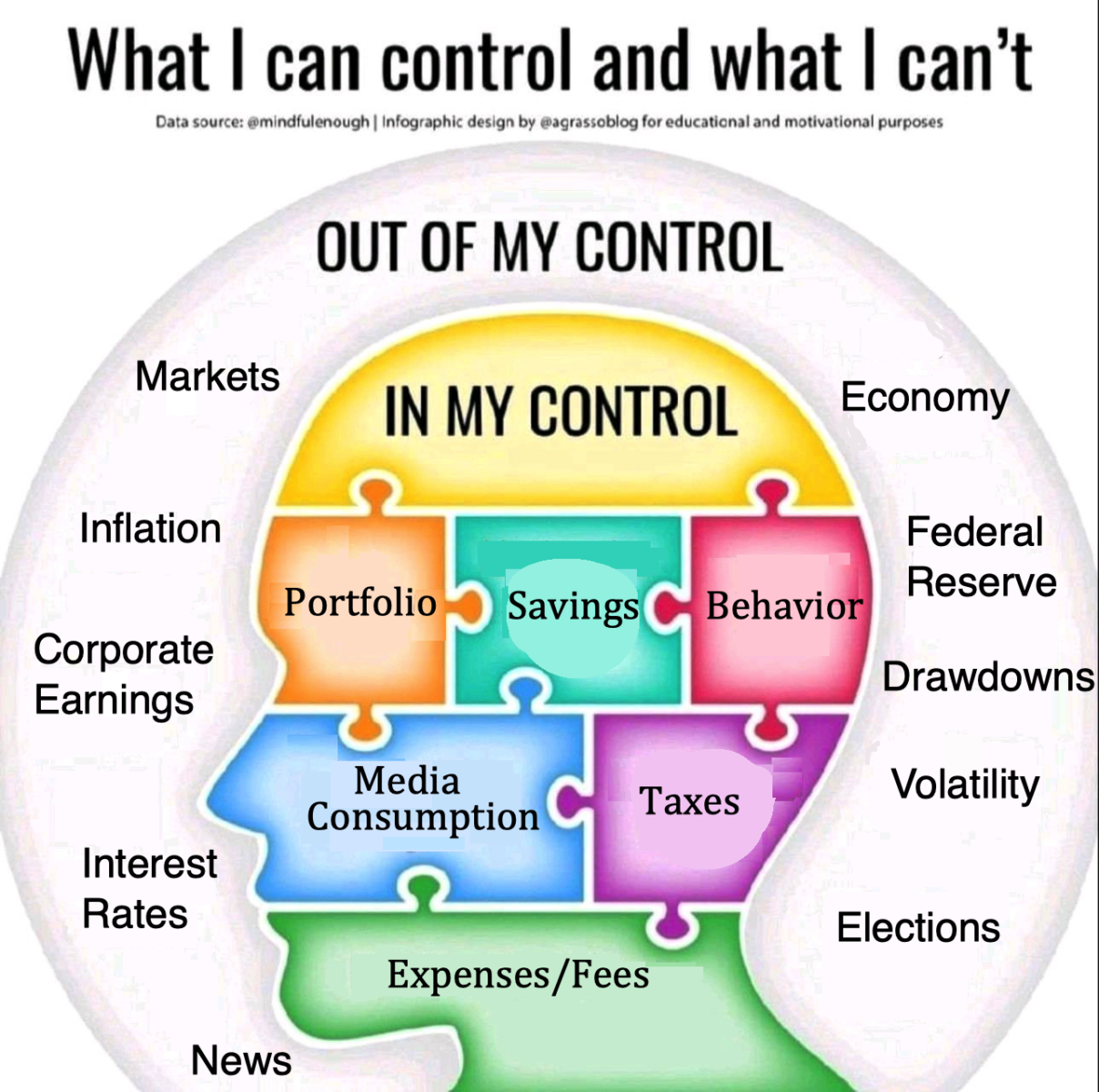

I recently came across a graphic from Barry Ritholz that illustrates the point well:

In his brief blog post accompanying the above graphic, Ritholz says, “I am often asked about how market action affects me — my psyche, emotions, and behavior. The short answer is very Zen: I understand what I can and cannot control, and then adjust accordingly.”

This caught my attention as my book, Spiraling Up: Discover Financial Serenity, Make Work Optional, and Live Happily in Retirement, begins with Principle One: Focus On What You Can Control. The Ritholz blog post is a timely reminder that we have no control over what happens in the markets, the economy, or whether banks fail, but we can control how we position our investment portfolio, our savings, spending, and news media consumption. In short, we can control our behavior, and that’s the most critical factor in determining long-term investment success.

The True Value of the Mortgage Interest Deduction

Over the years, many of our clients have told us they don’t want to pay off their mortgage due to fear of missing out on the mortgage interest deduction tax benefits. This is a benefit widely touted by real estate professionals, but it’s not always what it’s cracked up to be.

In one recent situation, a couple we work with had saved diligently and asked about paying off their approximately $300,000 mortgage, but they didn’t want to give up their mortgage interest deduction. Because they provided us with a copy of their tax return, we could see how much good the deduction was actually doing them.

It turned out they were paying about $15,000 in mortgage interest per year. When added to their other itemized deductions, it gave them a total of $29,000 in deductions on their tax return. However, the standard deduction in 2023 is $27,700, so they could only deduct an extra $1,300 by itemizing their deductions. They pay about 25% in taxes, so they only saved $325 per year ($1,300 * 25%) by deducting their mortgage instead of taking the standard deduction.

In other words, they paid $15,000 in mortgage interest to save $325 on their taxes. Their mortgage rate was 4.5%, so paying it off was like locking in a guaranteed 4.5% investment return. Sometimes the mortgage interest deduction can be helpful, but it’s clearly not in all cases. That’s why evaluating the pros and cons of having a mortgage or paying it off in each situation is essential. Our clients paid off their mortgage and now have the peace of mind of being completely debt free.

Last year we began using Holistiplan software to help us review our clients’ tax returns and evaluate tax planning strategies like Roth IRA conversions. It’s also a simple way to demystify your taxes and discover what you’re paying and why. We’ve received excellent feedback so far, and we’re incorporating this into our annual reviews when clients provide us with their tax returns.

Referrals to Other Professionals

Our clients in the story above had refinanced their mortgage through John Soricelli, Co-Founder and Managing Partner at J&J Coastal Lending in Huntington Beach. Like all of our clients we’ve referred to John, they were thrilled with the service he provided them.

John is one of several top-notch professionals my partner, Bob Kargenian, and I have gotten to know and introduced to many clients. Since founding TABR Capital Management in 2004, we’ve developed relationships with some outstanding estate planning attorneys, family law attorneys, real estate attorneys, life insurance agents, Medicare consultants, and CPAs, among others.

Remember that we’re a resource to connect you with other first-rate professionals whenever the need arises. We’d be happy to introduce you to those we know in the above areas. If you’re looking for someone outside the legal, real estate, and insurance areas, we may still know someone who could help. Just ask us. Even if we don’t know someone personally who specializes in your area of interest, we may know someone who knows someone who can get what you need.

Current Investment Allocations

In our most recent newsletter last month, Bob Kargenian wrote, “The first four months have been marked by choppiness, ups, downs, but very little in the way of trends, which is one of the worst environments for our risk models. At some point, this will change. Presently, 3 of our 5 stock market risk models are positive, and therefore our tactical stock market exposure is near 60% of its maximum.”

Another one of our models went on a buy signal on April 18, shortly after Bob wrote that update. As of today, 4 of our 5 stock market risk models are positive, so our tactical stock market exposure is approximately 80% of its maximum.

Our bond allocations have also changed with a buy signal in both high yield and the PIMCO Income Fund. On April 17, we sold our ultra-short bond funds and bought back into high yield bond funds. On May 8, we sold our PIMCO Short Term Fund positions and bought PIMCO Income Fund.

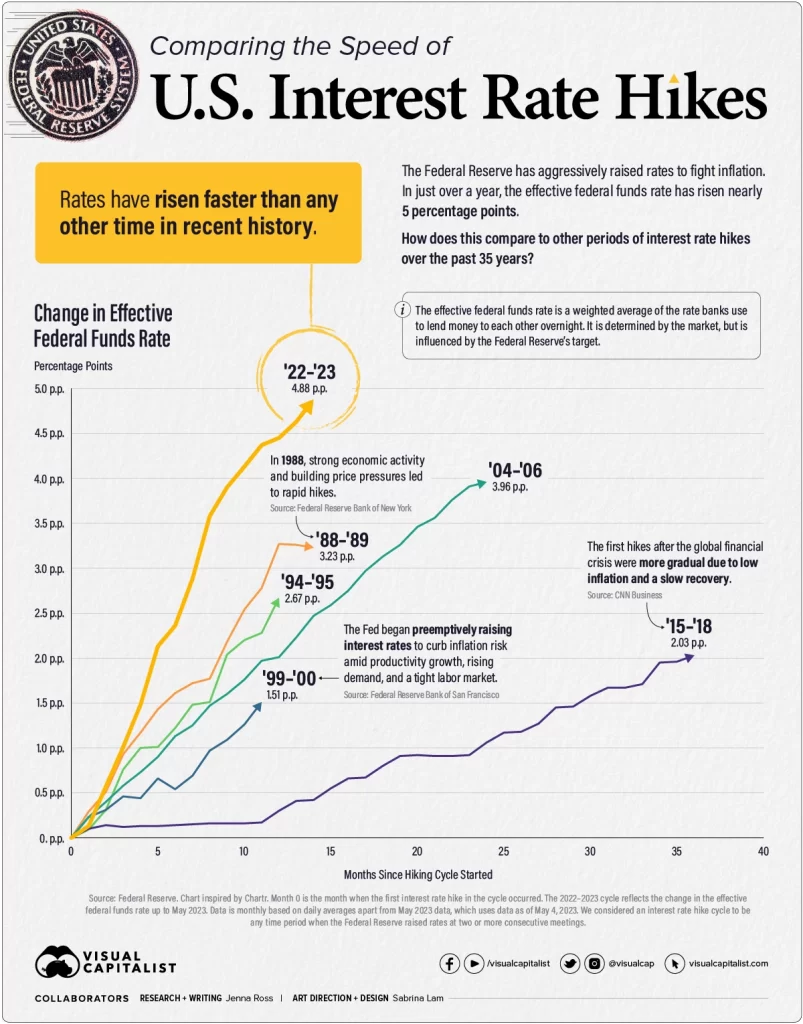

With most of our investment models in a buy mode, now is the time that we’d like to see a steady upward trend in the stock and bond markets. Whether we get that remains to be seen. One reason that casts doubt is the Federal Reserve has raised interest rates to fight inflation at a pace faster than any other time in the past 35 years, as shown by the yellow line in the chart below.

The nearly five percentage point rate increase in the last 14 months is a headwind for stocks because investors may begin to favor higher-yielding bonds over stocks. In addition, higher interest rates reduce the present value calculations of future stock earnings, putting pressure on stock prices. Higher interest rates also mean it’s more expensive for companies to borrow money for investment and expansion, which could negatively affect profitability and stock prices.

On the plus side for stocks, Fed Chair Jerome Powell signaled at the May meeting that the Fed might be close to pausing interest rate increases. When asked whether rates are now sufficiently high to tame inflation, Powell said, “We may not be far off. We’re possibly even at that level.”

The recent banking crisis will also factor into the Fed’s decisions. They’re walking a tightrope as it’s unlikely they’ll continue to raise interest rates if there’s a danger of causing more banks to fail.

Meanwhile, the unemployment rate is at 3.4%, the lowest in decades. Inflation is still higher than the Fed’s 2% goal, but it has decreased from 8% in calendar year 2022 to 4.9% today (over the previous 12 months). Chairman Powell’s comments reaffirmed they’d make decisions based on how the data unfolds, similar to our investment philosophy. Nobody can accurately predict what will happen in the markets or economy, reinforcing why focusing on what we can control is so important. That’s why we’ll continue to follow our investment models, and we’ll keep you informed as we make investment changes.

The Debt Ceiling Standoff

One of the factors that could at least temporarily disrupt the stock and bond markets is the current debt ceiling standoff. The debt ceiling is a self-imposed constraint, representing the maximum amount the US government can borrow to meet its spending needs, and we’re fast approaching that limit.

House Republicans passed a bill last month that would raise the debt ceiling but requires other provisions that would freeze government spending and some of President Biden’s programs. Treasury Secretary Janet Yellen said the so-called “X-date,” when the US government will run out of funds without an agreement, could arrive as soon as June 1, and that has many market prognosticators concerned.

Essentially, Republicans want the Biden administration to agree to spending cuts in return for a higher debt ceiling. The Biden administration wants to negotiate a clean debt ceiling increase, meaning a higher debt ceiling without agreeing to any demands.

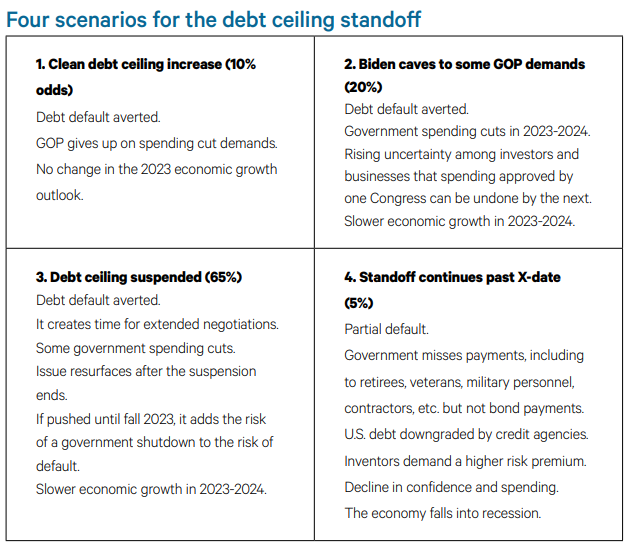

The two sides are in talks, and Ned Davis Research economist Veneta Dimitrova recently published a report on the impasse. The chart below shows her estimates of the likely outcomes. Her analysis indicates the overwhelming likelihood that a debt default will be averted one way or another, with only a 5% chance of a partial default. The US government has never defaulted on its debt, and that seems very unlikely even amid the current political posturing.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

Summer’s Almost Here

Even though the official start of summer is five weeks away, it feels much closer as my kids will be out of school at the end of this month. It’s hard to believe that Audrey will be a high school junior and Conrad will be a high school freshman in just three months. In the interim, we have lots of summer activities and travel planned, including a large extended-family trip to Oahu, where I was stationed on my submarine for four years, and our first trip to Italy together.

Here’s wishing you and yours a wonderful transition from spring to summer. As always, thank you for your continued trust and confidence in all of us here at TABR.

Best regards,

Steven W. Medland, MBA, CFP®

Partner

TABR Capital Management, LLC (“TABR”) is an SEC registered investment advisor with its principal place of business in the state of California. TABR and its representatives are in compliance with the current notice filing and registration requirements imposed upon registered investment advisors by those states in which TABR maintains clients. TABR may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to our investment advisory/management services. Any subsequent, direct communication by TABR with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of TABR, please contact TABR or refer to the Investment Advisor Disclosure web site (www.adviserinfo.sec.gov).

The TABR Model Portfolios are allocated in a range of investments according to TABR’s proprietary investment strategies. TABR’s proprietary investment strategies are allocated amongst individual stocks, bonds, mutual funds, ETFs and other instruments with a view towards income and/or capital appreciation depending on the specific allocation employed by each Model Portfolio. TABR tracks the performance of each Model Portfolio in an actual account that is charged TABR’s investment management fees in the exact manner as would an actual client account. Therefore the performance shown is net of TABR’s investment management fees, and also reflect the deduction of transaction and custodial charges, if any.

Comparison of the TABR Model Portfolios to the Vanguard Total Stock Index Fund, the Vanguard Total International Stock Fund, the Vanguard Total Bond Index Fund and the S&P 500 Index is for illustrative purposes only and the volatility of the indices used for comparison may be materially different from the volatility of the TABR Model Portfolios due to varying degrees of diversification and/or other factors.

Past performance of the TABR Model Portfolios may not be indicative of future results and the performance of a specific individual client account may vary substantially from the composite results above in part because client accounts may be allocated among several portfolios. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable

For additional information about TABR, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

A list of all recommendations made by TABR within the immediately preceding one year is available upon request at no charge. The sample client experiences described herein are included for illustrative purposes and there can be no assurance that TABR will be able to achieve similar results in comparable situations. No portion of this writing is to be interpreted as a testimonial or endorsement of TABR’s investment advisory services and it is not known whether the clients referenced approve of TABR or its services.